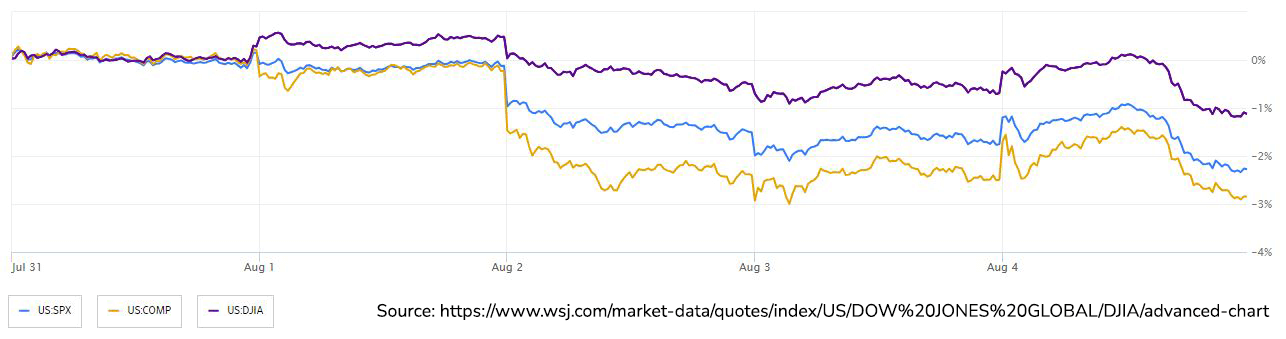

Stocks declined on Friday as Apple's market value dipped below $3 trillion and other large companies like Tesla and Meta Platforms also saw losses. However, Amazon's stock rose by about 8% after reporting strong results. The S&P 500 erased an earlier 1% gain, and the dollar retreated against other major currencies. Despite a strong earnings season for technology companies, the stock market has not rewarded them, as the rosy outlook was already priced in. Technology and internet firms have been standouts with a high earnings beat rate, but their stocks have fallen on average after reporting positive results. This decline is expected given the significant stock gains this year, which have lifted valuations to levels last seen when interest rates were near zero. The tech-heavy Nasdaq 100 has gained significantly this year, but it is down from its peak in July. The Treasury yield curve has experienced a bear steepening, with yields on 30-year Treasuries rising above their five-year counterparts for the first time since June. This shift has surprised and unnerved investors as they expected a rally in shorter-term debt amid Federal Reserve policy tightening. However, economic data and positive earnings reports have convinced traders that the Fed will control inflation without causing a severe economic slowdown. As a result, investors are demanding higher yields for longer maturities. Plans for increased issuance and Fitch Ratings' downgrade of the US credit ranking have also contributed to the selloff in longer bonds. The Treasury's decision to increase the size of its bond sales and the Bank of Japan's move to allow higher yields have added to the global debt selloff.

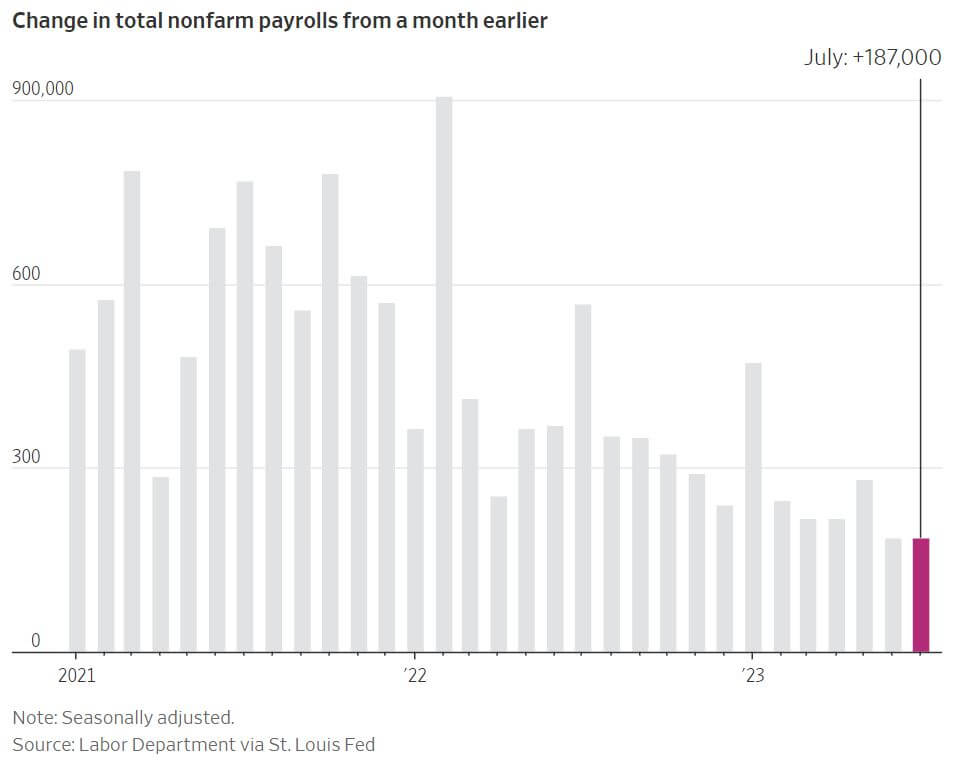

Employers in the U.S. slowed their hiring pace over the summer, signaling a gradual easing of the economy. In July, the U.S. economy added 187,000 jobs, slightly below the downwardly revised figure of 185,000 in June, and a significant drop from last year's monthly average of 400,000 job gains. The unemployment rate declined to 3.5% in July, indicating a strong job market near a half-century low. Average hourly earnings grew 4.4% in July compared to the previous year, slower than last year's growth but still higher than pre-pandemic levels. Fed officials estimate that wage growth of 3.5% would be consistent with their 2% target for inflation. Some sectors experienced job cuts in July, including temporary help services, tech and information companies, and retailers, while healthcare employers added staff. The employment report could relieve pressure on the Federal Reserve to raise rates at its next meeting in September. The central bank expects job growth to slow as part of its efforts to combat inflation. Officials will monitor additional hiring data for August and inflation readings for July and August before making any decisions. The economy appears to be on a slow but steady path toward a soft landing, where inflation returns to the Fed's 2% target without a recession or significant job losses. Despite the overall job gains, some industries, such as tech companies, retailers and temp agencies, have experienced slowdowns or job cuts. The hiring trend is now more concentrated in specific sectors like healthcare and government, while other sectors have not fully recovered from pandemic-related job losses.

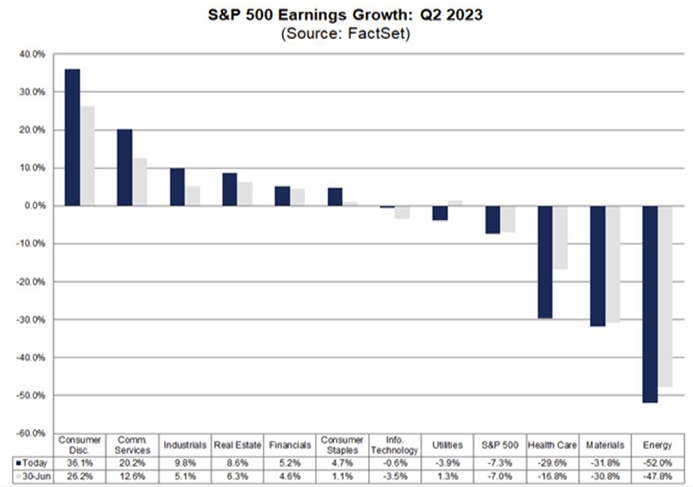

So far, 51% of the companies in the S&P 500 have reported actual results for Q2 2023. As of the mid-point of the Q2 earnings season for the S&P 500, more companies have reported positive earnings surprises than usual, but the magnitude of these surprises is lower compared to recent averages. Consequently, the index is reporting higher earnings for the second quarter compared to the end of the previous week but still lower earnings compared to the end of the quarter. In fact, the index is reporting its largest year-over-year decline in earnings since Q2 2020, with blended actual and estimated earnings falling 7.3% for the quarter. Positive earnings surprises in the Communication Services and Information Technology sectors have contributed to a decrease in the overall earnings decline for the index over the past week. However, downward revisions to EPS estimates for a company in the Health Care sector have partially offset this improvement. On the revenue front, 64% of S&P 500 companies have reported actual revenues above estimates, though slightly below the 5-year average. Nevertheless, the aggregate revenues are 1.5% above estimates, surpassing the 5-year average. Looking ahead, analysts still expect earnings growth for the second half of 2023. Projections indicate earnings growth of 0.2% for Q3 2023 and 7.5% for Q4 2023, with a predicted earnings growth of 0.4% for the entire CY 2023. The forward 12-month P/E ratio is 19.4, higher than both the 5-year and 10-year averages, indicating relatively high market valuations.