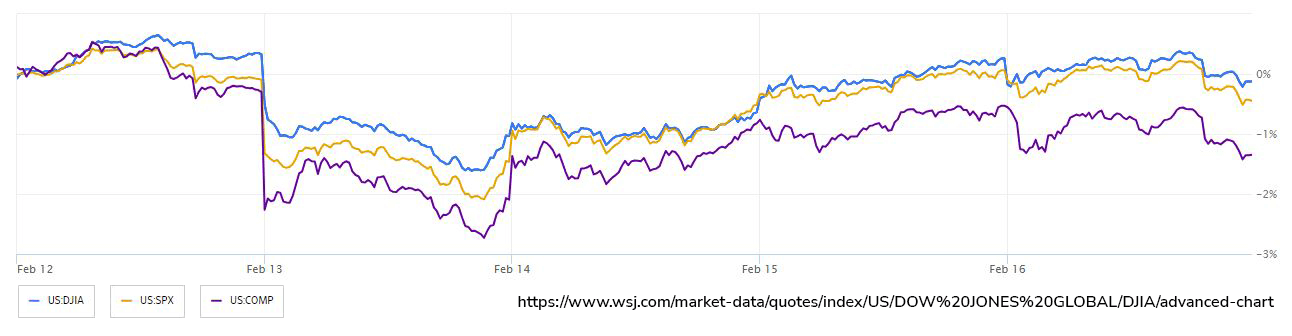

The global financial markets experienced notable movements last week driven by various economic indicators and Federal Reserve (Fed) signals. The US bond market, which is the largest in the world, continued its selloff trend amid speculation that the Fed would refrain from promptly cutting interest rates. This sentiment extended to the stock market, which saw a decline from its record highs. A significant factor contributing to market sentiment was the producer price index (PPI) report indicating persistent inflation pressures, particularly in service costs, suggesting inflation might be more resilient than previously anticipated. This, coupled with other economic data, led traders to revise their expectations of aggressive rate cuts, aligning more closely with the Fed's own projections. Key market indicators reflected this sentiment shift. Treasury yields rose, with two-year yields increasing notably. The S&P 500 halted its five-week winning streak, and the Nasdaq 100 experienced losses, particularly in prominent tech stocks like Meta Platforms Inc. and Apple Inc. The remarks from experts underscored the cautious approach investors were adopting. Some analysts viewed the latest inflation data as signaling minimal incentive for the Fed to enact rate cuts in the near term. However, there was also acknowledgment that achieving the Fed's inflation target would pose challenges, necessitating a reassessment of monetary policy. Notably, there were divergent views on the future direction of interest rates, with former Treasury Secretary Lawrence Summers suggesting a small potential for rate hikes given persistent inflationary pressures. Meanwhile, separate data indicated improved consumer sentiment and ongoing challenges in the housing market. Despite these developments, US equities experienced only a modest decline, with investors focusing on strong earnings and optimism surrounding artificial intelligence. However, concerns were raised about the valuations of certain tech stocks, with suggestions of a possible correction in the sector.

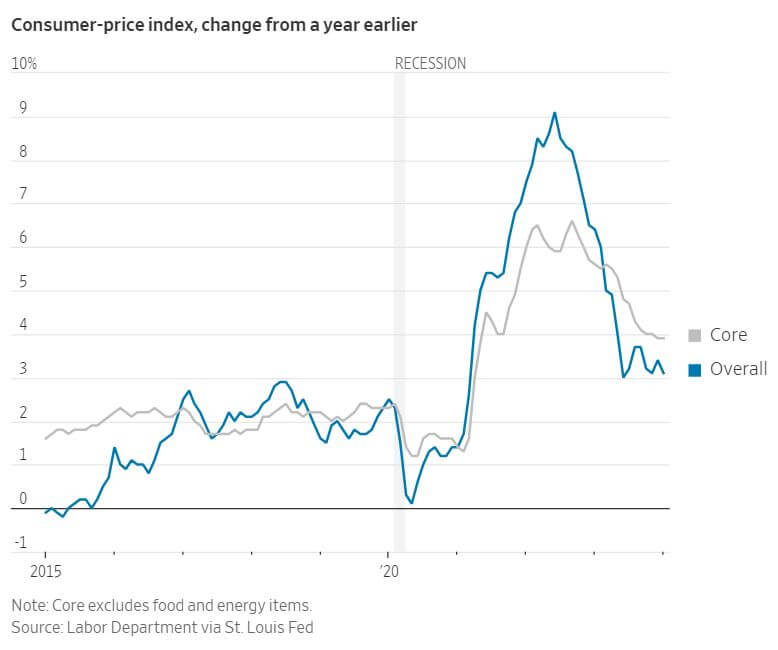

The latest release of US consumer price data for January 2024 showed price increases remained stubbornly high, potentially postponing anticipated interest-rate cuts by the Federal Reserve. Both monthly and yearly increases of the consumer price index (CPI) exceeded expectations, including core measures excluding food and energy costs. CPI rose at an annual rate of 3.1%, cooler than December’s 3.4% increase, but above the consensus forecast for an increase of 2.9%. Particularly notable was the substantial increase in a vital subset of service prices, marking the most significant surge in nearly two years, alongside escalating shelter costs. This was followed up by producer price index (PPI) data on Friday that also surprised to the upside. This unexpected inflationary pressure diminishes the likelihood of imminent rate cuts by the Fed, prompting traders to revise down expectations of such actions. The door has likely been closed for a rate cut in March, and swaps pricing indicates that the odds of a rate cut in May dropped from 64% to roughly 25% by the end of the week. Despite this surprise to the upside on CPI, economists maintain that the economy remains in a broader downward trend in inflation. The observed rise in prices, largely attributed to housing costs, prompts a cautious approach from the Fed, favoring a wait-and-see strategy until broader price pressures ease. The Bureau of Labor Statistics' recent annual revisions confirmed a steady decline in inflation towards the end of 2023. Shelter prices, a crucial component, are expected to play a pivotal role in driving core inflation down to the Fed's target. However, the discrepancy between the CPI and the Fed's preferred measure, the PCE index, persists, mainly due to varying weightings on shelter. Fed policymakers, buoyed by a robust job market and sustained real earnings growth outpacing inflation, are inclined to maintain a cautious stance on rate adjustments, with expectations of continued monitoring through multiple inflation reports leading up to their next policy meeting in March.

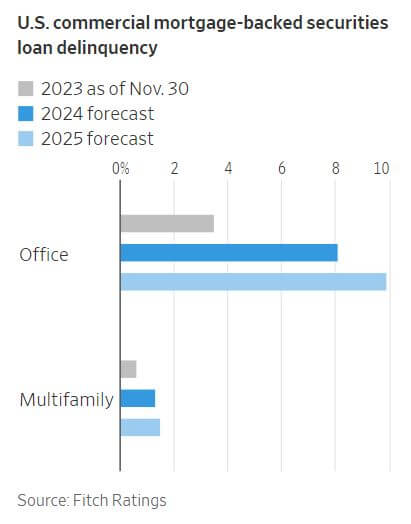

The commercial real estate market is facing a significant challenge with a record amount of loans coming due for refinancing. In 2023, $541 billion in debt backed by various types of commercial properties matured, marking the highest ever for a single year. This trend is expected to continue, with over $2.2 trillion in debt maturing by the end of 2027. While many loans were repaid or extended in 2022 and 2023, the extensions are now expiring, pushing borrowers to confront higher interest rates, vacancies, and weakening cash flows, which are lowering property values. The impact is widespread across various types of commercial properties, with office buildings particularly affected by remote and hybrid work trends, while multifamily and industrial sectors also show signs of weakness. Recent transactions of office buildings at significantly reduced prices compared to pre-pandemic levels signal potential equity losses for owners, with banks already experiencing substantial hits to their loan portfolios as loan defaults rise. Amidst these challenges, the intensifying property crisis in China adds further uncertainty, potentially leading to asset liquidation and further downward pressure on global property values. While concerns about the financial fallout from remote work persist, it's crucial to contextualize these challenges. Despite the severity of the situation, commercial real estate constitutes only a fraction of the overall property market, with offices representing a relatively small portion. Even in the worst-case scenario where all offices lost the entirety of their value in the US, losses from commercial property would only total roughly one-fourth of the broader residential real estate market's downturn experienced during the 2007-2009 financial crisis. Regulatory scrutiny is also increasing, with regulators closely monitoring commercial-property debt exposure, particularly among smaller banks. Measures such as aggressive write-downs and additional reserve requirements aim to mitigate potential losses and ensure financial stability amidst the evolving property landscape. While the impact of commercial real estate challenges is significant, it is unlikely to inflict severe, long-term damage on the financial system.