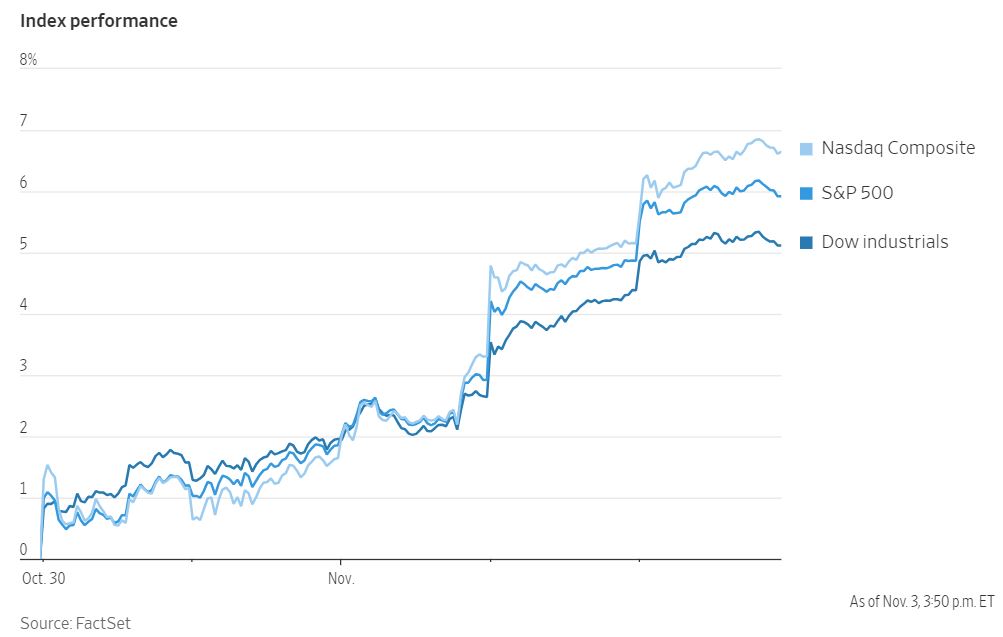

In the financial markets, a confluence of factors has led to significant shifts in asset prices and market sentiment. Stocks experienced a notable uptick in value last week, while bond yields exhibited a downward trajectory. These developments stem from indicators suggesting a moderation in both the labor market and the services sector, reinforcing the prevailing belief that the Federal Reserve has concluded its cycle of interest rate hikes. This bullish trend has coincided with a substantial decline in the VIX, commonly known as the "fear gauge," which has seen its most significant five-day drop in nearly two years. Meanwhile, US Treasury yields have decreased across the yield curve, with two-year yields declining by 16 basis points to 4.83%. The US dollar has experienced its most significant depreciation since July, contributing to the overall favorable market conditions. Perceived credit risk has also diminished, as reflected by two North American credit gauges. Additionally, oil prices have dipped below the $81 per barrel mark, indicative of a complex set of factors impacting the energy market. Market participants have adjusted their expectations regarding Federal Reserve actions. Swap markets now indicate a mere 20% likelihood of another rate hike by January, while rate cuts have been fully priced in for as early as June. It is important to note that while the US economy has displayed initial signs of weakness, market sentiment remains resolutely optimistic. This "not too hot/not too cold" economic backdrop has reassured investors who were previously concerned about an overheating economy. The prevailing market sentiment suggests that investors are relieved by the Federal Reserve's recent actions and the economic data, even though challenges persist in the form of corporate profit outlooks and ongoing volatility.

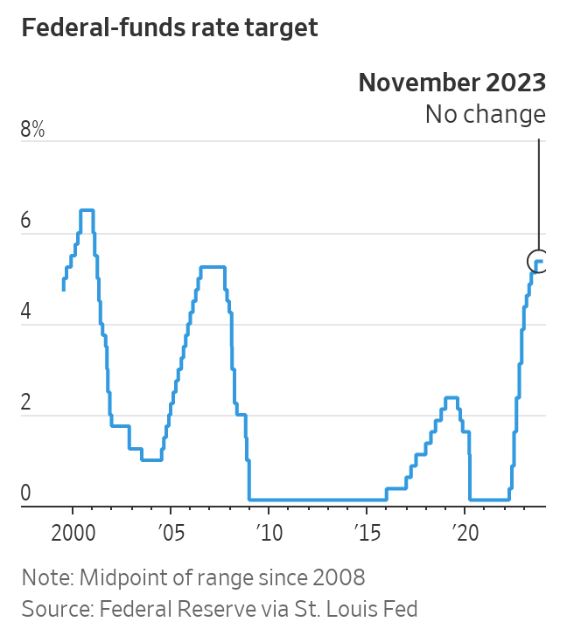

The US Federal Reserve maintained its current interest rate at a 22-year high at its most recent meeting and indicated a potential willingness to increase rates in the future to combat persistent inflation. Officials characterized recent economic performance as robust and emphasized the potential negative impact of rising long-term interest rates on economic activity. This decision comes amid rising concerns in financial markets, as the 10-year Treasury yield has increased substantially since the last rate hike, which occurred in July, bringing the benchmark federal-funds rate to a range between 5.25% and 5.5%. Notably, the Fed has now refrained from raising rates for two consecutive meetings. A continued deceleration in inflation might lead to a continued pause in rate hikes, while any acceleration in price pressures could prompt them to raise rates once more. Since their last meeting in July, the economic landscape has been influenced by three significant factors with varying implications for monetary policy. Firstly, economic activity has exceeded expectations, with consumers increasing spending and employers expanding payrolls. Second, inflation has moderated, with core inflation, excluding food and energy prices, dropping from its peak of 5.6% to a 2.8% annualized rate over the April-to-September period. Thirdly, financial conditions have tightened due to a rapid increase in long-term Treasury yields, resulting in higher borrowing costs for households and businesses. The Fed faces a delicate balancing act as sustained economic growth could raise concerns about potential overheating, given the economy's resilience to rapid rate hikes and other stressors. Fed officials are cautious not to overdo rate hikes to avoid an unnecessary economic downturn, while also being wary of allowing inflation to exceed their 2% target. The debate within the Fed varies, with some advocating for a more gradual approach in the face of slowing inflation and wage growth, while others argue for additional rate hikes as a precaution against the possibility of economic and inflationary resilience.

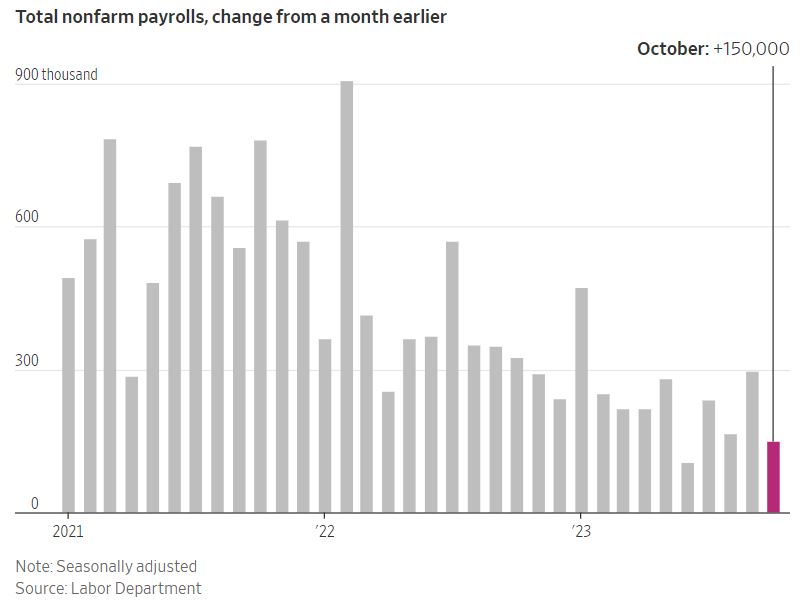

The US experienced a significant deceleration in hiring in October, indicating a cooling economy after a robust summer. According to the Labor Department, US employers added 150,000 jobs in October, a notable drop from the previous month's revised gain of 297,000, marking the smallest increase since June. The United Auto Workers strike played a role in this slowdown, with automakers reducing their payrolls by approximately 33,000 workers. The unemployment rate also inched up from 3.8% to 3.9% over the previous month. Wage growth also showed signs of cooling as employers hired fewer workers. Average hourly earnings increased by 4.1% compared to the previous year, down from the 4.3% growth observed in September. The labor force participation rate slightly decreased from 62.8% in September to 62.7% in October. Some experts, like Andrew Hunter, Deputy Chief US Economist at Capital Economics, view this report as an indication that the third-quarter economic strength is likely to unravel in the fourth quarter. With wage growth slowing down, it becomes increasingly difficult to envision the Fed raising interest rates further. The surprising resilience of the US economy in 2023, despite forecasts of a recession and higher borrowing costs, can be attributed to the strong labor market, which continued to create jobs. This robust job market encouraged consumer spending, contributing to GDP growth in the third quarter, which was the fastest since 2021. Forecasters and the Federal Reserve now expect the economy to avoid a recession and gradually slow down to keep inflation in check. The strong labor market has enticed more people to seek employment, resulting in the highest workforce participation rate in over two decades. This trend could make it easier for employers to find workers, helping to maintain wage growth and inflation at manageable levels. Fed Chair Jerome Powell cited the cooling labor market as a reason for a potential pause in rate hikes. He highlighted increased labor-force participation and immigration as positive signs that the economy could thrive without significant price increases.