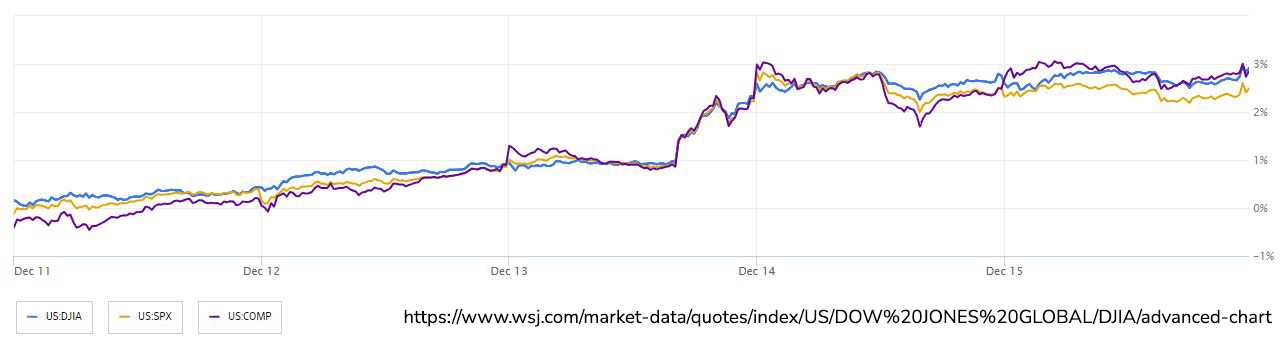

Investors' growing confidence in a perceived peak in interest rates led the Dow Jones Industrial Average to a new record high last week above 37,000. The Nasdaq 100 also hit a new high, last reached two years ago. Simultaneously, the S&P 500 reached its highest level since January 2022, and the yield on the 10-year U.S. Treasury note dropped below 4% for the first time since August in a substantial decline from where it started the week. This surge commenced after the Federal Reserve's decision to maintain steady rates and project three quarter-point rate cuts next year. The optimism stems from the hope that the economy will slow sufficiently for rate cuts without tipping into a recession. Lower rates, if achieved without economic repercussions, would benefit stocks and bonds by providing cheaper financing for various entities, including companies and households. Despite these positive trends, doubts linger about the rally's sustainability. Concerns include the perception that economic growth remains too robust to warrant the anticipated number of rate cuts. Some worry that the market's optimistic conditions might obviate the need for cuts by doing the Federal Reserve's work. Last week’s rally included rate-sensitive sectors such as banks and small-cap companies, as well as large cap technology firms. Despite the uncertainties, investors are encouraged by the easing of financial conditions and the potential for a favorable market outlook.

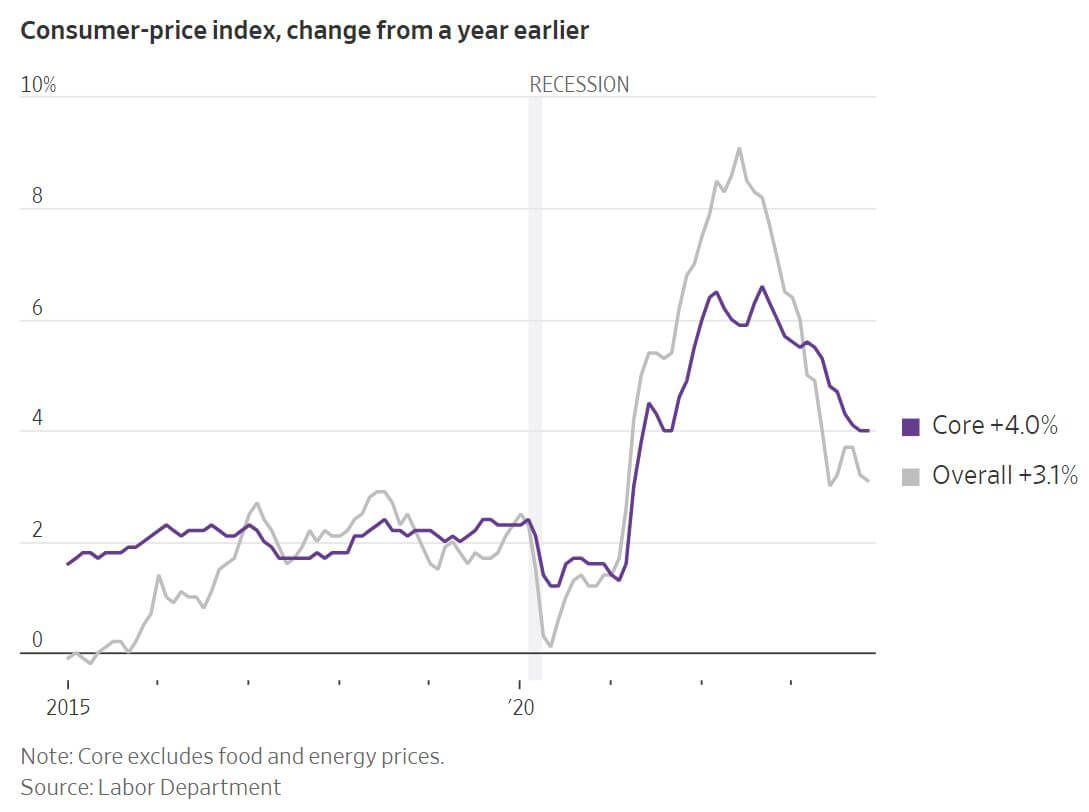

The consumer-price index (CPI) rose 3.1% in November from a year earlier, a modest decrease from October but still above the 2% target set by the Federal Reserve. This stabilization suggests that while inflation has improved compared to its peak earlier in the year, it remains a concern, hindering hopes for immediate Federal Reserve rate cuts. Core prices, which exclude volatile components like food and energy, increased by 4% in November from a year earlier, maintaining the same pace as October. However, caution persists within the Federal Reserve. There is a historical pattern of inflation appearing to decline only to reaccelerate, prompting the Fed to avoid premature actions that could impact the economy negatively. Consumer sentiment is gradually improving as long-term inflation expectations decrease and Americans become more optimistic amid slowing price gains. Housing costs continue to exert upward pressure on inflation, with the shelter index rising by 0.4% last month and 6.5% over the past year. If housing costs cool in the coming months as expected, overall inflation could dip below 3% for the first time since the pandemic. The dichotomy between goods and services is evident, with smoother supply chains and restrained consumer spending contributing to slowed price increases for goods. However, certain service categories, such as healthcare and auto repair, continue to experience price gains.

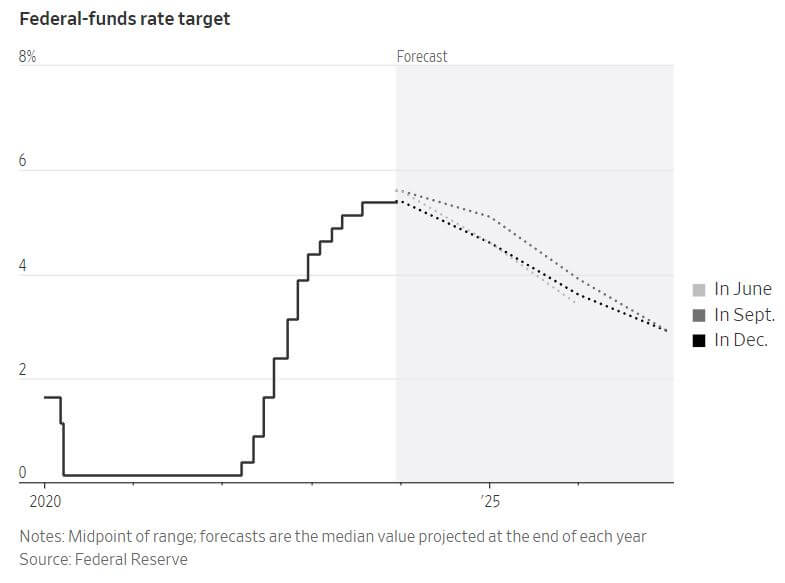

The Federal Reserve, after its two-day meeting, decided to maintain interest rates while signaling that inflation has improved more rapidly than anticipated. This stance opens the door to potential rate cuts in the coming year. The majority of Fed officials projected three interest rate cuts for 2024 in a surprisingly dovish shift from the most recent Fed meeting. Core prices, excluding volatile food and energy items, are anticipated to rise 3.2% this quarter from a year ago, down from the previous estimate of 3.7%. Similarly, the projection for core inflation at the end of next year was adjusted to 2.4%, down from 2.6% in September. The Federal Reserve has maintained its benchmark federal-funds rate at a steady level of 5.25% to 5.5% for three consecutive policy meetings, having most recently raised rates in July. While most officials have been reluctant to openly discuss rate-cut timing, market expectations as reflected in interest-rate futures suggest a likelihood of rate cuts starting in the spring, with a potential reduction of at least 1 percentage point by the end of 2024. The central bank is navigating the delicate balance between moving cautiously to prevent economic decline due to higher interest rates and the risk of easing prematurely, causing inflation to exceed the 2% goal. Recent improvements in the U.S. economic outlook, characterized by slowing inflation and wage growth, provide the Fed with room to lower rates rapidly if needed, even if economic expansion remains stable. The European Central Bank (ECB) also decided to hold its deposit rate at 4% for a second consecutive meeting but revised down its inflation forecasts for the coming year. This adjustment indicates an expectation that inflation will be brought under control soon, prompting an acceleration in the exit from pandemic stimulus programs. The ECB's dovish shift was evident in the removal of a phrase from previous statements suggesting that inflation would remain elevated for an extended period. Meanwhile, the Bank of England adopted a more cautious stance, stating that it is premature to consider lowering its key interest rate. Inflation remains elevated in the UK relative to the US and the Eurozone, with prices in the UK up 4.6% compared to a year ago.