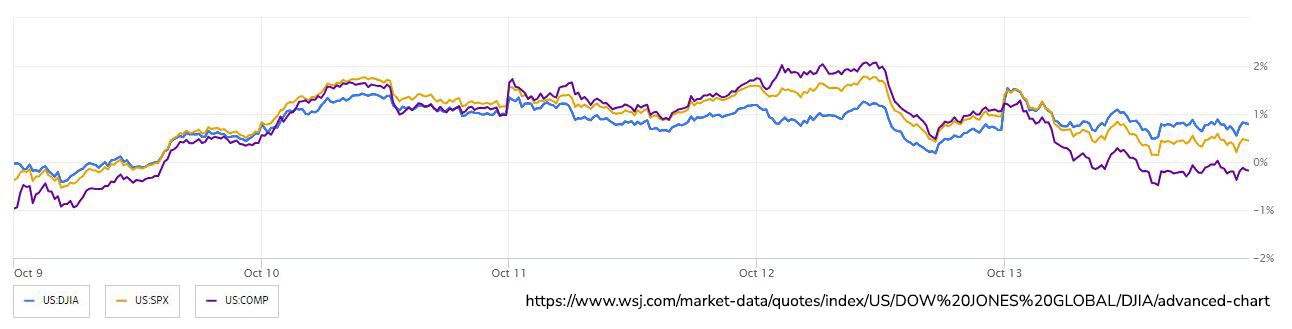

Stocks fell and bonds rose as concerns about Israel's potential ground invasion of Gaza drove traders to seek safety before the weekend. Gold saw a significant surge in value and oil prices rallied. West Texas Intermediate crude oil surpassed $87 per barrel. Big tech stocks experienced a decline, with the Nasdaq 100 falling by over 1%. Boeing Co. dropped due to quality issues with the 737 Max aircraft, while JPMorgan Chase & Co. and Wells Fargo & Co. reported strong earnings, leading to gains. Treasury 30-year yields decreased, unwinding some of the previous session's surge. The yield on 10-year US Treasuries declined eight basis points to 4.62%.

The situation in Israel raised the potential for a broader conflict, possibly involving Iran, which supplies arms and funds to Hamas. This could result in a significant increase in oil prices and a global economic slowdown. A sustained rise in oil prices could further harm the global economy, especially considering the already high stock market valuations. Jamie Dimon, JPMorgan's CEO, warned of significant geopolitical risks amid Israel's preparations for a ground assault on Gaza, emphasizing the potential impact on energy, food markets, global trade, and geopolitical relationships. In the corporate world, Microsoft completed its acquisition of Activision Blizzard, Progressive Corp. showed improved underwriting profitability, UnitedHealth Group Inc. raised its annual profit forecast, BlackRock Inc. saw outflows from long-term investment funds, and PNC Financial Services Group Inc. began reducing its workforce.

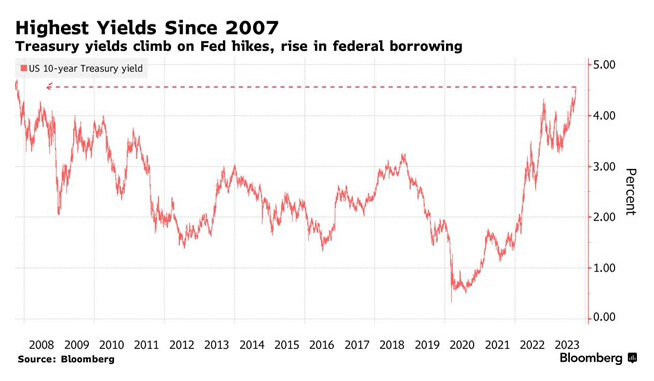

The Federal Reserve's historic cycle of interest rate hikes may be approaching an anticlimactic conclusion due to a sustained rise in long-term Treasury yields. Key central bank officials have indicated that they might cease raising short-term interest rates if long-term rates remain high and inflation continues to moderate. In July, the Fed raised its benchmark federal-funds rate to a range of 5.25% to 5.5%, a level not seen in 22 years. Although officials kept rates unchanged at their recent meeting, they hinted at potential rate hikes in one of their last two meetings for the year. The surge in long-term Treasury yields began after the July rate increase and accelerated following the September Fed meeting. If long-term Treasury yields continue to rise they might obviate the need for further increases in the federal-funds rate. Initially, the increase in long-term rates was attributed to favorable economic news, diminishing expectations of a recession prompting the Fed to lower rates in the first half of the following year. However, it is increasingly evident that factors beyond economic and Fed policy outlooks, such as mounting government deficits, are influencing the rise in rates, which suggests an increase in term premiums (the extra yield demanded by investors for longer-dated assets). Term premiums are challenging to measure precisely, but they appear to account for at least half of the increase in long-dated Treasury yields since late July. Fed Vice Chair Philip Jefferson and other officials have indicated their awareness of the tightening in financial conditions through higher bond yields when deciding on future rate increases. Given these remarks, it appears that the Fed is likely to maintain steady rates at its October meeting. The Fed may wait to assess economic and financial developments before deciding on further rate hikes in December.

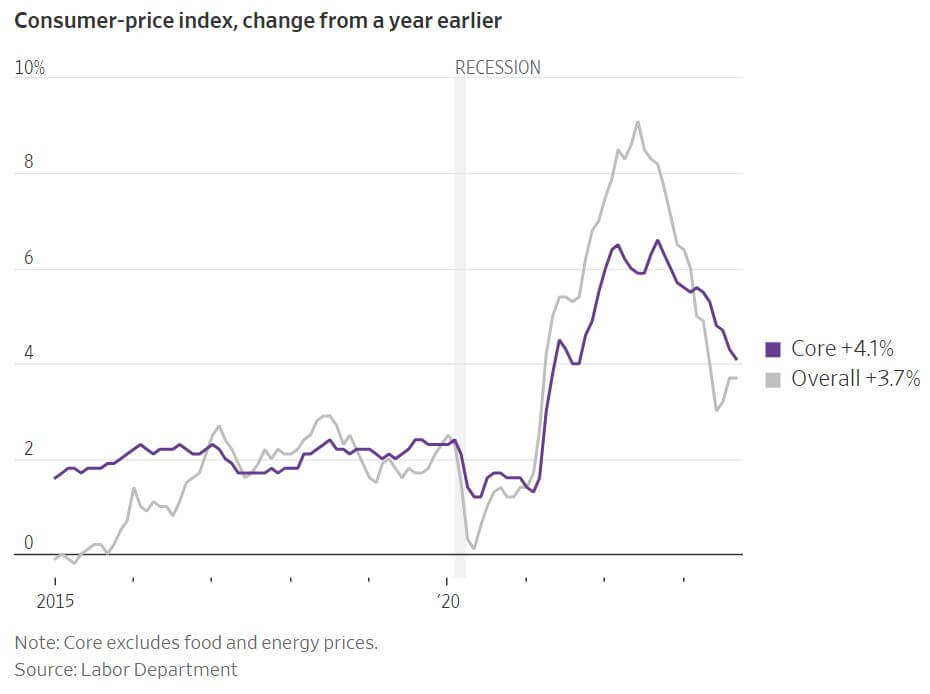

In September, progress in reducing inflation slowed, indicating a challenging path to eliminating price pressures. The Consumer-Price Index (CPI) increased by 0.4% from the previous month and 3.7% from a year ago. When volatile food and energy items are excluded, core prices rose by 0.3% in September and 4.1% over the previous year. Meanwhile, prices paid to U.S. producers (PPI) exceeded expectations in September, with a 0.5% increase in the producer price index for final demand. This was driven by a 5.4% rise in gasoline costs. When excluding food and energy, the PPI increased by 0.3%. Over the year, the overall measure rose by 2.2%. The increase in prices was mainly due to higher energy costs and a significant rise in food prices. Excluding these components, prices for goods only edged up by 0.1%, while service costs increased by 0.3%, primarily led by financial services. Gasoline prices have fluctuated, and housing costs are expected to provide relief from inflation in the coming months. Used car prices have declined.

A recent uptick in oil prices, along with the conflict in Israel, threatens the progress made in controlling producer inflation. Economists are closely watching the PPI report, as it influences the Fed's preferred inflation measure. Federal Reserve officials are considering holding short-term interest rates steady at their upcoming meeting due to the recent rise in long-term interest rates, which could dampen economic growth. They are closely monitoring the inflation situation, and it remains uncertain whether they will continue to raise rates. Worker pay and labor costs are also factors affecting inflation, especially in the service sector. While progress has been made in inflation control, the Fed cannot declare victory yet.