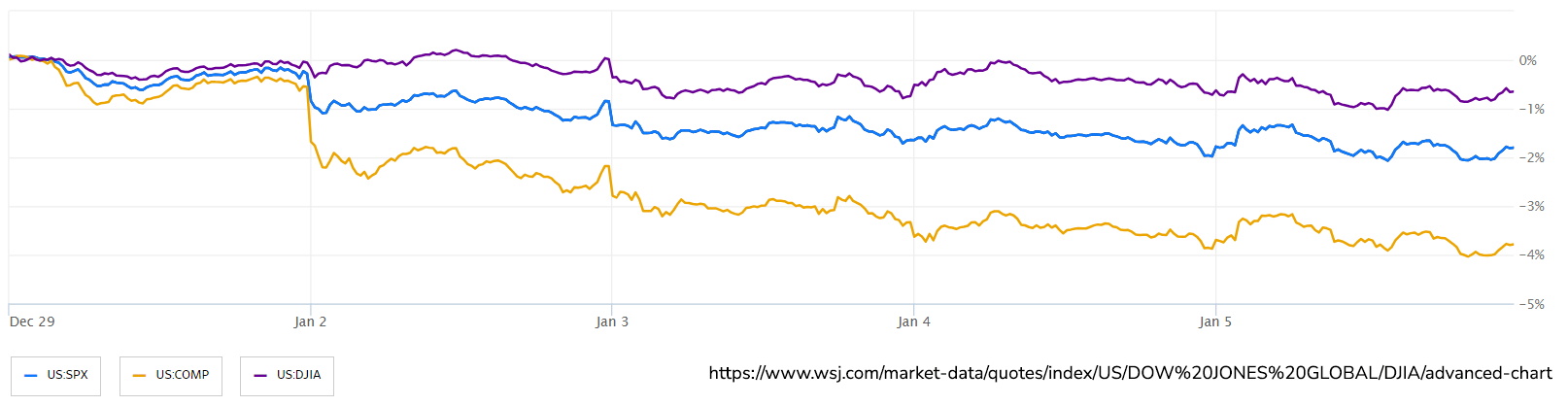

US Equities ended the first week of 2024 on a down note after nine straight weeks of gains for the S&P 500 and Nasdaq. Treasuries were weaker across the yield curve as the 10-year yield moved back above 4%, while the dollar index posted strong gains, and oil finished up 3.0% for the US benchmark West Texas Intermediate (WTI). Analysts and traders point towards a defensive positioning to start the year off as the markets look to be in overbought territory following the dovish tone from the Federal Reserve in December. Corporate earnings expectations for the fourth quarter and geopolitical concerns over a potential widening of the conflict in the Red Sea have added anxiety to the markets.

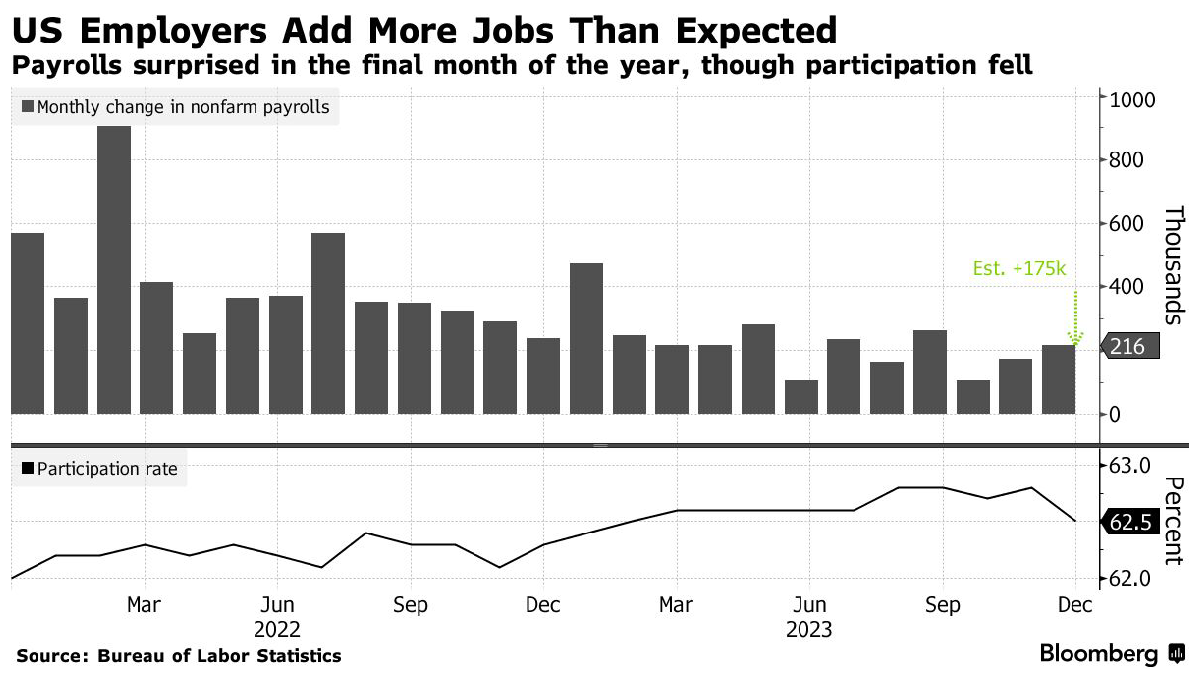

Last week, two reports showed that the labor market remains strong despite high interest rates, though some figures suggested softening. The United States experienced a decline in job openings in November, reaching the lowest level since early 2021, suggesting a cooling demand for labor. The Bureau of Labor Statistics Job Openings and Labor Turnover Survey (JOLTS) reported a decrease from 8.85 million to 8.79 million vacancies. Hiring also dropped to its lowest point since April 2020. Notably, layoffs saw a slight decrease. The quits rate, reflecting voluntary job departures as a percentage of total employment, reached its lowest point since September 2020. The ratio of job openings to unemployed individuals remained at 1.4, a significant decrease from its 2-to-1 peak in 2022. Meanwhile, the nonfarm payrolls survey for December showed a notable uptick in job growth with payrolls increasing by 216,000, surpassing the median estimate of 175,000. The unemployment rate remained stable at 3.7%, and average hourly earnings exceeded expectations by rising 0.4% from the previous month. Kathy Jones, Chief Fixed Income Strategist at Charles Schwab, characterized the overall job market as steadily cooling off, but emphasized that the increase in average hourly earnings might influence the Federal Reserve to maintain its current stance for a longer duration than the market anticipates. Despite these positive aspects, the labor-force participation rate experienced its largest monthly drop in nearly three years, particularly affecting younger and older cohorts. The duration of unemployment spells extended, and the number of full-time employees saw the most significant decline since April 2020. Furthermore, the report indicated a decline in temporary-help employment, often considered a precursor to recession, reaching its lowest point since May 2021.

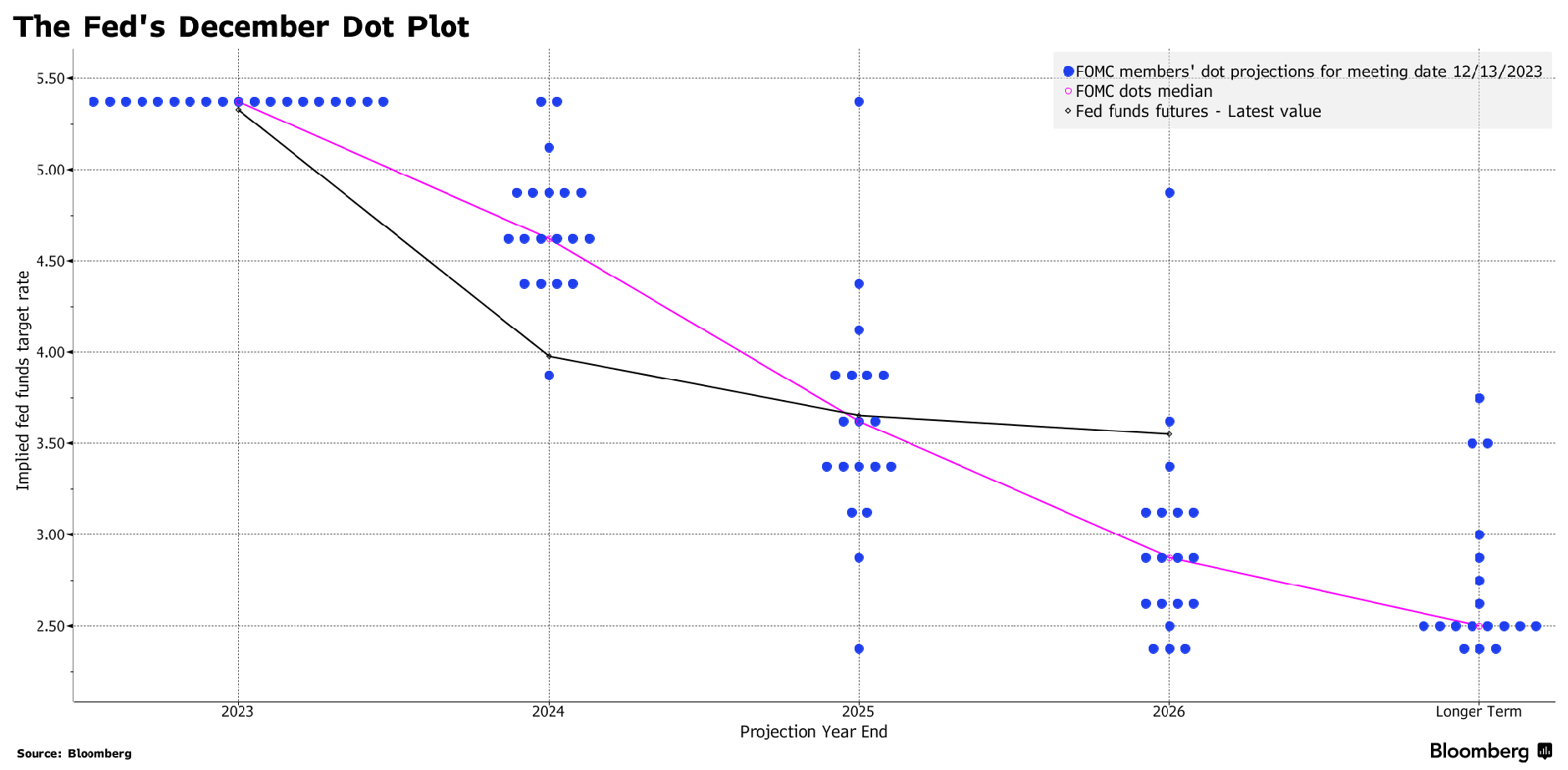

The Federal Reserve's December meeting minutes reveal a nuanced outlook on monetary policy, despite the decision to maintain interest rates. While there was no substantial debate on when to initiate rate cuts, most officials anticipated a lowering of policy rates before the end of the year. The minutes underscored heightened uncertainty following the most rapid interest rate increase in four decades. Some policymakers expressed concerns about leaving rates too high for an extended period, emphasizing the downside risks associated with an overly restrictive stance. They highlighted the potential for a rapid downturn in the labor market if rates were not adjusted appropriately. Conversely, others believed that current conditions might warrant keeping rates steady for longer, especially if inflation remained persistently above the Fed's 2% target. The confusion surrounding Fed Chair Jerome Powell's news conference and the subsequent market reactions indicated a shift in expectations towards rate cuts, despite the Fed's official stance on being attentive to economic risks that might require higher rates. The minutes reflected increasing comfort with the effectiveness of previous rate hikes, as references to "unacceptably high" inflation, seen in previous minutes, were absent in the latest account. However, the minutes did not provide clear insights into officials' views on the prospect of rate reductions. Some believed the easiest part of the inflation fight was over and further progress may be tougher, while others saw potential for supply-side improvements to continue. The challenge for the Fed lies in managing market expectations, with investors already anticipating earlier and deeper rate cuts than initially projected by the Fed. The focus on preventing real interest rates from becoming too tight may prompt the Fed to lower nominal rates even before reaching the 2% inflation target.