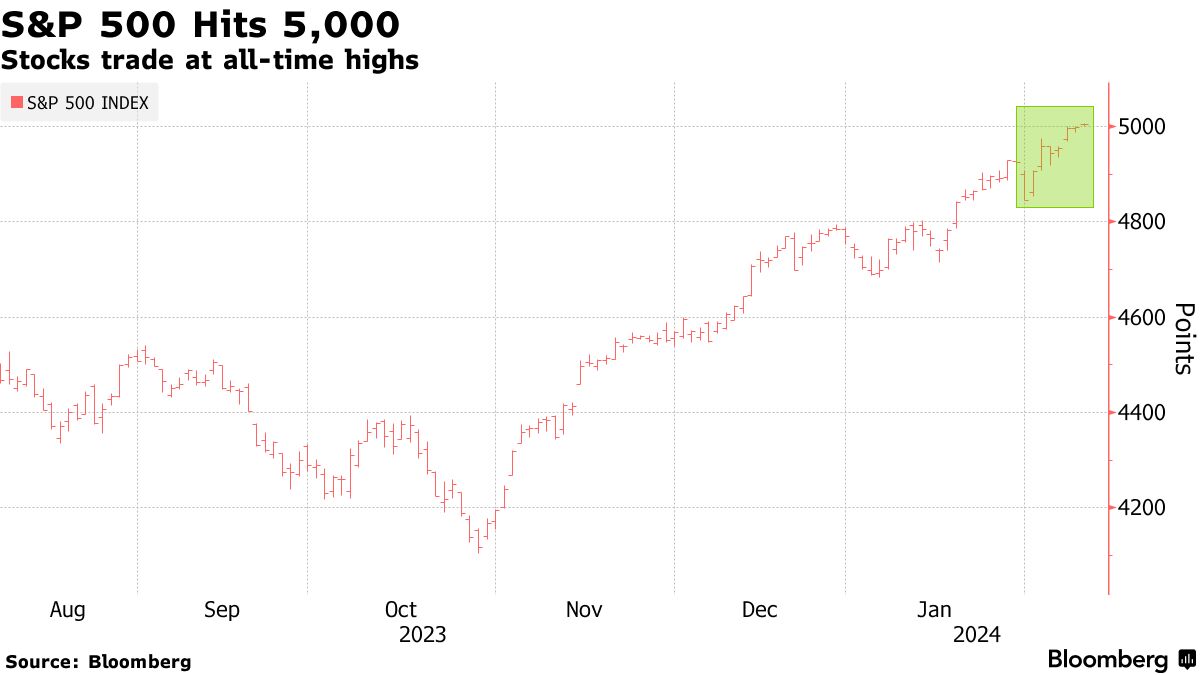

The S&P 500 last Friday surpassed the milestone of 5,000 for the first time. This achievement is attributed to a renewed rally in big tech stocks and expectations of rate cuts by the Federal Reserve, which is seen as supportive of corporate profits. Despite concerns about an overstretched market, investors remain optimistic about the economic outlook. The market was reassured on Friday by the lack of any surprises in the annual CPI revision, which further confirmed that inflation continued to cool to end 2023. Analysts emphasized the significance of the S&P 500's milestone, noting its implications for market sentiment and potential psychological support or resistance levels. While some experts view the achievement positively, others caution against market complacency and warn of potential sell signals triggered by high valuations and investor positioning. Despite differing opinions on the sustainability of the market rally and concerns about overheated stocks, many analysts remain cautiously optimistic, citing strong corporate earnings and ongoing economic growth as supporting factors. With the Q4 earnings season 2/3rds complete, 80% of companies have beaten earnings expectations, well above the 10 year average of 74%. Analysts are revising estimates upwards in response and are now projecting that Q4 earnings will rise 6.5% compared to a year ago. This would make this quarter the best for earnings growth since Q2 of 2022. However, there is acknowledgment of the need to monitor market developments closely, especially in light of changing Fed expectations and potential shifts in investor sentiment.

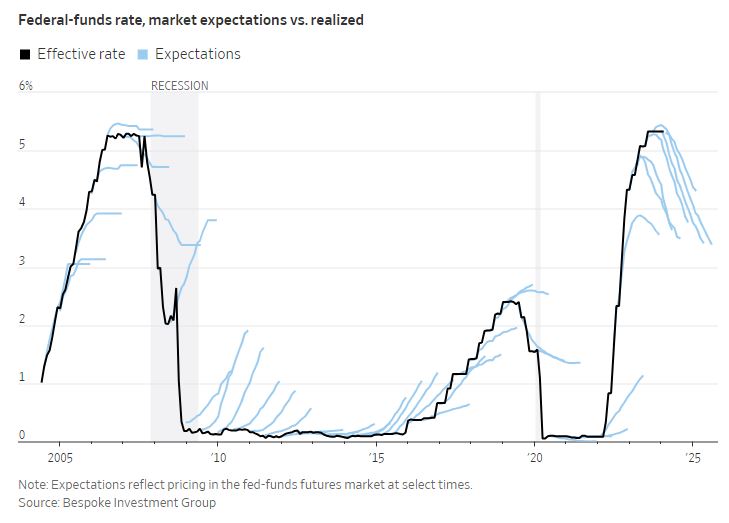

In the current financial landscape, investors are increasingly convinced that interest rates will decrease later in the year. This sentiment contrasts with the historical accuracy of such predictions, as Wall Street has often misjudged interest rate movements. Despite initial skepticism about the Federal Reserve reaching a 5% rate, traders are now inclined towards betting on imminent rate cuts, only to find their expectations challenged by strong economic data. The divergence between investors' expectations and actual rate projections holds significant ramifications, particularly for borrowing costs and stock prices. A decrease in interest rates typically elevates stock prices by stimulating growth and diminishing competition from bonds for investor capital. Investors monitor various indicators to gauge market sentiment and historical precedents. Currently, futures markets indicate a substantial divergence from Fed officials' rate projections, reflecting common tendencies for investors to anchor their expectations to recent events rather than long-term trends. Historical analysis reveals past instances where Wall Street misjudged the trajectory of interest rates, particularly in the aftermath of the 2008 financial crisis and more recent unexpected Fed decisions. Despite expectations for rate cuts, robust economic performance, such as the recent surge in job creation, challenges the necessity for such measures. The possibility of continued high rates poses risks to stock market stability, which may potentially disrupt the recent bond rally and lead to simultaneous declines in both fixed income and equity markets. The interconnectedness of stocks and bonds underscores the importance of closely monitoring inflation trends and government spending, which could exacerbate inflation concerns and bond market volatility.

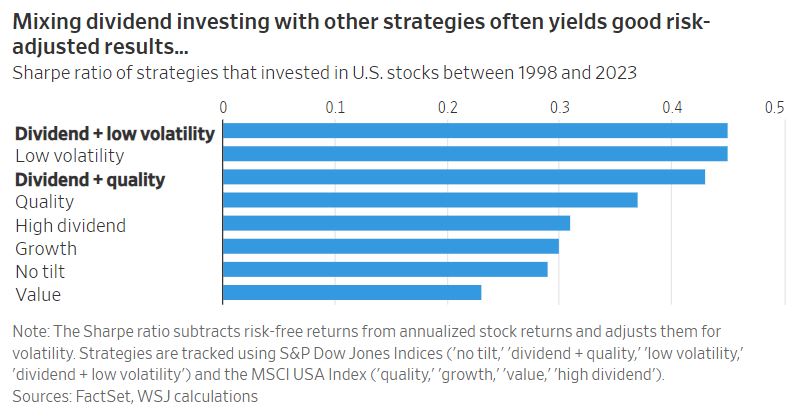

In the current investment landscape dominated by trends such as artificial intelligence (AI), sustainable funds, and quantitative (quant) investing, traditional stock picking strategies like dividends may seem antiquated. Sectors traditionally associated with dividends, like manufacturing and utilities, have lagged behind growth sectors like tech and healthcare in the 21st century, exacerbated by recent economic trends. However, recent developments suggest a potential revival of interest in dividends. Since the 2008-09 financial crisis, dividends have been overlooked by investors, with U.S. equities yielding above 5% delivering lower returns compared to the broader market. Daniel Peris, a portfolio manager and market historian, contends in his book "The Ownership Dividend" that low interest rates and the emergence of high-growth digital companies temporarily subdued the significance of dividends. Historical stock data corroborates this, showing that dividends contributed significantly less to total returns in the past decade compared to earlier periods. From the 1870s to 1950s, dividends made up 80% of total return for stocks, with capital appreciation constituting only 20%. However, over the past decade, dividends made up only 30% of total return. The average dividend yield of the S&P Composite has been below 2% for the past 25 years, much lower than its longer historical average of 4.3%. Peris argues that as the tech sector matures and scrutiny of buybacks intensifies, shareholders will increasingly demand income in the form of regular dividends, which may drive a version to the mean for the returns to dividends. Dividend payments still serve as a signal of fiscal prudence for some companies, contrasting with others that reinvest cash flows to underscore growth prospects. However, investors should approach dividend investing cautiously, avoiding stocks with unsustainable payouts and instead focusing on companies capable of sustainable dividend growth or those with low volatility. Despite recent underperformance, low volatility dividend strategies have historically offered risk-adjusted returns competitive with other strategies. Dividend strategies should be viewed as a middle ground between high-risk growth stocks and low-risk bonds, offering stable returns with lower volatility.