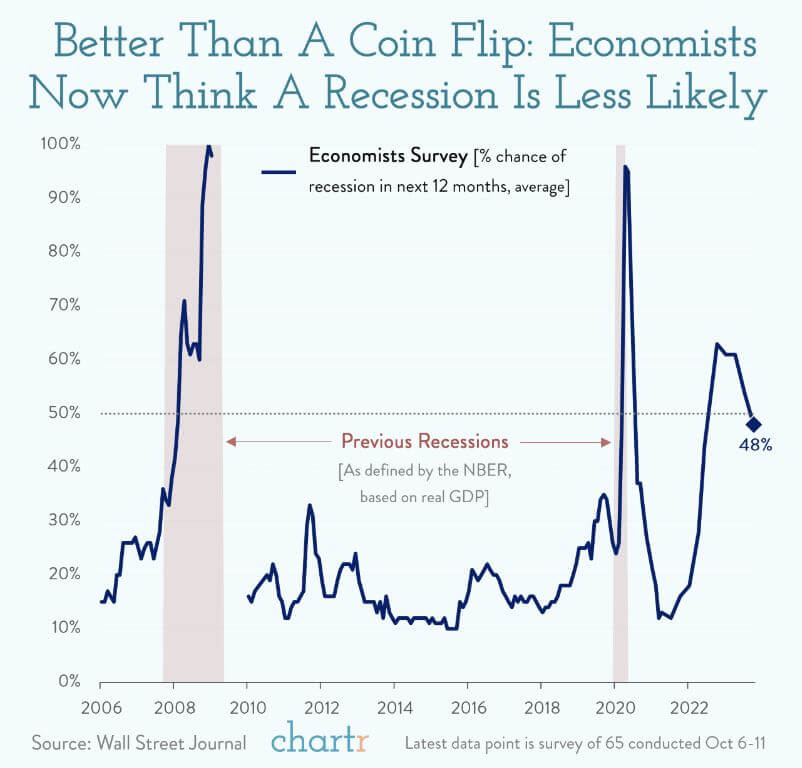

Economists in a recent Wall Street Journal survey are growing more optimistic about the U.S. economy. They have reduced the probability of a recession in the next year from 54% to 48%, marking the first time it's fallen below 50% since the middle of the previous year. This shift is attributed to factors such as declining inflation, the Federal Reserve's decision to stop raising interest rates, and the resilience of the labor market and economic growth surpassing expectations. In the fourth quarter of 2023, GDP is expected to increase by 2.2%, a significant upward revision from the previous forecast of 1%. Although economists have slightly lowered their predictions for next year, they still anticipate continued growth in 2024 and 2025, with the unemployment rate remaining just above 4%. However, the initial half of 2024 may see weak economic growth and job creation due to high interest rates.

Approximately 60% of economists believe the Fed has concluded its current cycle of interest rate increases, and some expect rate cuts in the second quarter of next year as economic growth cools. This overall optimism indicates confidence in achieving a "soft landing," reducing inflation without a recession. Inflation is projected to decrease from 3.7% in September to 2.4% by the end of next year and 2.2% by the end of 2025. Still, economists acknowledge potential challenges ahead, such as rising energy prices due to international conflicts and increased bond yields. While bond yields are expected to ease in the coming months, these developments could pose risks to the economy. Despite these potential hurdles, economists generally give Federal Reserve Chair Jerome Powell positive ratings for his monetary policy, though they criticize his earlier view that inflation would be transitory in 2021.

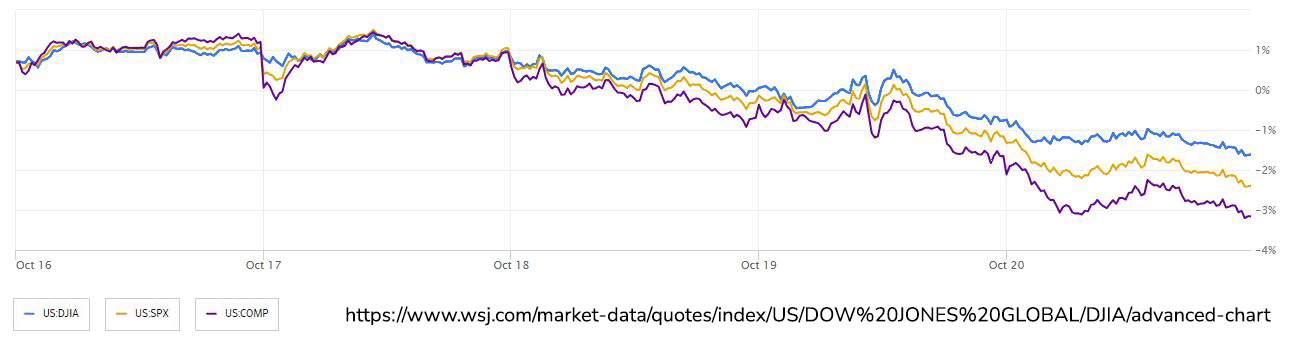

Global markets reacted to the escalating Israel-Hamas conflict, resulting in stock market declines, a surge in bond prices, and a rise in the price of gold. The S&P 500 dropped over 1% on Friday, marking its worst week in a month and breaking through the key 200-day moving average, which is often seen as a sign of potential further declines by technical chartists. Major companies, including Tesla Inc. and American Express Co., saw significant drops in their stock prices. Regions Financial Corp. also suffered losses in the banking sector after warning of further declines in net interest income. Investors sought safe haven assets due to the geopolitical tensions, with Treasury yields retracting from recent increases and gold prices approaching $2,000 per ounce.

Apart from the Middle East crisis, global markets were influenced by rising Treasury yields and concerns about prolonged high interest rates. Federal Reserve Bank of Cleveland President Loretta Mester indicated that the U.S. central bank is nearing the end of its tightening campaign if the economy follows the expected trajectory. Corporate earnings reports were also being closely watched, with a majority of S&P 500 companies beating profit estimates. However, the Middle East conflict and Treasury yields took precedence, causing S&P 500 constituents to move in unison due to broader market fluctuations. Notably, the frequency of over 400 S&P 500 members moving in the same direction during a trading session occurred more frequently in recent weeks, indicating increased market volatility. The Cboe Volatility Index (VIX) futures contracts closed in a pattern known as backwardation, signaling mounting distress among traders and expectations of near-term volatility in the U.S. equity market.

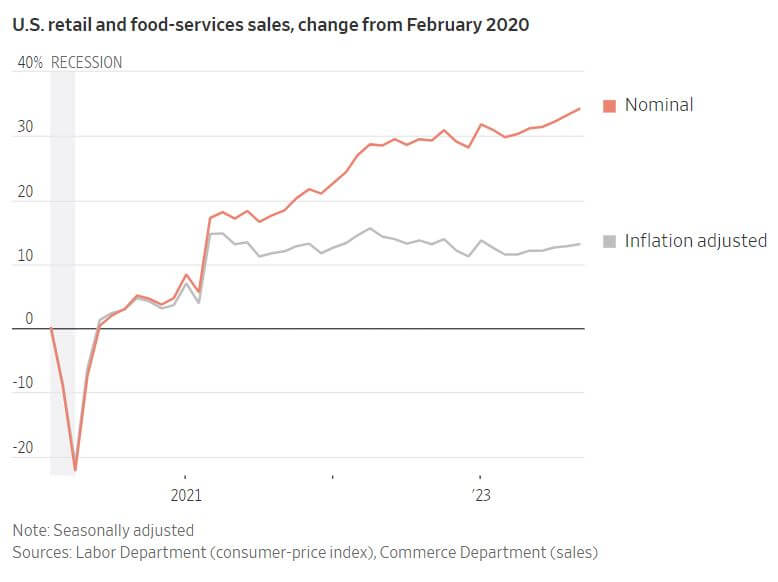

Despite high interest rates, elevated inflation and dwindling pandemic savings, the American consumer is showing remarkable resilience through increased spending. The latest retail-sales report for September revealed a stronger-than-expected 0.7% increase in spending at stores, online retailers and restaurants. This robust consumer behavior contributes to evidence of strong economic growth, which could result in higher interest rates, causing Treasury yields to surge towards yearly highs. The consumer's willingness to spend remains evident in various sectors, including interest-sensitive areas like automotive purchases and more expensive dining experiences. Their broad-based retail spending in September has led some economists to revise their estimates for third-quarter economic growth, with many predicting GDP growth above a 4% annual rate. While consumers increased spending in September, particularly on experiences like dining out, the surge in "revenge travel" is starting to wane, with some budget airlines forced to reduce fares to maintain occupancy. It's important to note that the retail-sales figures don't account for inflation, and a more comprehensive spending report that includes services will be released by the Commerce Department later in the month.

The state of the labor market is expected to be a determining factor in consumer spending in 2024. Higher borrowing costs are anticipated to weaken the job market, but economists are cautiously optimistic that the U.S. can avoid a recession. Although consumer confidence has dipped, the unemployment rate remains low, and wage growth is strong. Signs of financial strain are emerging, with consumers feeling the impact of high inflation and reduced savings. The personal saving rate has significantly decreased, and delinquencies on certain types of consumer debt are on the rise, though most economists are not yet alarmed by this trend. Nonetheless, these indicators are being closely monitored as consumers face numerous financial challenges.