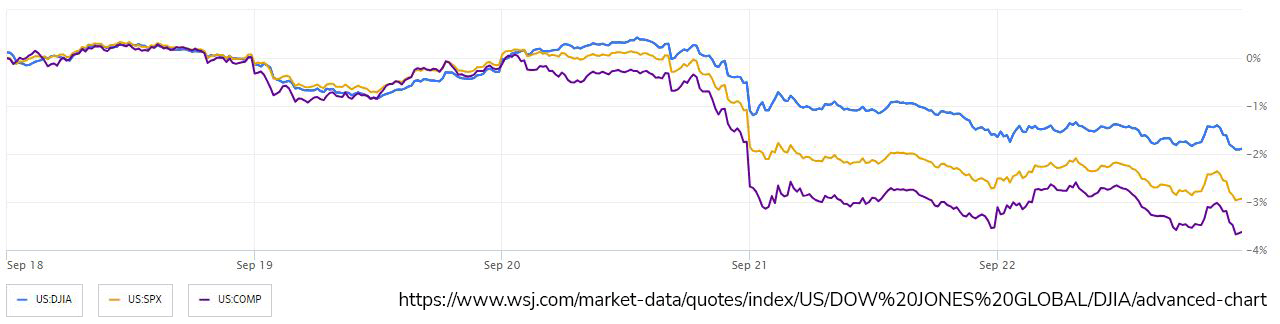

In a volatile week, Treasuries rebounded while stocks struggled as investors adjusted to the Federal Reserve's anticipated longer-lasting stance on higher interest rates. The 10-year yield briefly surpassed 4.5%, marking the first time since 2007, while the S&P 500 experienced its worst week since March, with tech stocks outperforming due to Apple's product launches. US-listed Chinese shares also rallied on news of economic discussions between Washington and Beijing. Concerns about inflation and Fed policy persisted, with some officials suggesting the possibility of more rate hikes. Market analysts emphasized that it is premature to conclude that markets have stabilized. Equities saw significant outflows as higher interest rates raised concerns about a potential recession. In corporate news, the United Auto Workers reached an agreement with Ford while expanding strikes at other companies, and Microsoft's acquisition of Activision Blizzard received UK regulatory approval. The Federal Trade Commission was expected to sue Amazon for antitrust violations. In market movements, the S&P 500 fell, the yield on 10-year Treasuries declined, and cryptocurrencies showed mixed performance.

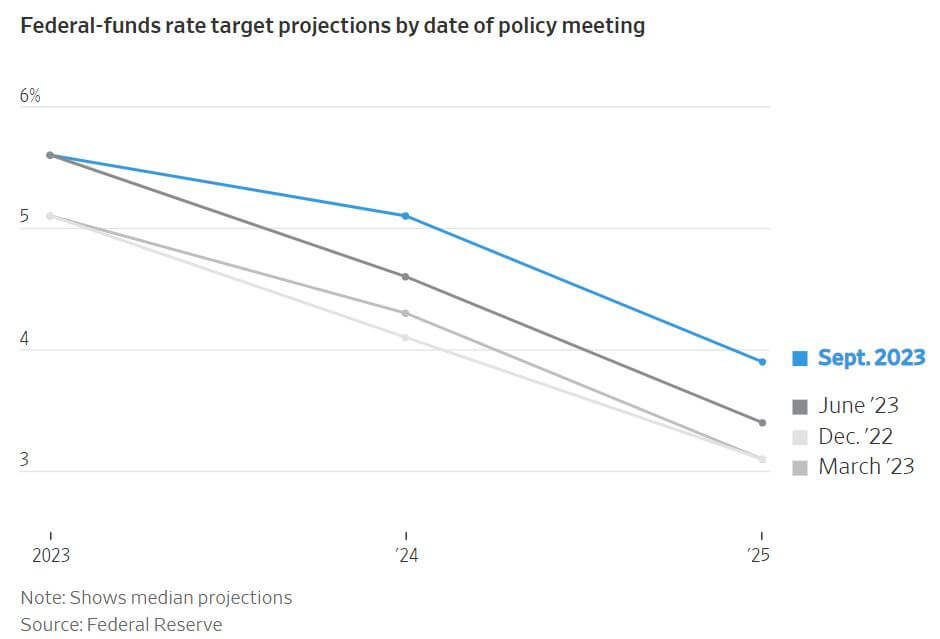

Federal Reserve officials opted to maintain interest rates at their current level last week, which remains at a 22-year high. The decision comes in light of stronger-than-expected economic activity, and most officials anticipate the need to keep interest rates near their current level through 2024. This decision marks the second time this year that the Fed has refrained from raising rates, having also paused in June. Fed Chair Jerome Powell emphasized a cautious approach, stating that the timing of another rate hike would depend on incoming data. The Fed acknowledges that rate increases typically take a year or longer to impact economic activity, and a slower pace of hikes allows them to monitor the economy's response more effectively. The new economic projections reveal that a majority of officials expect to raise rates once more this year, aligning with their outlook from June. They are scheduled to meet again in October and December. The median projection suggests a reduction in the federal funds rate to approximately 5% by the end of 2024, implying the possibility of two rate cuts in the coming year if a rate hike occurs this year. Officials have adjusted their economic growth projections upward for this year and the next, accompanied by a lower unemployment rate forecast compared to their June projections. Most officials anticipate that the unemployment rate will rise to 4.1% next year, lower than previously expected. The Fed’s forecast for core inflation, which excludes food and energy prices, decreased slightly to 3.7% for the fourth quarter, down from 3.9% in June. However, robust economic growth and concerns about rising prices for commodities like oil and transportation could lead to inflationary pressures reemerging, necessitating higher rates.

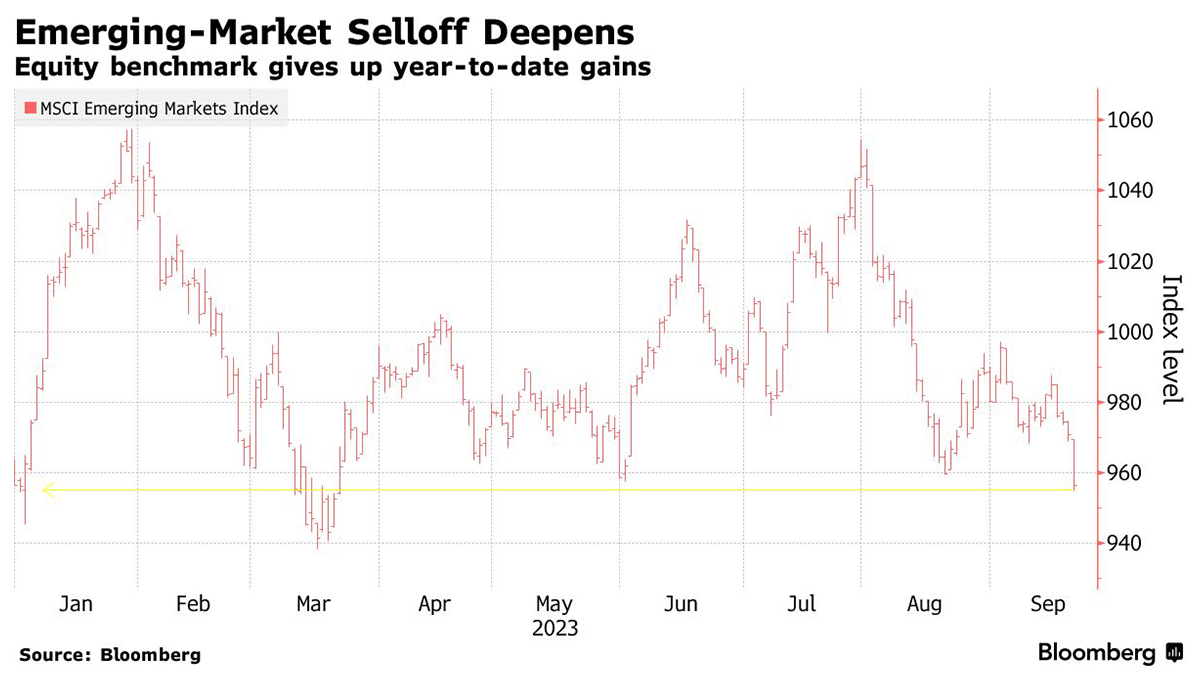

The US dollar has surged against major currencies in the last two months, largely due to a growing divergence in the global economy. While the US economy has defied earlier pessimistic forecasts and continued to perform strongly, growth in China and Europe has faltered. Many economists had predicted that the Fed would be shifting towards recession-fighting measures by now, including reducing interest rates. However, the US economy has outperformed expectations, leading investors to move their funds to the US, where higher interest rates are expected to persist. This shift in investor sentiment has driven the Bloomberg Dollar Spot Index back towards its yearly highs after an eight-week rally starting in mid-July. Though the current dollar surge is not as steep as the one experienced in 2022, it still has global consequences, especially in emerging markets. A stronger dollar makes imports more expensive and intensifies inflation pressures, forcing central banks in developing nations to maintain high interest rates to protect their currencies and prevent capital flight. The combination of the Fed signaling a prolonged period of higher interest rates and China's economic challenges has created a double shock for emerging-market equities. The ongoing underperformance of emerging market equities relative to US equities is now extending into a sixth consecutive year. Earnings estimates for companies in the MSCI gauge have fallen by 2% this year, and valuations remain relatively high, with the index trading at 11.8 times the projected earnings of its constituent companies, only slightly below the five-year average.