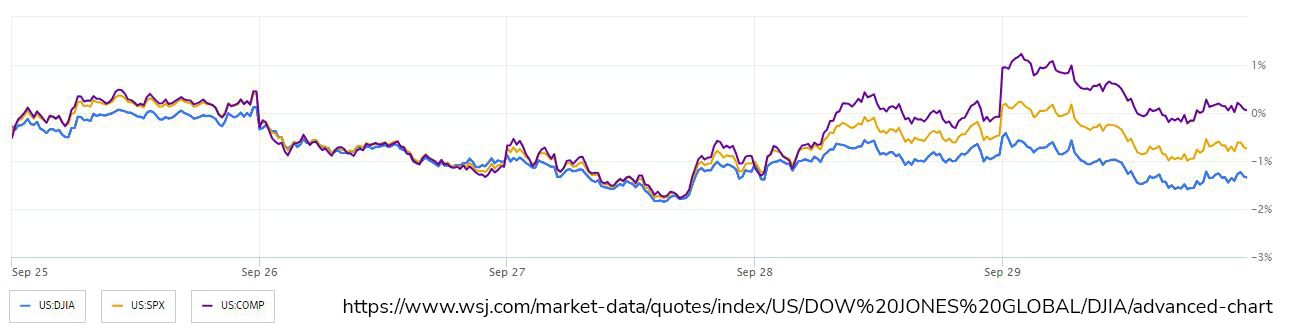

Markets saw a rebound Friday in US stocks and Treasuries, but that momentum waned after the head of the Federal Reserve Bank of New York suggested that interest rates should remain high for an extended period. As a result, the S&P 500 fell by 0.3%, and the Nasdaq 100 lost its gains for the day. The yields on two-year Treasury bonds remained steady, but the benchmark 10-year Treasury yield increased to 4.57%, the highest since 2007. Global bonds are facing their worst monthly selloff since February, although cautious comments from other Federal Reserve officials and signs of moderating inflation have eased immediate rate hike fears. The financial markets appear uncertain, and Bill Ackman of Pershing Square Capital expressed caution about longer-dated Treasuries potentially reaching a yield beyond 5%. Despite these challenges, some experts remain bullish on bonds maturing in five to 10 years, citing falling inflation as a potential positive factor. Futures for West Texas Intermediate oil finished the week at $90.90.

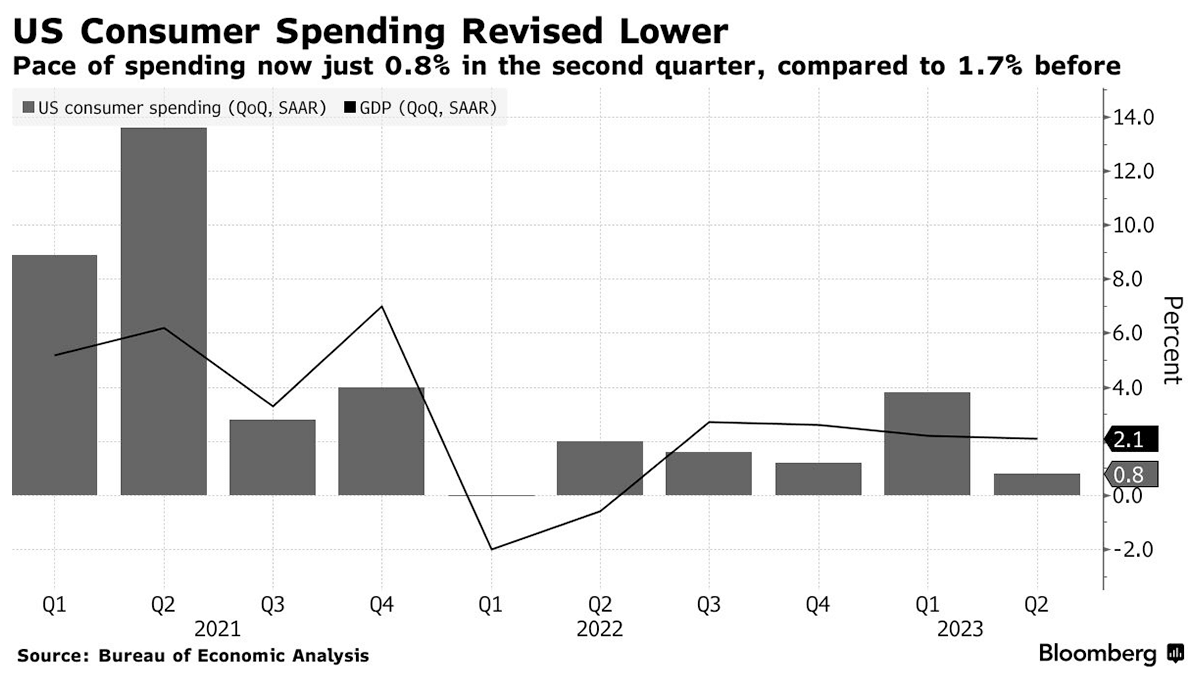

In the second quarter, U.S. consumer spending experienced a slower growth rate than previously reported, primarily due to weakened services spending according to new government data. Personal consumption, a key driver of the U.S. economy, increased at an annualized rate of 0.8% during April to June, marking a significant drop from the prior estimate of 1.7% and representing the weakest growth in over a year. Nevertheless, overall GDP remained unchanged, growing at a 2.1% rate during the same period. The slowdown in consumer spending was partially offset by stronger business fixed investment, which increased at a pace of 7.4%, up from the previously reported 6.1%. The slowdown in spending brings renewed focus on household savings balances, which saw a substantial increase due to government stimulus checks and reduced spending opportunities during the pandemic. The amount of remaining savings is significant, as it could bolster consumer spending in the coming months and act as a financial cushion, making it easier for individuals to weather economic downturns and reducing the likelihood and severity of recessions. A pessimistic estimate from the Federal Reserve Bank of San Francisco suggests excess savings peaked at around $2.1 trillion in August 2021 but had dwindled to less than $190 billion by the second quarter of 2023. However, different assumptions and data revisions can lead to varying estimates. Goldman Sachs, for instance, calculated about $1.3 trillion in excess savings as of July, equal to 5% of GDP. Data from Bank of America suggests that increased cash holdings have been relatively evenly distributed across income groups, with median household savings and checking balances up by over 40% compared to 2019 for low-, medium- and high-income households. This distribution reflects the strength of the labor market, allowing people to maintain spending without significantly depleting their accumulated savings.

The U.S. economy, despite braving numerous challenges this year, now faces a convergence of potential hazards that could create significant turbulence. One looming economic threat is the potential escalation of the United Auto Workers strike, which began with around 13,000 workers in three plants and may expand to encompass 38 General Motors and Stellantis parts-distribution centers across 20 states. A broad strike could hamper auto production and inflate vehicle prices, with potential job losses among auto-parts suppliers. Another impending challenge is the possibility of a partial government shutdown if Congress fails to reach an agreement by the end of September. A shutdown could result in furloughs for as many as 800,000 non-essential government workers, leading to reduced spending and government procurement. The resumption of federal student loan payments on October 1 poses an additional threat. This could divert approximately $100 billion from consumers over the next year, impacting retailers and discretionary spending. Higher gasoline prices, driven by surging oil prices, add to these economic pressures, leading to increased consumer inflation and reducing budgets for various expenditures. Collectively, these factors, as noted by Federal Reserve Chairman Jerome Powell, constitute a collection of risks that, when combined, pose challenges to an economy currently displaying significant momentum. While a recession may not be imminent, the convergence of these potential hazards makes for a potentially turbulent fourth quarter and end to the year for the U.S. economy.