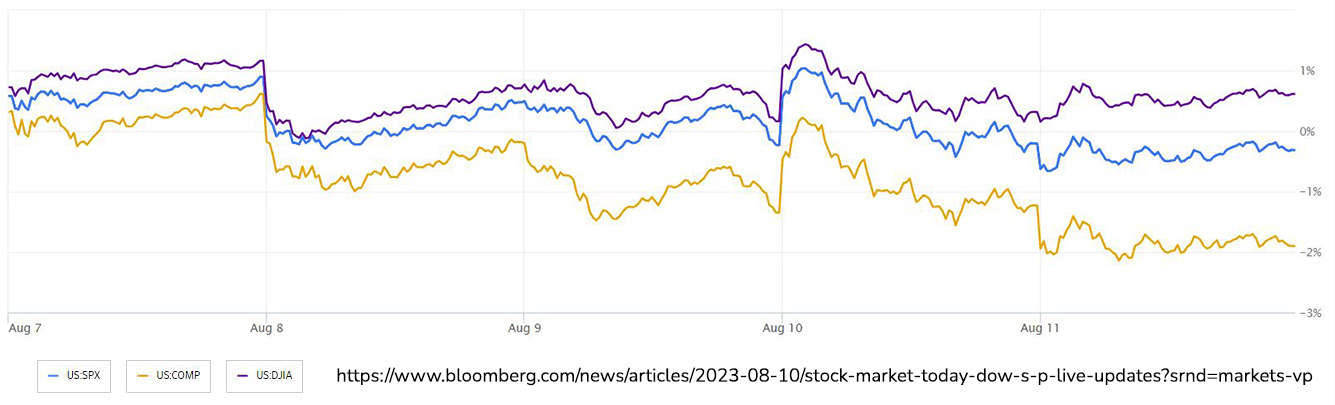

Tech mega-caps experienced a renewed slide and mixed economic data led to uncertainty in the stock market on Friday. The S&P 500 closed at a one-month low, dropping by 0.1%, while the Nasdaq 100 hovered near 15,000, facing its longest weekly losing streak this year, and the Dow Jones Industrial Average recorded a mild gain. Analysts note that stocks have lost momentum and could be heading for a correction in the near future, particularly as the volatile September/October period approaches. Despite near-term oversold conditions, some experts expect stocks to attempt an oversold rally. The equity risk premium, which measures the gap between S&P 500 earnings yield and the 10-year Treasury rate, indicates that stocks are becoming overvalued compared to bonds. However, historical analysis reveals that this gauge is at a level where S&P 500 returns historically averaged high single digits over a 12-month period.

Economic reports did not significantly impact swap market expectations that the Federal Reserve will pause its rate hikes next month. Consumer inflation expectations unexpectedly fell in a welcome sign for the Fed. UK bond yields increased as data revealed the British economy's strong quarterly growth, pressuring the Bank of England to consider further rate hikes. Oil extended its rally, achieving its longest streak of weekly gains since mid-2022, supported by forecasts of increased demand, supply disruption risks and prolonged Saudi production cuts. The yield on 10-year Treasuries increased by six basis points to 4.17%, while Germany's 10-year yield advanced by nine bps to 2.62%, and Britain's 10-year yield surged by 16 bps to 4.53%. West Texas Intermediate crude oil rose by 0.4% to $83.12 a barrel, and gold futures fell by 0.2% to $1,945.70 an ounce.

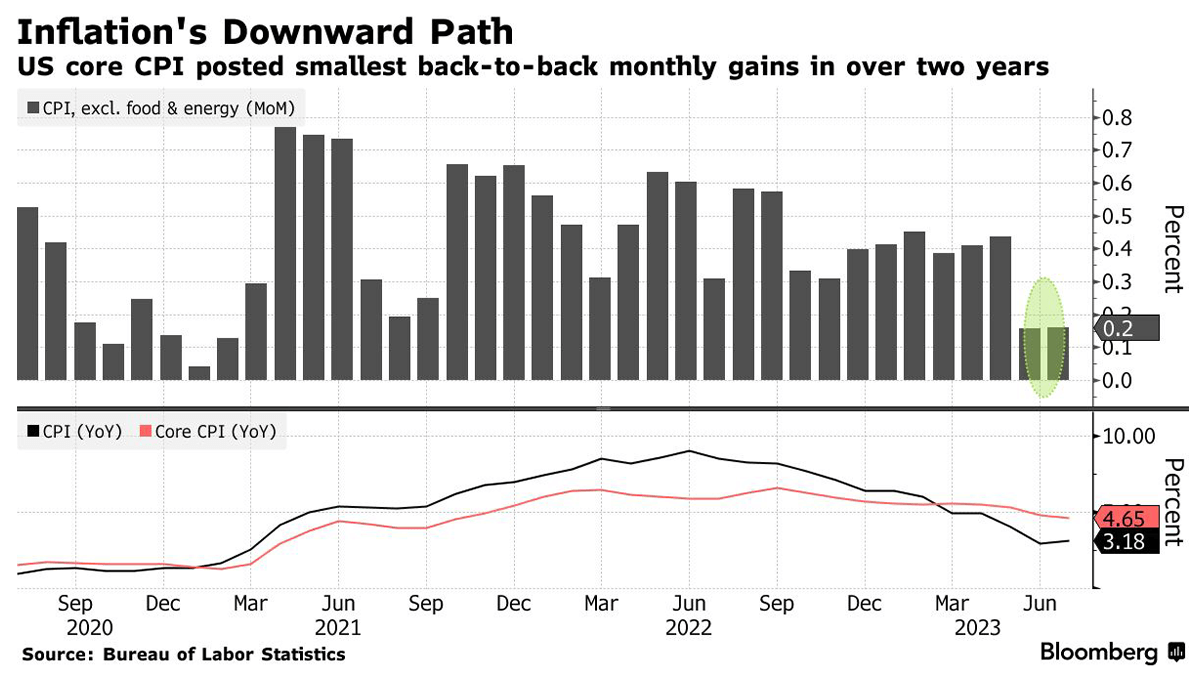

The US Core Consumer Price Index, a crucial gauge of consumer prices, experienced a modest increase of 0.2% for the second consecutive month, according to Bureau of Labor Statistics data. This represents the smallest gains over a two-year span. Economists consider the core measure, which excludes volatile food and energy costs, to be a better indicator of underlying inflation than the overall Consumer Price Index (CPI), which also saw a 0.2% monthly increase. However, the annual CPI figure showed a slight uptick to 3.2% due to an unfavorable comparison with the index from a year prior. US producer prices increased in July due to rises in certain service categories, indicating challenges in managing inflation, though that marked the first increase in three months. The producer price index for final demand and the core index (excluding food and energy) both rose by 0.3%, slightly surpassing forecasts. While this growth was higher than expected, downward revisions to the previous month's data moderated the strength of the trend. However, inflationary pressures are resurfacing due to increasing oil prices. While the recent CPI report increases the likelihood of the Fed maintaining current interest rates at the upcoming meeting, inflation remains higher than the target. The report highlighted that more than 90% of the overall CPI increase was attributed to housing costs, which have moderated since the year's start and are expected to fall in the future. In fact, excluding shelter, inflation would have been 1% last month compared to a year ago. Despite these positive indicators, uncertainties persist concerning the economy and inflation, with factors such as resuming student loan payments and tightening lending conditions acting as potential headwinds. The trajectory of inflation could become more uncertain, with factors like gasoline prices and health insurance adjustments potentially impacting consumer price growth.

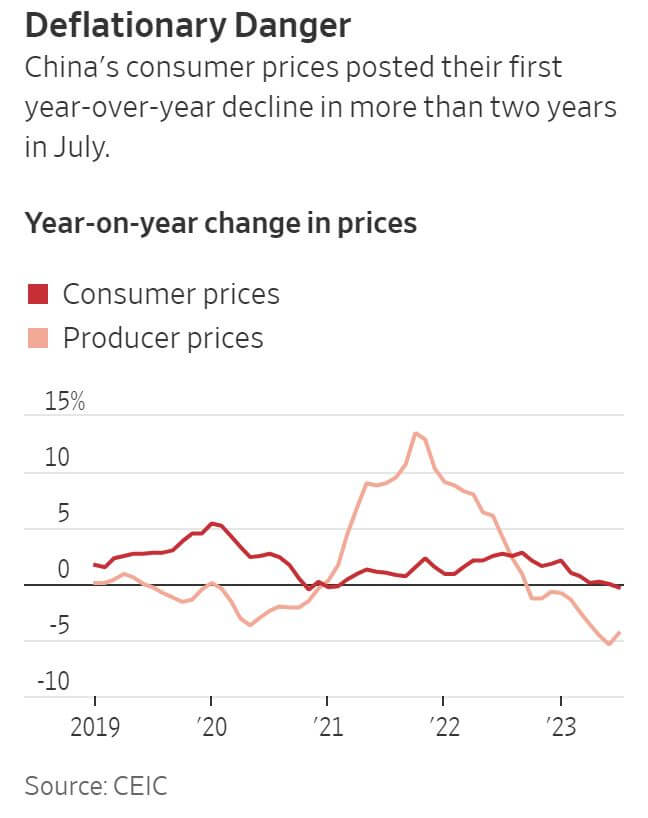

China's economy is facing a dangerous phase of deepening economic troubles. In July, consumer prices in the country entered deflationary territory for the first time in two years due to a range of issues impacting its recovery from COVID-19 restrictions. This stands in contrast to much of the world where economies are grappling with inflation. The Chinese economy is mired in challenges including declining exports, high youth unemployment, and a prolonged housing market downturn. Unusually, China is experiencing falling prices across commodities like steel and coal, daily essentials and consumer products. This deflation could potentially harm demand, worsen debt burdens and trap the economy in a difficult cycle. Deflation is risky for China given its high debt levels. The country's total debt is nearly three times its GDP, surpassing the US, according to the Bank for International Settlements. The situation is worsened by a lack of social security support for households, which incentivizes them to save for a rainy day and limit spending. China's central bank has cut interest rates several times this year, but the government has not yet implemented significant stimulus measures due to concerns about high debt levels. Unlike Western countries that have provided consumer cash handouts, China hasn't directly supported households, preferring historically to stimulate the supply-side of the economy. The central bank is expected to lower interest rates further, but experts are skeptical that this alone will restore consumer confidence.