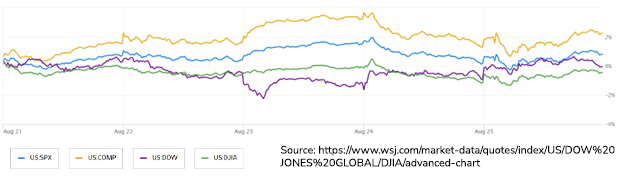

US equities were mainly higher last week, with the S&P 500 and Nasdaq Composite ending a three-week streak of weekly declines. The markets saw mixed performance driven by a blend of factors. The Federal Reserve's optimistic outlook, particularly from Chairman Powell, buoyed market sentiment as he refrained from suggesting higher interest rates or opposing rate cuts in 2024. However, economic data showed signs of weakness, including subdued manufacturing data and concerns about over-optimistic 2024 earnings estimates due to various factors. Investor positioning improved, potentially indicating oversold conditions, and the S&P earnings revisions turned positive. Nvidia's robust earnings results were a standout, with solid growth in AI-driven Data Center revenue and improved demand visibility. Nonetheless, the surge in yields remained a significant concern, impacting stocks. Powell's Jackson Hole speech provided reassurance, emphasizing data-driven decision-making and a commitment to restrictive policy until inflation reaches the 2% target.

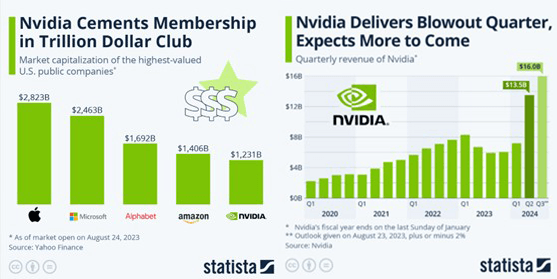

The chip maker announced earnings on Wednesday after market close that saw Nvidia surpass forecasted earnings for the third-straight quarter. The company has been at the heart of the recent AI boom and has returned over 200% through August. Nvidia now joins the ranks of the trillion-dollar club of mega-cap stocks as the recent stock price as of 8/24 translates to a valuation of $1,231 billion. Nvidia CEO and founder Jensen Huang noted on Wednesday's earnings call when asked if the current growth was sustainable: "This is not a near-term thing… This is a long-term industry transition, and Nvidia plans to be at the heart of it."

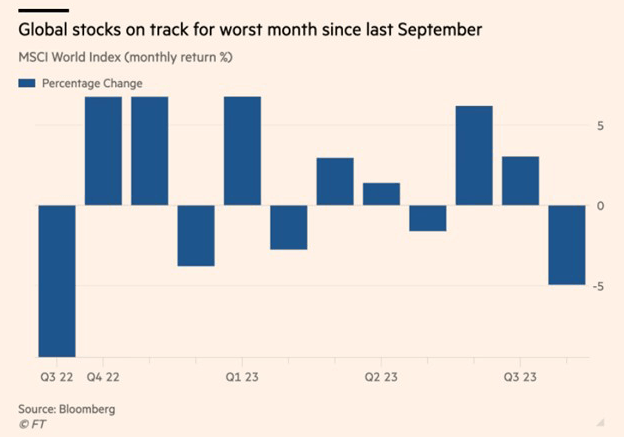

Global stocks have shed $3 trillion in value this month as economic data from China and rising borrowing costs in the US put a damper on investor sentiment. The S&P 500, Europe's Stoxx 600 and China's CSI 300 have lost $2.8 trillion in value, an approximate fall of 5% and an amount equivalent to the entirety of the London FTSE 100's market cap. While equity markets had one of the strongest first halves of a year in nearly 40 years, the recent US economic data and stubborn Eurozone inflation have caused investors to rethink the path of inflation and interest rates. Western European markets are particularly affected, as they face additional challenges due to indications that China, the world's second-largest economy, is encountering difficulties adapting to a post-pandemic environment. There have been increased concerns from analysts and investors over Beijing's failure to follow through on support for the weakened property sector and slowing consumer sentiment. Concern remains high for the European market for many analysts. Higher interest rates, tighter credit conditions and slowing Chinese demand weigh on the economy.