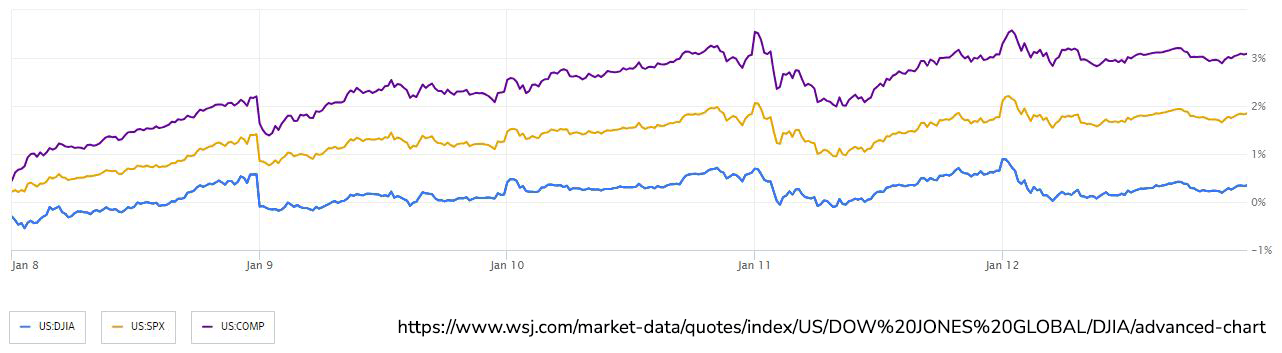

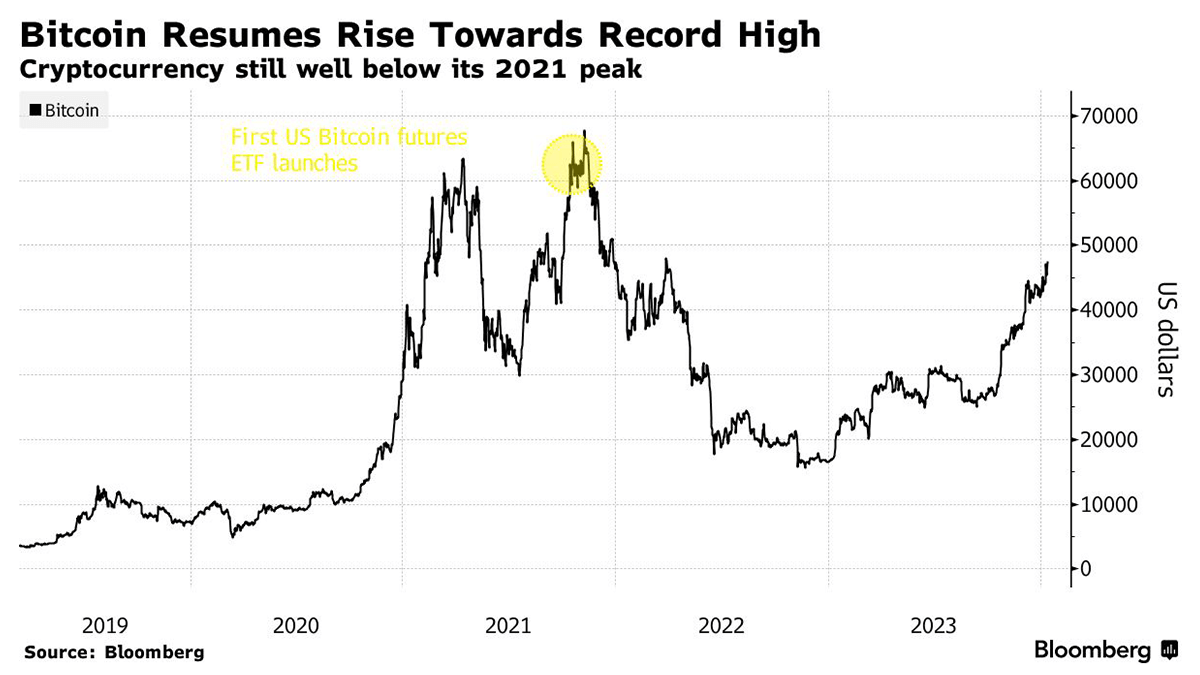

In the current financial landscape, a wave of bank earnings reports from JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo has captured investors' attention. The results so far indicate that Americans' finances have remained surprisingly stable. Specifically, JPMorgan Chase reported the most profitable year in US banking history, with record net interest income and an optimistic forecast. Bank of America's earnings fell short of expectations, marked by various charges in the fourth quarter. Wells Fargo predicted a 9% drop in net interest income for 2024, while Citigroup announced plans to eliminate 20,000 roles to boost returns. Bank stocks dipped in response to the earnings reports. Delta Air Lines and UnitedHealth reported results, contributing to declines in their respective stocks, while real estate and energy stocks saw gains. Stock indexes experienced slight declines on Friday, with the S&P 500, Nasdaq, and Dow Industrials down marginally, though the S&P 500 remains in striking distance of its record high. Despite a strong performance in the equities benchmark, analysts project only a modest growth in fourth-quarter profits for S&P 500 members. Meanwhile, the focus shifts to the climb in oil prices and energy shares, driven by US-led coalition strikes on Houthi rebel targets in Yemen. Oil prices rose, with benchmark US crude futures gaining 0.9%. In the cryptocurrency market, Bitcoin tumbled below $44,000, erasing gains made after the US Securities and Exchange Commission (SEC) approved bitcoin ETFs, providing a stock-like ease of access to the cryptocurrency. Internationally, the Stoxx Europe 600 gained ground, while Japan's Nikkei 225 continued its rally with a 1.5% increase. The 10-year Treasury yield dipped, settling at 3.949%. Treasury two-year yields recently hit their lowest level since May at 4.15%, driven by a surprising decline in producer prices on Friday. This development has intensified expectations of Federal Reserve rate cuts in the coming year. Traders are now pricing in an 80% chance of a Fed reduction in March, a significant increase from just over 50% a week ago.

The SEC has granted approval for the first U.S. exchange-traded funds (ETFs) that hold bitcoin directly, marking a significant development that will allow mainstream investors to trade bitcoin as easily as stocks and mutual funds. This decision has been eagerly anticipated, contributing to a surge in bitcoin prices, which reached nearly $48,000 during the week, a substantial increase from $17,000 in January 2023. Previously, individuals interested in trading digital currencies faced the choice of using crypto exchanges with high transaction fees or investing in products indirectly tracking bitcoin. Several bitcoin-futures ETFs already exist, utilizing futures contracts to provide exposure to bitcoin price movements, though criticism has been directed at these funds for deviating from bitcoin's actual price. The SEC, under the leadership of Chair Gary Gensler, had previously rejected applications for spot bitcoin ETFs, citing concerns about vulnerability to fraud and market manipulation. However, the recent approval signals a shift in regulatory stance. Interestingly, the SEC's decision coincided with a hack into its official account on X (formerly Twitter), which falsely claimed approval for the bitcoin ETFs in advance of the official announcement. The price of bitcoin initially surged but later reversed when the SEC clarified that its account had been compromised. Major asset management firms such as BlackRock, Fidelity Investments, ARK Investment Management, Invesco, WisdomTree, Bitwise Asset Management, and Valkyrie have applied to list the newly approved spot-bitcoin ETFs, which distinguish themselves by directly buying and selling the digital currency. Trading for these highly anticipated ETFs commenced on Thursday. The approval of spot bitcoin ETFs represents a significant step in integrating digital assets into traditional financial markets, providing mainstream investors with a more accessible and regulated means to engage with bitcoin.

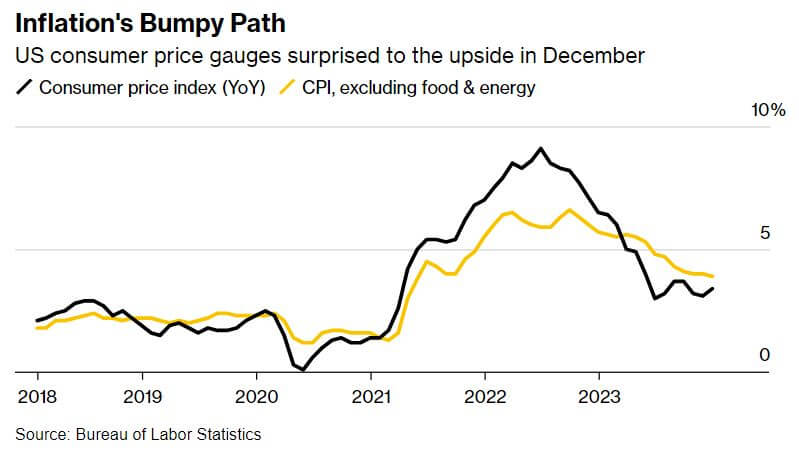

The year concluded with a noteworthy uptick in inflation, according to the latest report from the Labor Department. The Consumer Price Index (CPI) rose by 0.3% in December compared to the previous month and exhibited a 3.4% increase from the corresponding period in the preceding year. This contrasts with the 0.1% monthly gain observed in November, marking an acceleration from the 3.1% annual rise recorded that month. In terms of core prices, which exclude volatile food and energy items, there was a 0.3% increase in December, in line with November but exceeding the Federal Reserve's long-term inflation target of 2%. The year-on-year core prices showed a 3.9% uptick, indicating a modest deceleration from the 4% annual increase observed in November. In December, rising prices were driven by increased expenditures on rent, auto insurance, and dental visits, offset by declines in furniture, toys, and sporting goods. Energy costs rose by 0.4% on a monthly basis, fueled by hikes in gasoline and electricity prices. Federal Reserve officials are unlikely to adjust interest rates during their upcoming meeting. They rely on the personal-consumption-expenditures price index to gauge progress toward their 2% inflation goal. This index, which will be released later this month by the Commerce Department, currently stands just above 2.5%, a positive trend according to New York Fed President John Williams. Thankfully, though CPI surprised to the upside for December, the producer price index (PPI) fell 0.1% for the month. Core PPI rose only 1.8% in annual terms in December, the smallest rise since 2020. The consensus among Fed officials is that the last rate increase occurred in July, reaching a range between 5.25% and 5.5%, a 23-year high. Markets anticipate a potential rate reduction in March, contingent on future inflation readings. The overall decline in inflation since its peak in mid-2022 is attributed to normalized factory production, stabilized supply chains, consumer habit adjustments, and recent moderation in labor markets. However, robust consumer spending and potential price adjustments by businesses could impede the swift progress of disinflation witnessed in recent months.