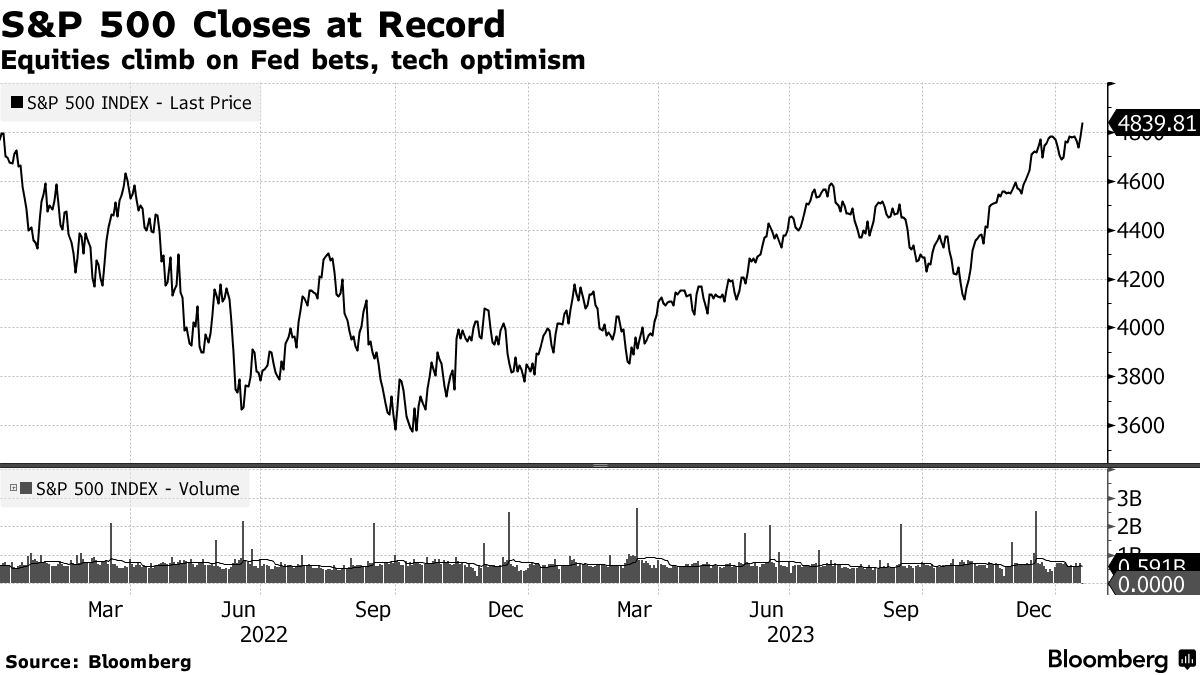

Wall Street closed the week on a positive note, reaching all-time highs fueled by speculation that the Federal Reserve will cut rates in the coming year. The S&P 500, led by the technology sector, hit a record high, surpassing 4,800. This surge is driven by optimism about the continued growth of artificial intelligence, with companies like Nvidia and Microsoft leading the way. The positive sentiment is supported by a drop in Treasury volatility, indicating a favorable environment for risk-taking on Wall Street. Additionally, a report highlighting high consumer confidence and lower inflation expectations is seen as "Fed-friendly." The S&P 500 erased losses from earlier in the week, rising by 1%, while the Nasdaq 100, driven by tech stocks, saw a larger increase. Notably, the "Magnificent Seven" cohort, Apple, Amazon, Tesla, Nvidia, Microsoft, Meta, and Alphabet, continues to lead the market. Semiconductor shares also received a boost from a bullish forecast by Taiwan Semiconductor Manufacturing Co. Investors are focusing on growth, technology, and the "AI bubble," with tech-stock funds experiencing significant inflows.

However, concerns arise as fund managers heavily invest in technology stocks, making the Nasdaq 100 vulnerable to potential pullbacks. Despite the ongoing rally in certain sectors, there are warnings of a widening divergence beneath the surface, indicating technical concerns. The market's narrow leadership, reminiscent of the previous year's mega-cap/AI dominance, raises the possibility of increased volatility in the near future. Economist Mohamed El-Erian cautions that markets may be overpricing the pace and amount of expected Fed rate cuts, as resilience in US economic data and concerns about persistent inflation may lead to a more gradual approach by the central bank. Currently, markets are pricing in approximately 1.4 percentage points of rate reductions for the year. While some officials, such as Fed Bank of Chicago President Austan Goolsbee, suggest the possibility of rate reductions in response to declining inflation, others, including Atlanta Fed's Raphael Bostic and San Francisco Fed Chief Mary Daly, emphasize the need for caution.

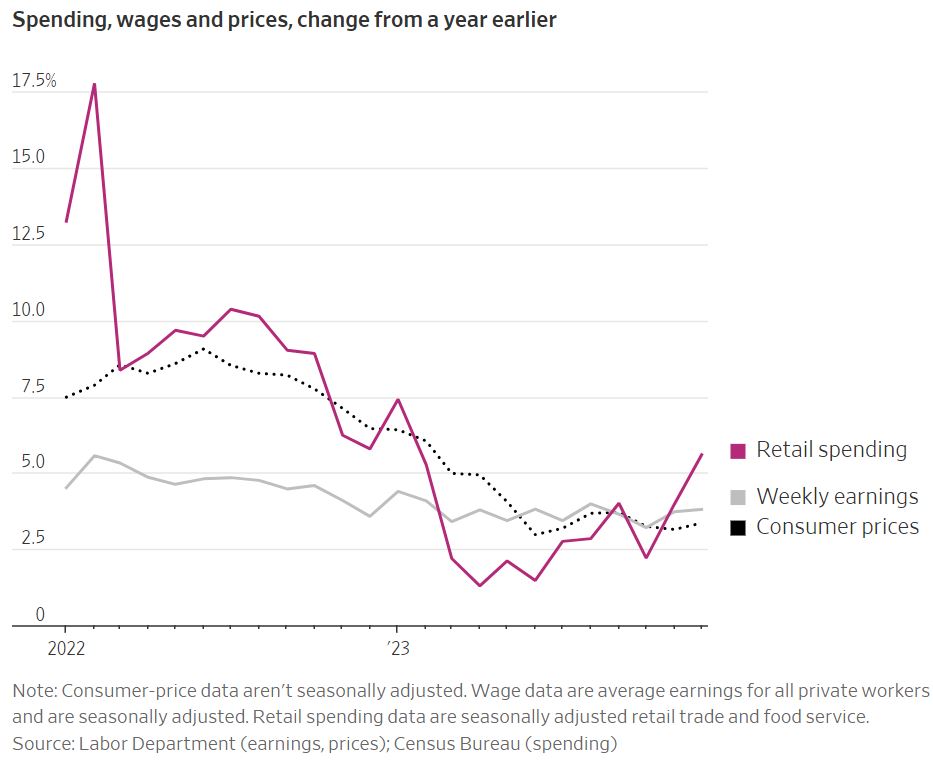

In December, U.S. retail sales exceeded expectations, rising by a seasonally adjusted 0.6% from the previous month, according to data released by the Commerce Department. This increase, following a 0.3% rise in November, suggests a robust finish to the holiday season for retailers. The positive trend was driven by higher spending at stores, auto dealerships, and online platforms. Notably, Americans spent more on vehicles, clothing, department stores, and online purchases. The strong retail performance is attributed to rising wages and moderating inflation, which have bolstered consumers' purchasing power. The 5.6% year-over-year increase in sales also indicates a solid growth trajectory, outpacing the 3.4% rise in the consumer-price index for the year through December. This moderation in spending growth aligns with the broader economic goal of achieving a soft landing, where inflation is controlled without triggering a recession. Consumer spending, a key driver of the U.S. economy, played a significant role in buoying economic growth in 2023. Despite the Federal Reserve's interest rate hikes, consumers continued to spend, particularly on travel and dining. The Fed, anticipating at least three rate cuts in 2024, is closely monitoring inflation and other economic indicators. Online spending reached a record $222.1 billion between November and December, reflecting a 4.9% increase from the previous year. This surge was attributed to discounts and the popularity of "buy now pay later" options. The overall economic growth for 2023 is estimated at 2.6%, defying earlier expectations of a recession. However, forecasts indicate a slowdown to a 1% growth rate in 2024 due to moderating labor market conditions and the impact of higher interest rates. Consumer sentiment in December was positive, fueled by robust hiring, strong wage growth, and optimism about the economic situation.

China faces significant economic challenges as it enters the new year. Gross domestic product (GDP) grew by 5.2% in the previous year, meeting expectations, but home prices and property-related spending indicators have disappointed, impacting business investment, job creation, and consumer spending. In December, home prices experienced the most significant decline since 2015, and spending on construction and decoration fell by 7.8% for the entire year. Housing new starts, a key confidence gauge among developers, plunged by 20.9%. The economy is still experiencing deflation, marked by the longest stretch of quarterly declines in broad price changes since the Asian Financial Crisis in 1999. Policymakers emphasize a focus on growth, with some potential for fiscal support in 2024. However, there is a debate among economists and investors about the nature and size of such support. The People's Bank of China has utilized lending programs to boost property investment, but bolder monetary policy steps, such as interest rate cuts, remain unimplemented. Addressing the deflation problem requires boosting consumption, but the size and speed of policy stimulus are crucial. The longer deflation persists, the greater the need for substantial policy measures.

Efforts by Beijing to reassure investors have been met with skepticism so far, and even attractive valuations have failed to provide support, with the MSCI China Index at its cheapest compared to the S&P 500 gauge from a forward earnings estimate perspective. The Hang Seng China Enterprises Index has already lost 11% in 2024, exacerbating a four-year losing streak and signaling a structural shift as both active and passive fund managers turn away from the second-largest stock market globally. Asian fund managers have reduced their allocation to China, with a net 20% underweight, the lowest in over a year, according to a Bank of America survey. The Hang Seng China Enterprises Index experienced a more than 6% plunge in a single week, on track for its worst January performance in eight years. On the mainland, the CSI 300 Index has dropped in nine of the last 10 weeks. The market has seen a staggering $6.3 trillion decline in the market value of Chinese and Hong Kong stocks since the peak reached in 2021, highlighting the difficulty for Beijing in restoring investor confidence.