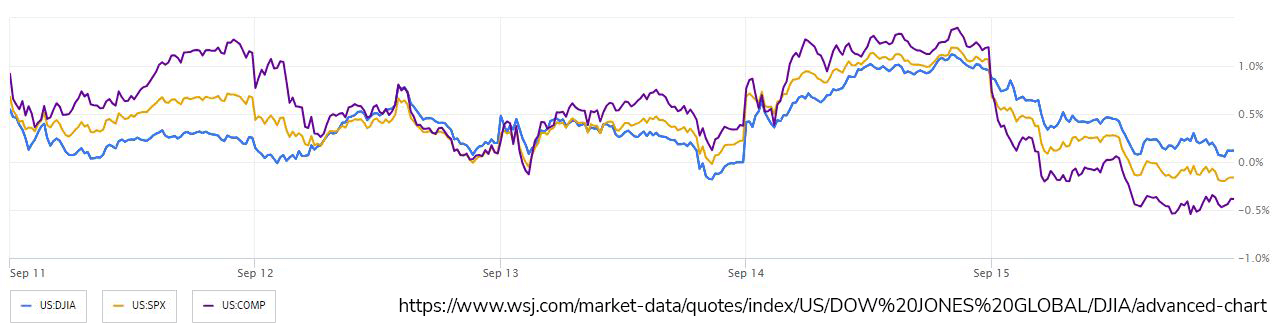

Stocks experienced a decline on Friday marked by significant volatility, driven by a confluence of factors including a large options expiration event and labor strikes affecting Detroit automakers. Major technology companies, such as Nvidia and Meta Platforms, led the losses, with their shares dropping over 3.5%. The S&P 500 erased gains made earlier in the week, while the Nasdaq 100 saw a nearly 2% decline. This volatility was further exacerbated by news that Taiwan Semiconductor Manufacturing Co. had requested a delay in the shipment of high-end equipment, leading to a drop in chipmakers. In the derivatives market, a significant options expiration event occurred, prompting traders to either roll over existing positions or initiate new ones. This event coincided with the rebalancing of benchmark indexes, notably the S&P 500, which added to the overall turbulence in the stock market.

In terms of economic data, U.S. inflation expectations declined to their lowest point in over two years, despite increased consumer optimism about the economic outlook. New York state factory activity unexpectedly expanded, while factory production experienced minimal growth due to reduced output in the motor vehicle sector. Economists surveyed by Bloomberg News suggested that the resilience of the U.S. economy would likely lead the Federal Reserve to consider one more interest rate hike this year, with an extended period at the peak level in 2024. Equity funds witnessed the largest weekly inflow in 18 months, reflecting growing investor confidence in a soft landing for the U.S. economy.

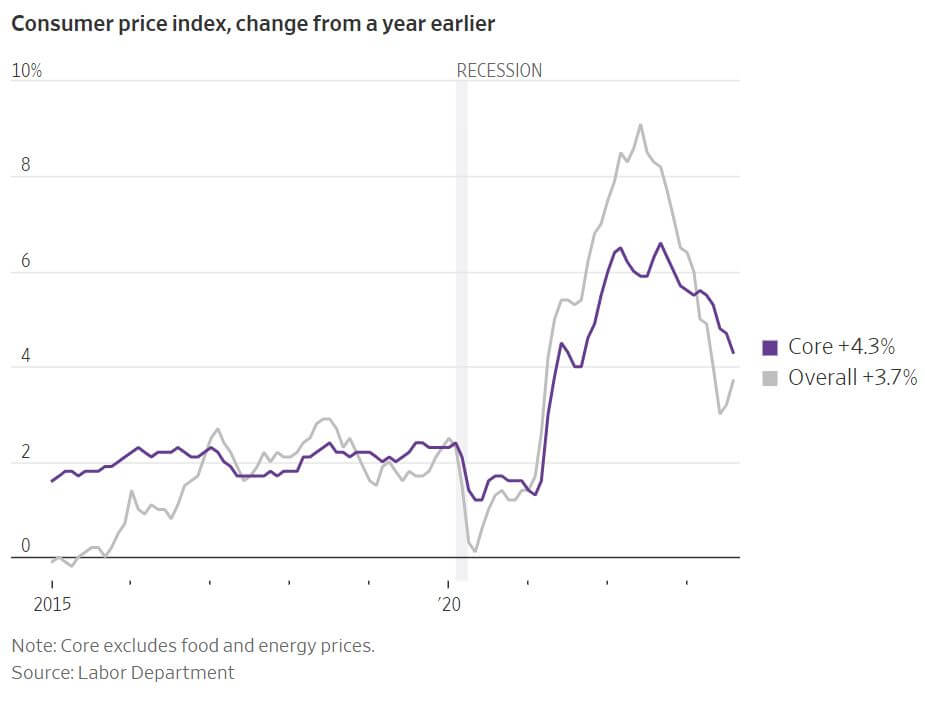

In August, consumer prices in the U.S. rose compared to the prior month, primarily driven by a surge in energy costs. The consumer-price index, a key measure of inflation, rose by 0.6% from the previous month, with more than half of this increase attributed to higher gasoline prices. However, when looking at core prices, which exclude the volatile food and energy components, the rise was a more modest 0.3% in August, following even lower readings in June and July. These core price increases were mainly due to higher expenses in areas like airfares and vehicle insurance. This data is likely to allow the Federal Reserve to maintain its current stance on holding interest rates steady at its upcoming meeting, without settling the ongoing debate on whether to raise rates further this year to control inflation and maintain economic stability. Financial markets reacted with mixed results to this inflation data on Wednesday, with the Dow Jones Industrial Average falling by 0.2%, while the broader S&P 500 inched up by 0.1%, and the NASDAQ Composite rose by 0.3%. On an annual basis, overall prices increased by 3.7% in August compared to 3.2% in July. However, annual core inflation decreased slightly to 4.3% in August from 4.7% in the previous month.

Several factors could exert upward pressure on prices in the coming months. Saudi Arabia's decision to extend crude oil output cuts could keep gasoline prices elevated. Labor strikes, such as the strike by the United Auto Workers union, could disrupt production and affect prices. Additionally, labor contracts in sectors like airlines and healthcare may increase worker pay at a time when the Fed aims to cool inflationary pressures by slowing wage growth. It's important to note that while there has been a slowing of inflation over the past year, many Americans are still grappling with higher prices for various goods and services. Rising energy and food costs, which heavily influence inflation perceptions, can impact consumer behavior, including wage demands from employees.

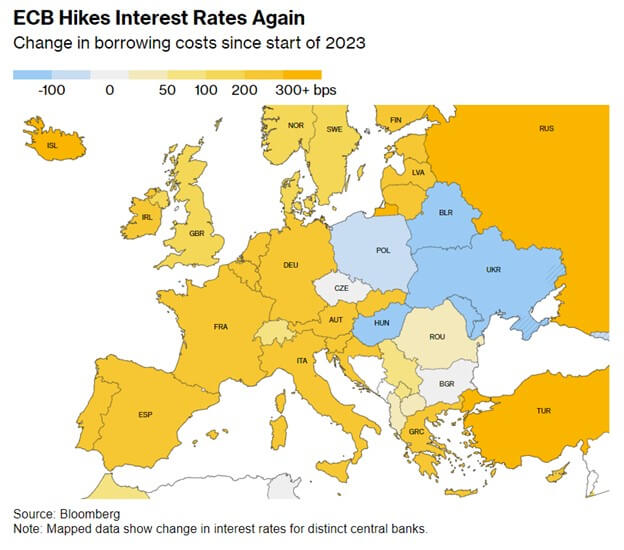

The European Central Bank (ECB) recently announced a quarter-percentage-point increase in interest rates, reaching a historic high. This decision marked the 10th consecutive rate hike, a significant ascent from negative rates just a year ago. ECB President Christine Lagarde suggested that this rate increase might be the final one but did not rule out further increases if necessary to bring inflation down to the 2% target. However, Lagarde's statement led investors to revise their expectations for future ECB rates, causing a drop in the value of the Euro against the dollar and a decline in bond yields. European stocks, on the other hand, saw gains. It's important to note that the Eurozone still maintains lower interest rates compared to the U.S., though it is facing higher inflation and a struggling economy. Investors are now betting that rates may peak and even start to decline by next spring as both inflation and economic growth recede. Market data from Refinitiv suggests that the ECB may maintain interest rates at around 4% through next summer before considering rate cuts. In contrast, the Federal Reserve is expected to maintain rates within a range of 5.25% to 5.5%, possibly initiating rate cuts early next year. The Bank of England is also anticipated to raise interest rates at least once this year before considering rate cuts in the following year. Economic forecasts released by the ECB suggest a more significant slowdown in Eurozone growth than previously expected for the current and following years, with inflation projected to remain well above the 2% target due to increased energy prices.