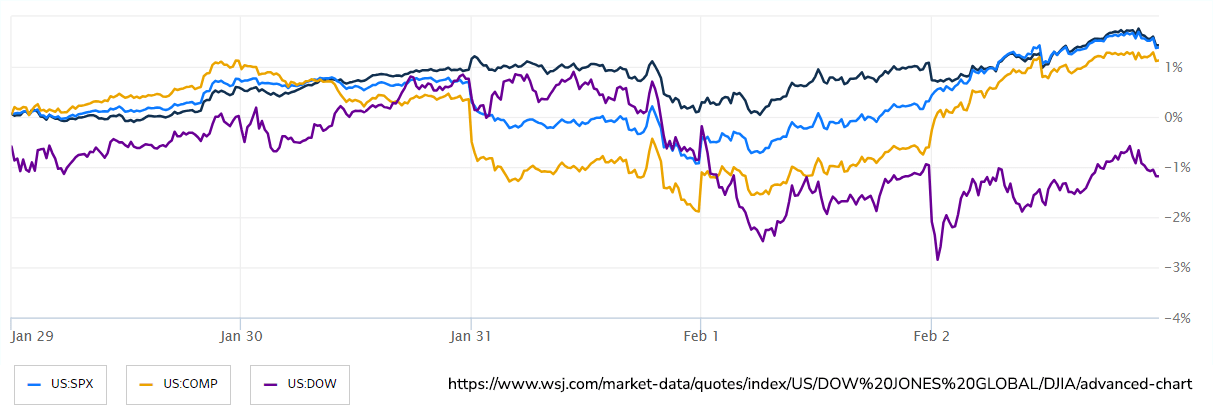

Equity markets finished the week on a positive note as the Nasdaq, S&P 500, and Dow Jones Industrial Average finished the day up 1.74%, 1.07%, and 0.35%, respectively. Big Tech earnings provided a tail wind to equities as META and AMZN rallied while AAPL pulled back. The nonfarm payrolls came in stronger than expected with a gain of 353,000 vs. the expected 185,000, while Average Hourly Earnings year-over-year climbed to 4.5% vs the expected 4.1%. The hot payrolls report drove a surge in Treasury yields on Friday and helped push down rate cut expectations to 115 basis points (bp) from roughly 140 bp on Thursday. Economists have pointed to Fed Chair Powell’s comment that the “Fed doesn’t need to see labor market weakness before cutting” as a sign that the central bank will continue to view disinflation as its primary goal.

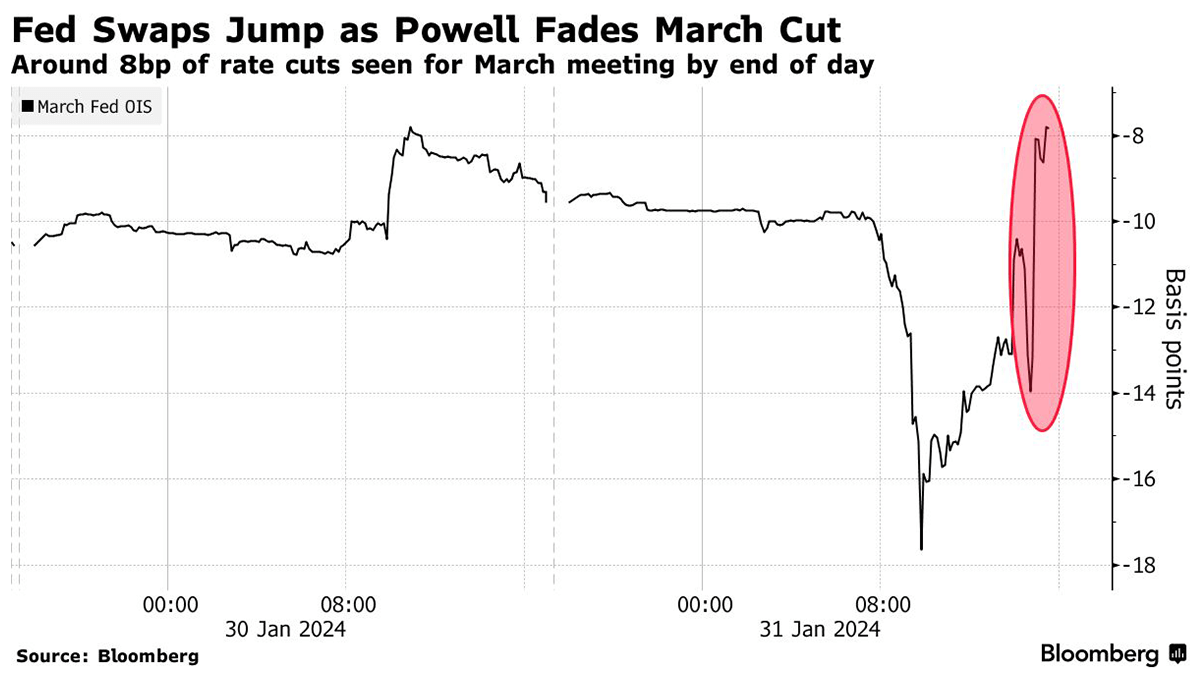

The Federal Reserve adjusted its interest-rate outlook in its latest policy statement, signaling a willingness to potentially lower rates in the coming months if convinced that inflation risks have diminished. As widely expected, the central bank maintained its benchmark federal-funds rate within a range of 5.25% to 5.5%, a level unchanged since July. The policy statement emphasized a shift in the balance of risks to achieving employment and inflation goals, adopting a more neutral stance and removing previous references to the possibility of "additional policy firming" or higher rates. While leaving the door open for rate cuts, the Fed clarified that it does not anticipate an immediate reduction in the target range, emphasizing the need for greater confidence in sustained inflation movement toward the 2% target. Federal Reserve Chair Jerome Powell acknowledged the likelihood of dialing back policy restraint later in the year but expressed caution due to the unpredictable nature of the economy's progress towards the inflation objective. Economic growth has outperformed expectations in recent months, potentially making policymakers cautious about declaring victory over inflation too early. However, cooling price pressures and wage growth indicate that inflation may continue to decline. The central bank faces the challenge of balancing the risks associated with moving too slowly, potentially causing economic downturn under higher interest rates, versus easing too quickly and allowing inflation to reaccelerate. The Fed is contemplating scenarios where rate cuts might be considered despite solid growth, particularly as inflation declines. The inflation backdrop has changed since December, with a decline in the 12-month rate of inflation, excluding volatile food and energy prices, to 2.9% in December, down from 3.5% in October. The market is showing a 50% probability at the next meeting in March and a 95% probability of a cut by May.

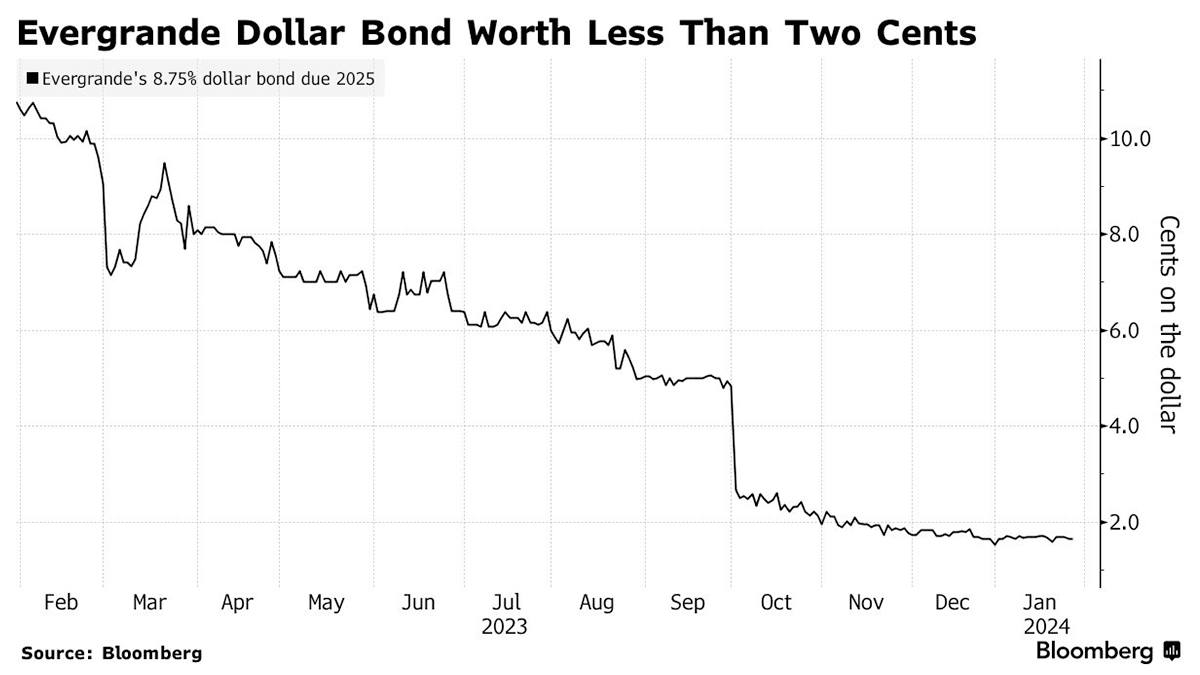

China Evergrande Group, once the country's largest property developer, has been ordered to liquidate by a Hong Kong court, marking the conclusion of a protracted saga that has significantly impacted the world's second-largest economy. Currently valued at just $275 million, a fraction of its peak, Evergrande's collapse is the most substantial in a crisis that has led to a record number of 50 defaults by property developers. The company, burdened with around $300 billion in liabilities, ceased debt payments more than two years ago, leading to ongoing negotiations with creditors. Despite last-minute efforts by creditors to negotiate a deal, the court issued the liquidation order, emphasizing that Evergrande had failed to present a viable restructuring plan or engage in good-faith negotiations. The court's decision grants creditors control over Evergrande's parent company, allowing them to liquidate all of its global subsidiaries and assets to repay debts. The liquidation process, expected to be complex due to the sheer scale and global nature of Evergrande's operations, will be closely watched by global investors. The legal reach of Hong Kong courts in China, where most of Evergrande's assets are located, remains a crucial factor. Additionally, navigating asset sales in an industry lacking liquidity and confidence poses a challenge for any new management. Over 90% of the company's assets are located in mainland China, raising questions about claims available for holders of $17 billion in Evergrande dollar bonds covered in its proposed restructuring plan.

Concerns about an uneven playing field for foreign capital amid President Xi Jinping's tightening control on the economy have led to the withdrawal of billions of dollars from mainland China by global investors. The ongoing courtroom drama also highlights the struggles of other Chinese developers facing liquidation, such as Jiayuan International Group and Yango Justice International Ltd. Despite Beijing's efforts to implement measures to revive home sales and provide liquidity to debt-laden developers, the property market continues to slump, with a Bloomberg gauge of Chinese developers dropping 59% in the past year. The crisis has dealt a blow to China's economic growth, as the real estate industry, once a major driver, now contributes to a drag on the economy. Economic indicators for 2023 reveal a dire situation, with a 6% decline in newly built home sales and falling prices, suggesting that the real estate slump is poised to persist for years, posing challenges to the country's economic recovery. Policymakers face the challenge of restoring investor confidence while ensuring the completion of unfinished homes and maintaining the resilience of the financial system amidst the property industry's challenges.