Following a remarkable $3 trillion surge in November, the S&P 500 is now just shy of its all-time high. The index's impressive 9% climb in November, a rarity since 1928, represents its most substantial monthly gain since July 2022. Recent data indicates a cooling in US consumer spending, inflation, and labor market activity, supporting the belief that economic growth is gradually decelerating. The core personal consumption expenditures price index, a key measure of underlying inflation preferred by the Federal Reserve, aligned with economists' expectations. Sonu Varghese, a global macro strategist at Carson Group, suggests that these developments are likely to reinforce expectations of an impending monetary policy shift, with at least one rate cut expected in the first half of 2024. The Bloomberg Intelligence Economic Regime Index is now indicating a potential easing of America's macroeconomic challenges, adding a favorable perspective for equity optimists. While it signals potential economic weakness, as long as it remains above its lows, the outlook is positive for the S&P 500, according to Gina Martin Adams, chief equity strategist at Bloomberg Intelligence. Traders are closely monitoring statements from US officials, including Fed Bank of New York President John Williams and his San Francisco counterpart Mary Daly. Williams suggests the benchmark lending rate is at or near its peak, emphasizing a restrictive policy stance. Daly, while stating that rates are in a "very good place" to control inflation, is not considering cuts and deems it premature to determine if hikes are concluded.

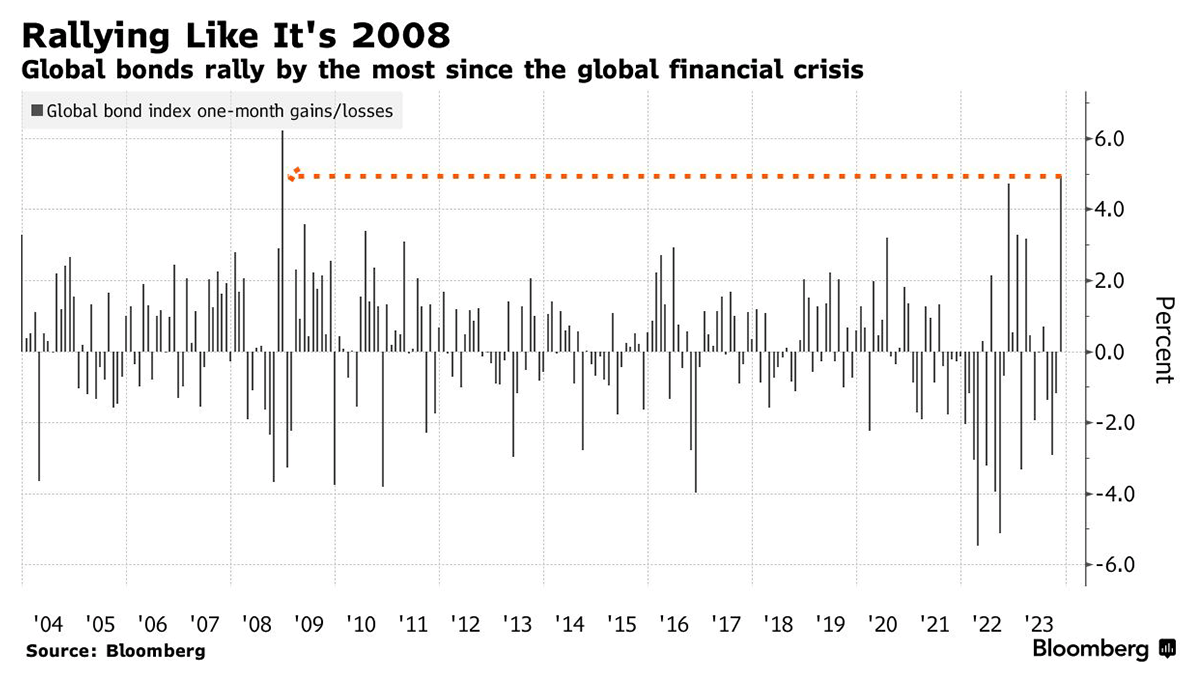

Global bonds are experiencing their most significant surge since the 2008 financial crisis, with a Bloomberg measure of global sovereign and corporate debt delivering a 4.9% return in November, marking the largest monthly gain since December 2008. This rally is attributed to growing speculation that major central banks, particularly the Federal Reserve, have concluded their interest rate hikes and are poised to begin cutting rates next year. Market expectations reflect a full percentage point reduction in the US in 2024 , commencing in June. Federal Reserve Governor Christopher Waller's recent comments expressing a dovish outlook have reinforced bets on rate cuts, surprising some given his previous hawkish stance. This shift signals a potential end to the Fed's tightening cycle. Treasuries have extended their gains, with US 2- and 10-year yields decreasing, while Australian and European bonds also experienced notable drops in yields. The European Central Bank is also anticipated to implement rate cuts, with markets pricing in a full percentage point of easing next year, starting in June. However, some market participants, including Justin Onuekwusi, Chief Investment Officer at St. James’s Place Plc, caution that the market may be overly optimistic, suggesting central banks might not ease policy as early as expected. The current bond rally marks a turnaround in a volatile year for bonds, with the Bloomberg Global Aggregate Total Return index rebounding from a mid-October low to a 1.4% gain for 2023. This shift in central bank expectations has benefited corporate bonds, as spreads on investment-grade global company debt are at their lowest levels since April 2022. The optimism about a soft landing for the US economy has led to increased demand for corporate bonds, causing their average yield to retreat to around 5.3%, down from nearly 6% in October, the highest level since 2009. This trend is further evidenced by a JPMorgan survey indicating that active investors are the most bullish they've been in the market since 1991.

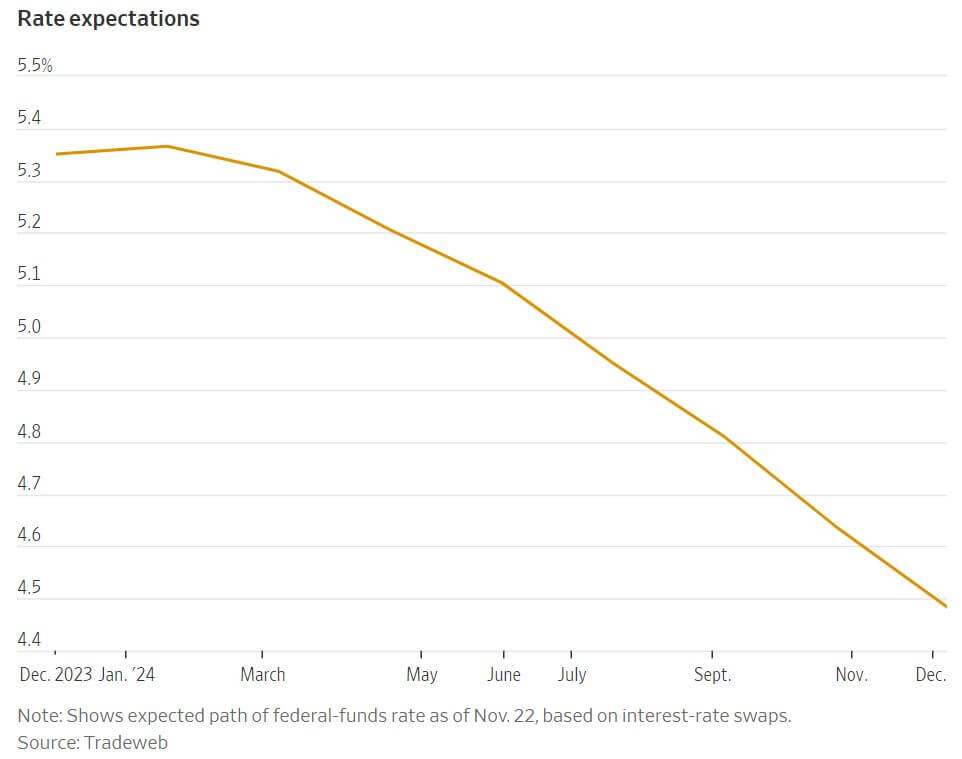

Investors are increasingly betting on a shift in the Federal Reserve's monetary policy, indicating a greater likelihood of rate cuts in the coming months rather than further rate hikes. This sentiment is reflected in interest-rate futures, with a significant rise in the probability of a quarter-of-a-percentage point rate cut by the Fed's May 2024 policy meeting, reaching around 60% compared to 29% at the end of October. However, there is a divergence in expectations, with some traders preparing for a range of outcomes, from the Fed taking no action to aggressive rate cuts. Economic data, including weaker-than-expected purchasing managers' surveys and a slight increase in the unemployment rate, contribute to the uncertainty. Rob Waldner, fixed income chief strategist at Invesco, acknowledges an increased threat of recession but maintains the base case that the Fed will enact insurance cuts without a downturn. Investors caution that the possibility remains that the Fed may not cut rates in 2024, potentially leading to a rise in bond yields. The resilience of the U.S. economy over the past few years and the Federal Reserve's history of surprising investors by raising rates higher than expected contribute to this cautious outlook. The bond market's recent rally, lowering the 10-year yield below 4.5%, began on November 1 when the Treasury Department increased auction sizes of longer-term bonds less than anticipated. This reassured investors that yields had risen disproportionately to economic fundamentals, making the decline in yields more welcome. While Fed officials have consistently stated that rate cuts are not imminent, they have signaled a willingness to lower rates once confident that inflation will reach their target. Fed Chair Jerome Powell has emphasized that the timing of rate cuts will depend on economic conditions. Investors' positioning on rates reflects a belief that the Fed may cut rates by less than 1 percentage point next year, but the wager is made in anticipation of the possibility of even larger cuts. Comparisons with past recessions, where the Fed typically cut rates by 3 to 4 percentage points over a year, suggest that the perceived chance of a recession in 2024 is around 20%, factoring in bets on more modest insurance cuts.