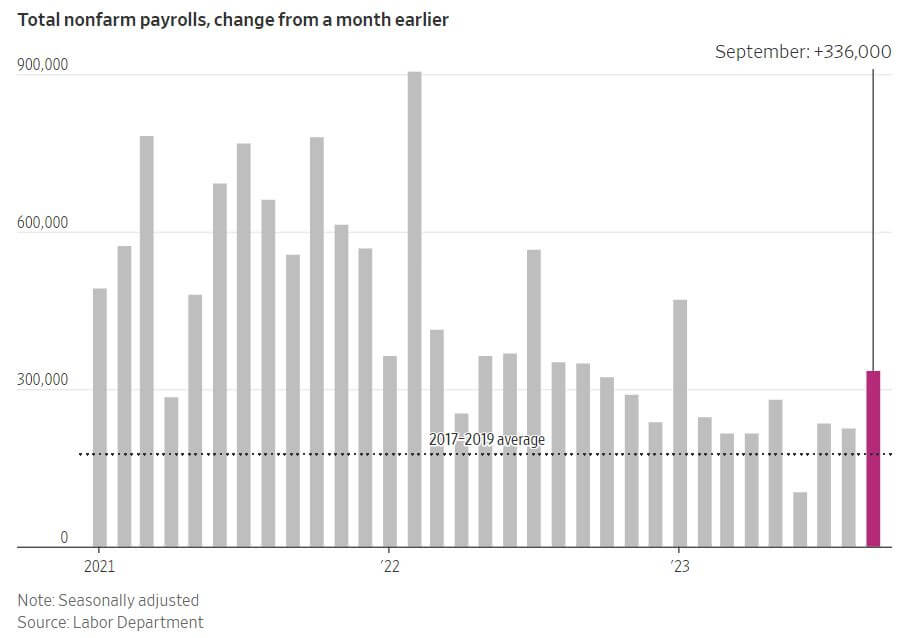

All eyes were on the labor market report out on Friday morning but despite the higher-than-expected gains in non-farm payrolls the equity markets surged higher. The S&P 500 closed up 1.5% while the Nasdaq 100 jumped 2.0% on the day. Positive news on a last-minute deal for the autoworker’s union helped break a four-week losing streak for equities and buoy sentiment on the final trading day. Yields continued their march higher for the week as well after the 10- and 30-year Treasuries touched 2007 highs and settled at 4.9% and 5.1%, respectively. Given recent economic data and market data traders have priced in roughly a 50% change of another rate hike by the end of the year.

U.S. hiring saw a significant surge in September, with employers adding 336,000 jobs, the strongest gain since January. Job growth was stronger than expected and defied predictions of a slowdown due to high interest rates, inflation, student loan repayments, and rising oil prices. The report also highlighted well-rounded hiring across various sectors. The unemployment rate remained at 3.8%, and employers increased wages to attract workers, with average hourly earnings rising 4.2% year-over-year. Employment in sectors like restaurants, hospitals, and trucking returned to pre-pandemic levels for the first time. Last week also saw the release of the Bureau of Labor Statistics' Job Openings and Labor Turnover Survey (JOLTS) for August, which showed that job openings unexpectedly increased to 9.61 million, up from 8.92 million in July. This rise, driven by white-collar positions, demonstrates strong and lasting labor demand. Hiring saw a slight increase, while layoffs remained low. The ratio of job openings to unemployed individuals remained relatively unchanged at 1.5, compared to its peak of 2 to 1 in 2022. Hiring increased slightly after three months of decline, particularly in accommodation and food services, while layoffs remained low, indicating company reluctance to let go of employees. These reports may complicate the Fed's efforts to slow the economy and control inflation, potentially leading to another interest-rate hike. Fed officials will closely monitor consumer inflation data and rising borrowing costs in bond markets. The increase in bond yields poses a risk to the economy, impacting home mortgages, auto loans, and business debt costs. Fed officials have considered another rate increase this year to control inflation, with their next meetings scheduled for October and December.

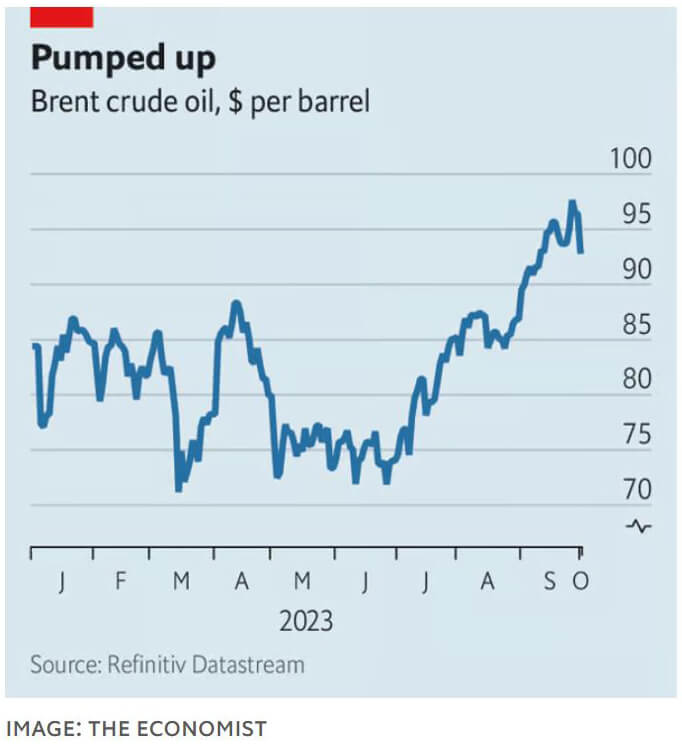

In the first half of the year, Saudi Arabia and OPEC faced falling oil prices due to weak demand and rising interest rates. To counter this, they extended output cuts, but prices continued to drop. However, in July, Saudi Arabia implemented an additional 1 million barrel per day output cut, and oil prices have since risen by 30%. Now, there is uncertainty in the oil market, with prices reaching $97 per barrel before falling back to $92. Some believe the rally might continue, while others think prices will drop below $90 by Christmas. The stakes are high, as dearer oil could lead to inflation and impact the global economy. Bulls argue that oil demand remains resilient, especially in China and the United States. They also note that supply cuts are benefiting producers, and there might be extensions of supply cuts as a result. Meanwhile, American shale production is not filling the gap. Bears, on the other hand, believe that the recovery in China's oil demand has already occurred, and they expect flat demand for the rest of the year. They also worry about the impact of high oil prices on inflation in the United States, which could lead to higher interest rates and a stronger dollar, which could way on the global economy and weaken demand for oil. The short-term outlook may favor the bulls, but the bears expect to gain the upper hand in 2024 as new production arrives, potentially leading to a gradual descent in oil prices. However, the situation remains uncertain, and Saudi Arabia's response to lower prices could influence the market's future dynamics.