The S&P 500 Index is generally thought to be an appropriate indicator for a reading on the general state of the US stock market. However, the dominance of seven prominent technology companies increasingly challenges that rule of thumb. Collectively referred to as the "Magnificent Seven," this group of tech giants includes Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Despite their substantial market value and dynamic presence, considering them emblematic of the broader market is an oversimplification. Consider the hypothetical concept of a "S&P 493 Index," a term coined to encompass the 98.6% of companies in the S&P 500 that do not belong to the Magnificent Seven. This new index features more mature and diverse entities such as Berkshire Hathaway, Eli Lilly and JPMorgan Chase. Unlike the tech behemoths, these companies, while not reaching trillion-dollar valuations, are characterized as successful and resilient, offering a counterbalance to the youthful and rapidly growing nature of the dominant tech players. The S&P 493 was resilient during the 2022 market crash due to the robust and established business models of its constituent companies, falling just 12% in 2022 while the Magnificent Seven dropped by 41%. However, the performance differential between the two groups reversed in 2023, with the Magnificent Seven gaining 52%, while the S&P 493 has fallen 2% YTD. This stark divergence raises questions regarding the suitability of the S&P 500 as a benchmark for the broader stock market, highlighting its dominance by seven distinct stocks. Despite this, many investors opt for index funds precisely to capture gains without being overly concerned about the composition. However, at this point a deeper examination beyond the headline index into the rest of its constituents is necessary for a more nuanced understanding of America's stock market composition and performance.

The stock market has continued its upward momentum in November, driven by strong performance from tech giants. The S&P 500 reached the significant level of 4,400 and the Nasdaq 100 saw a gain of over 2%, with notable companies like Microsoft and Nvidia performing well. This positive trend is attributed to a rebound in influential stocks, a relatively stable bond market and no surprising statements from Federal Reserve speakers. Investors have been optimistic this month, as they believe interest rates may have peaked, leading to a decline in bond yields. Despite concerns about inflation, corporate outlooks and geopolitical developments, the market has continued to rise. Market experts point to factors like oversold conditions, solid earnings and a decrease in interest rates as key drivers of this recovery. If the S&P 500 breaks out above 4,400, it could potentially reverse its recent downtrend and indicate that the correction lows were set the previous month. A calmer session in the Treasury market, with little change in 10-year yields, contributed to the stock market’s gains. Federal Reserve officials’ remarks were closely monitored, with different opinions on the need for further interest rate hikes. Inflation concerns persist as consumer long-term inflation expectations have reached a 12-year high. However, investors have become less reactive to data in recent weeks, with reduced market volatility. The caution that characterized equity markets in the past three months has now shifted to optimism regarding year-end expectations of a decline in US bond yields. Global stocks have seen significant inflows, although cash remains a preferred asset class. Bitcoin ended the week near $37,000, its highest level since May 2022. Oil dropped for the third straight week, with WTI closing at $77.25 per barrel.

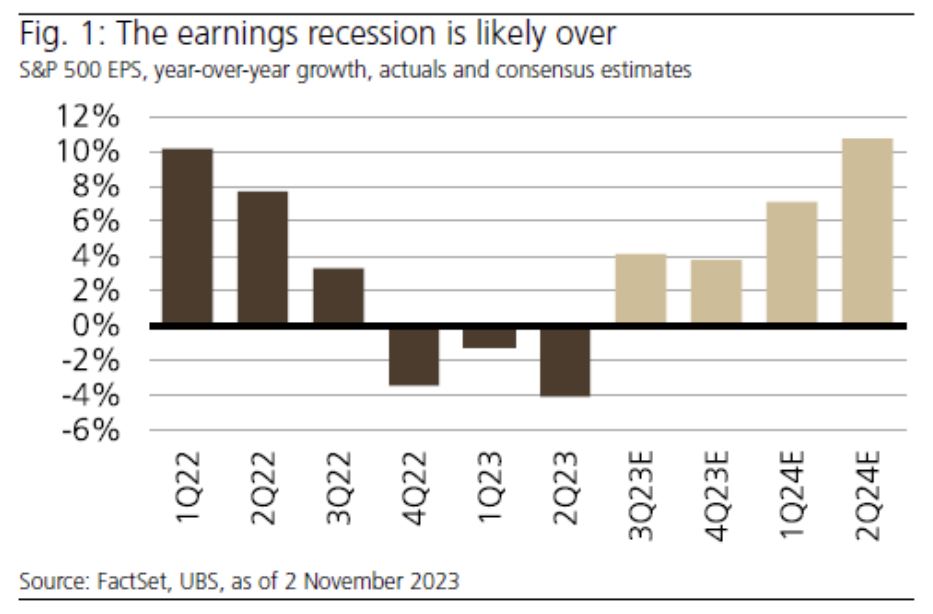

After three consecutive quarters of year-on-year profit declines, the S&P 500 exhibited earnings growth in the third quarter, a trend that Wall Street anticipates will persist. Notably, David Lefkowitz of UBS asserts that the earnings recession has come to an end. However, while corporate profits have rebounded, the corporate sector is not synonymous with the U.S. economy, which is forecasted to slow after rapid growth in Q3. Earnings have lagged behind GDP growth for several consecutive quarters, largely attributed to the transition from goods to services. Lefkowitz underscores a key distinction: S&P 500 profits are tilted more toward goods than services compared to the composition of GDP. Therefore, the resurgence in goods activity hinges partially on the health of consumer spending. Companies, unlike the broader economy in the short term, benefit from cost-cutting measures, leading to margin expansion. This phenomenon has transpired without significant job cuts this year, which further bolsters the recovery of corporate profits. However, expectations for sales and earnings in the current quarter have been markedly revised downward, though that situation is partly attributed to unique issues faced by pharmaceutical companies like Pfizer and Merck, who are facing weaker demand than expected for COVID-19 vaccines. A substantial economic downturn, although not currently integrated into most analysts' forecasts, could alter the trajectory for corporate profits. Investment banks can now utilize "big data" tools to analyze earnings call transcripts for trends. Notably, they have found a discernible trend of mentions of "reshoring," which involves the relocation of offshore jobs and production capacity back to the U.S. This practice, while initially denting short-term profits and potentially increasing inflation, is anticipated to foster long-term domestic growth by boosting investment. In earnings calls, chief executives have also been raising concerns regarding higher financing costs. This implies that monetary policy is beginning to take effect, suggesting that higher interest costs may impinge on profits. Nevertheless, there is a prevailing belief that companies can still generate profits despite the burden of higher interest rates, although this outlook is subject to scrutiny.