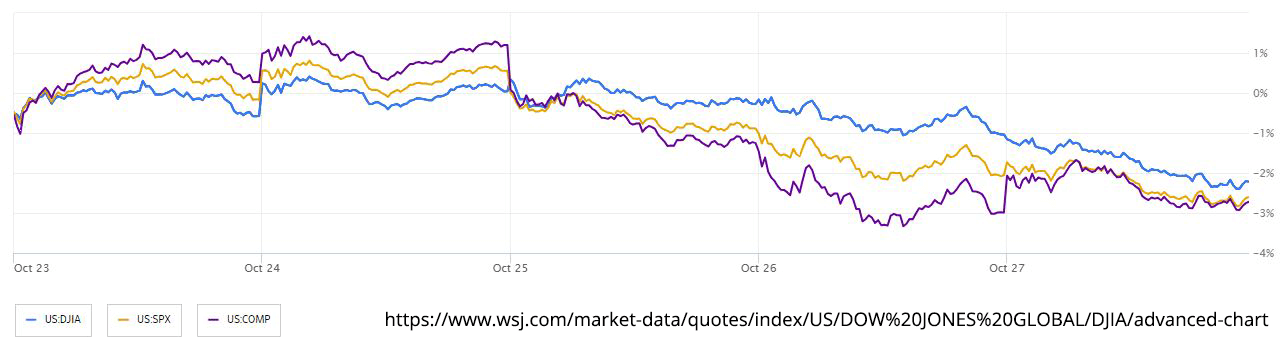

Recent developments in financial markets reflect a turbulent landscape. The S&P 500 index has witnessed a faltering rebound, with the decline extending from its peak in July to reach a significant 10% correction, signifying a challenging period for equities. Concurrently, the prices of key commodities have surged, as oil surpassed $85 per barrel and gold reached $2,000, primarily driven by ongoing geopolitical events. Market volatility has resurfaced due to reports of Israeli forces expanding their activities in Gaza. As a result, the benchmark stock index is approaching its worst weekly performance in a month.

JPMorgan Chase & Co. experienced a decline as CEO Jamie Dimon announced plans to sell shares worth approximately $141 million. In contrast, Amazon.com Inc. and Intel Corp. posted gains in their stock prices following favorable earnings reports. Treasury two-year yields have slightly decreased, as traders have accommodated a higher inflation measure with relative calm, while the value of the dollar has exhibited uncertainty. U.S. stocks are currently enduring their third consecutive month of declines, prompted by concerns stemming from rising bond yields and a persistently hawkish stance adopted by the Federal Reserve. These concerns have been exacerbated by the ongoing war in the Middle East and a somewhat underwhelming corporate earnings season.

Mark Hackett, Chief of Investment Research at Nationwide, attributed the recent market selloff primarily to technical factors, emphasizing that underlying fundamentals remain robust. He anticipates a potential rebound driven by signs of oversold conditions and supportive seasonality. However, a shift in market sentiment may require a catalyst or a period of capitulation. Notably, over two-thirds of stocks in the S&P 500 are trading below their 200-day moving averages, indicating widespread challenges in stock prices, particularly as companies struggle with lackluster earnings in the face of high interest rates and steadily increasing bond yields.

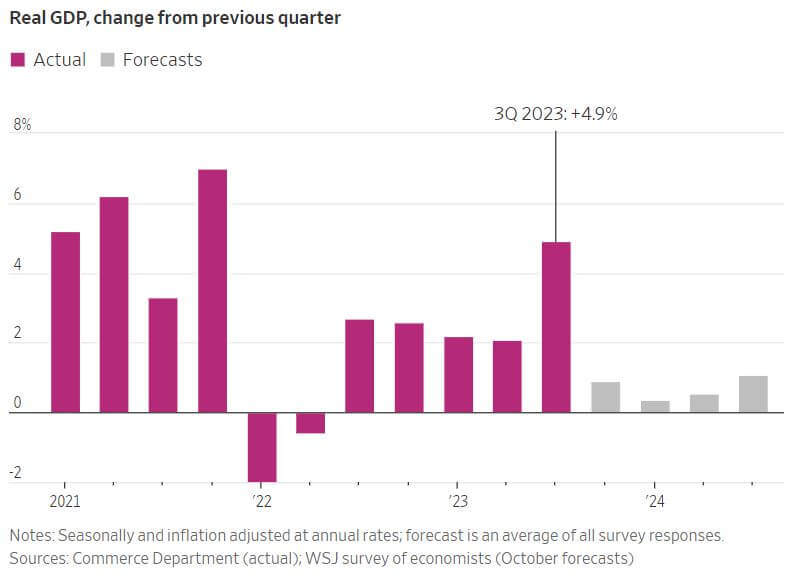

In the third quarter of 2023, the U.S. experienced robust economic growth with a 4.9% annualized increase in Gross Domestic Product (GDP), a rate significantly exceeding earlier forecasts and the fastest since late 2021. This surge was primarily driven by increased consumer spending, which defied expectations, despite the Federal Reserve's interest rate hikes aimed at curbing inflation and slowing economic growth. Consumer spending rose by 4.0% in the third quarter, supported by a strong job market and savings accumulated during the COVID-19 pandemic. The Federal Reserve, in response to high inflation, raised the federal-funds rate to a range between 5.25% and 5.5% in July. Inflation has eased from its peak in June 2022, and prices excluding volatile food and energy categories increased by 2.4% in the third quarter, only slightly above the Fed's 2% target.

This combination of moderating price increases and a resilient economy has raised hopes for a "soft landing," where inflation decreases without triggering a recession. However, the economy's resilience may face challenges in the near future, including rising long-term interest rates, geopolitical conflicts in Ukraine and the Middle East, the potential for a government shutdown, and prolonged labor strikes. The increase in the yield on the 10-year Treasury note to 5% may impact borrowing costs, potentially slowing down the economy. Residential investment, while improving, could be impacted by higher mortgage rates. Business investment has remained flat, and higher interest rates may deter borrowing and spending. Personal income, adjusted for inflation, declined during the quarter, and Americans' savings decreased, potentially affecting future spending. It is expected that consumer spending will slow down in the fourth quarter due to the potential impact of higher interest rates and other economic headwinds.

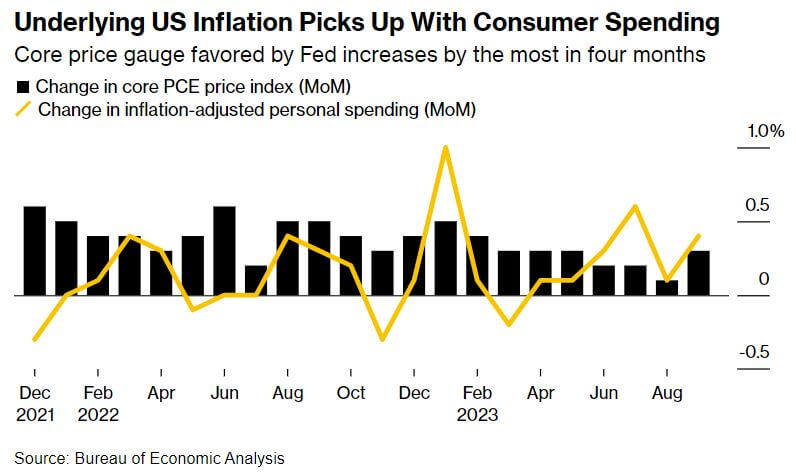

In September, the Federal Reserve's preferred measure of underlying inflation, the core personal consumption expenditures (PCE) price index, experienced a notable increase of 0.3% compared to the prior month, marking a four-month high. Concurrently, real consumer spending surged by 0.4%. Of particular concern to officials are service-sector prices, which rose by 0.5%, the most significant increase since January. Services inflation, excluding housing and energy, also accelerated to 0.4% from the previous month's 0.1%. Consumer spending was driven by purchases of both goods and services, including cars, prescription drugs and international travel. The labor market's strength continues to support household spending, although other factors, such as a significant increase in household wealth and lingering pandemic-era savings, have also played a role. This suggests robust momentum as the fourth quarter approaches, although economists anticipate a potential slowdown in consumer spending in the upcoming months. Despite a 0.4% rise in wages and salaries, real disposable income has fallen for the third consecutive month, leading consumers to save less to sustain their spending. The saving rate dropped to 3.4%, the lowest this year, raising concerns about the sustainability of spending at this pace throughout the year. Nonetheless, strong data has prompted the Fed to remain vigilant in considering further interest-rate hikes. Despite these inflation and spending figures, it is widely expected that policymakers will leave the benchmark interest rate unchanged at their upcoming meeting, largely due to concerns about a rapid increase in borrowing costs.