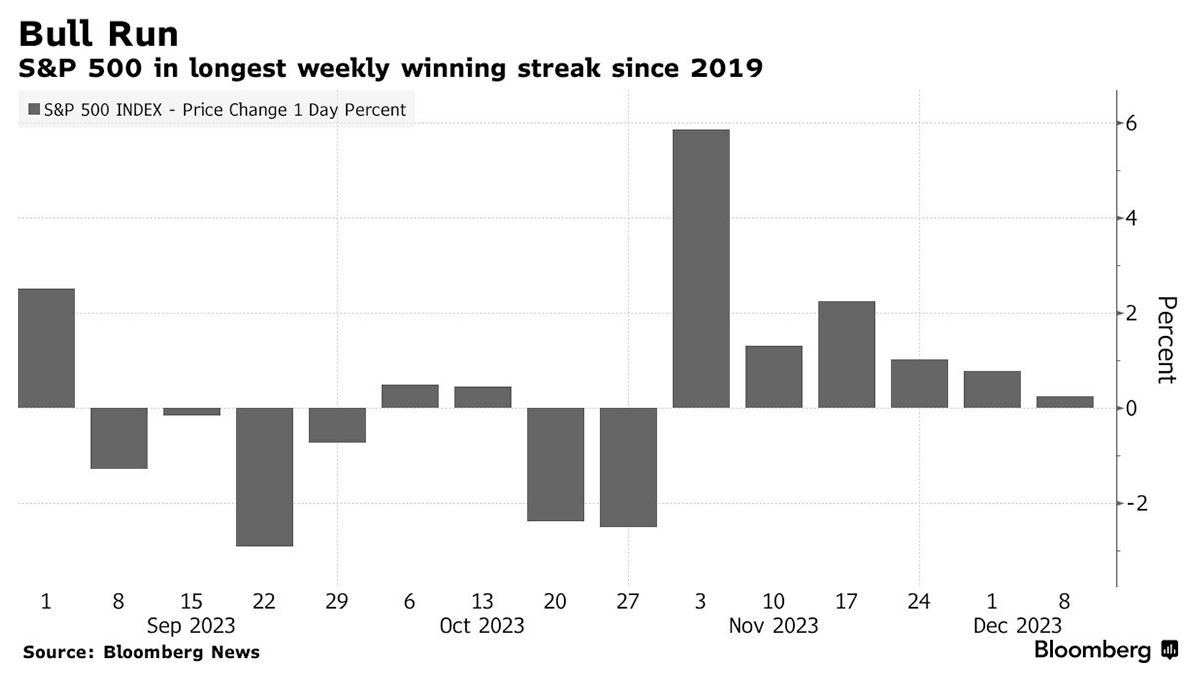

The prevailing sentiment on Wall Street is that while economic strength diminishes concerns of a hard landing, it also implies that the Federal Reserve might need to maintain higher interest rates for an extended period. The jobs report released on Friday came in somewhat stronger than expected, with the US economy continuing to exhibit strength. Market participants are reassessing expectations as a result, with the narrative shifting from anticipating rate cuts to acknowledging the Fed's potential to maintain higher rates for a more extended period. The recent decline in inflation and employment data had prompted expectations of rate cuts, but the strong economic readings have prompted a reevaluation. The S&P 500 has achieved its sixth consecutive week of gains, marking its longest winning streak since November 2019. The VIX, Wall Street's fear gauge, hovers near pre-pandemic levels. However, the flip side is that bond traders are now compelled to scale back their bets on rate cuts in 2024, leading to a rise in yields. The yield on the two-year US Treasury note rose 12 basis points on Friday to 4.72%. Interest rate swaps contracts imply that the probability of an interest rate cut in March dropped to 40% from over 50% earlier in the week. Despite the market initially rallying on the rate-cut trade, some believe that hopes have gone too far, considering the continuous strength of the U.S. economy. Investors are cautious about not overestimating the potential for rate cuts in 2024, with markets now pricing in around 110 basis points of cuts next year compared to the previous 125 basis points. The upcoming week is anticipated to be busy, with key economic readings, Treasury auctions, and the final Fed meeting of the year. Fed officials are expected to maintain borrowing costs at the highest level in two decades. There's a recognition that the Fed, despite better-than-expected data releases, may continue to adopt a cautious approach and not declare victory on quelling inflation. Despite signs of a potential soft landing, confidence in this outcome is not absolute.

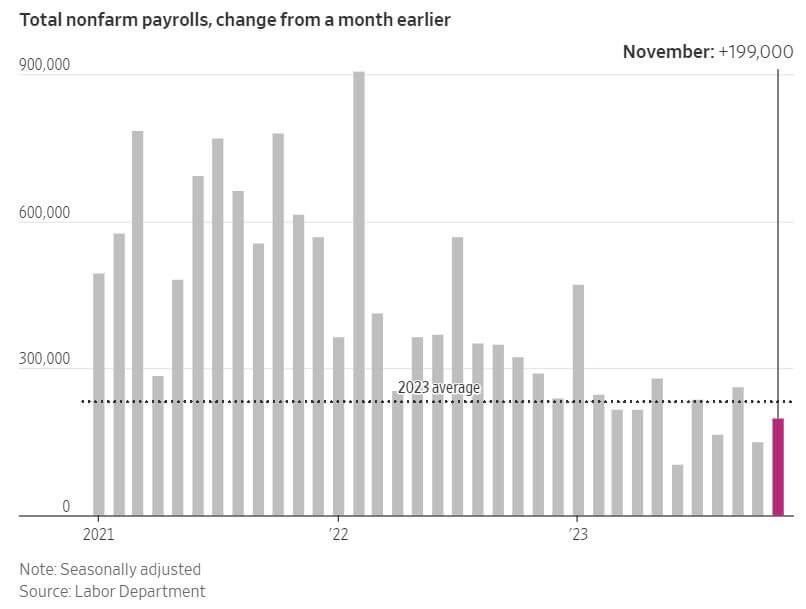

In October, US job openings declined to 8.7 million, marking the lowest level since early 2021, as reported by the Bureau of Labor Statistics Job Openings and Labor Turnover Survey (JOLTS). This decrease, compared to the previous month's 9.4 million, was more extensive than anticipated and spanned various sectors, signaling a gradual cooling in the labor market, aligning with the Federal Reserve's desired trend. The ratio of job openings to unemployed individuals decreased to 1.3, the lowest since mid-2021, indicating a less tight labor market. The data also highlighted stabilization in the quits rate, which measures voluntary job-leavers as a share of total employment. After reaching over four million per month last year, the quits rate has held steady for a fourth consecutive month at its lowest level since early 2021. The JOLTS data further showed historically low layoffs and a slight easing in hiring. A parallel report revealed a slowdown in inflation within the service sector, indicating movement toward the Federal Reserve's dual mandate of employment and price stability. Meanwhile, the Labor Department reported a seasonally adjusted addition of 199,000 jobs in November, a pace slightly slower than earlier in the year but in line with pre-pandemic gains. Adjusting for recent auto-worker strikes, the net job gain in November was approximately 169,000, marginally cooler than October's 180,000. The overall employment landscape remains robust, with the unemployment rate dropping to 3.7%, dispelling concerns raised in October when it briefly climbed to 3.9%. The addition of half a million Americans to the labor force in November, coupled with increased monthly wage growth of 4%, paints a positive picture. This overall trend suggests progress towards a soft landing in the labor market, characterized by a cooling of job openings, stability in quits and layoffs, and a better balance between demand and supply.

Gold briefly touched a record high of $2,135 per troy ounce last week, before falling back by 6%. The World Gold Council attributes the spike to short-term technical trading rather than fundamental factors like central bank gold buying. Despite central bank purchases, high gold prices have led to a reduction in jewelry demand, and exchange-traded funds have sold over 100 metric tons of physical gold this year. Additionally, mine production has reached a record 1,267 tons, and recycling has increased by 8% to nearly 300 tons. The surge in gold prices coincided with a similar rise in Bitcoin, with both being considered by some as safe-haven assets in times of economic uncertainty. Bitcoin climbed above $40,000 for the first time in 20 months last week and added to those gains to end the week in the range of $44,000. Options traders are increasingly placing bullish bets on Bitcoin reaching $50,000 by January. This surge in optimism is attributed to the anticipation that the Securities and Exchange Commission (SEC) will approve the establishment of exchange-traded funds (ETFs) directly holding Bitcoin, a development expected in January. In contrast, oil prices have seen a sharp decline recently due to a number of factors, including concerns about oversupply, momentum trading, and lower market volumes. Both the US benchmark West Texas Intermediate and the global benchmark Brent experienced significant declines, with Brent's open interest and trend-following algorithms contributing to the acceleration of the fall. Despite a US government report showing a decrease in crude stockpiles, traders appear unconvinced, and the market's weakness is highlighted by Saudi Arabia reducing its official selling prices to Asia. The Organization of Petroleum Exporting Countries (OPEC) and its allies announced deeper output cuts, but skepticism persists among traders regarding the members' commitment to implementing the reductions. West Texas Intermediate crude oil ended the week at $71.20 per barrel.