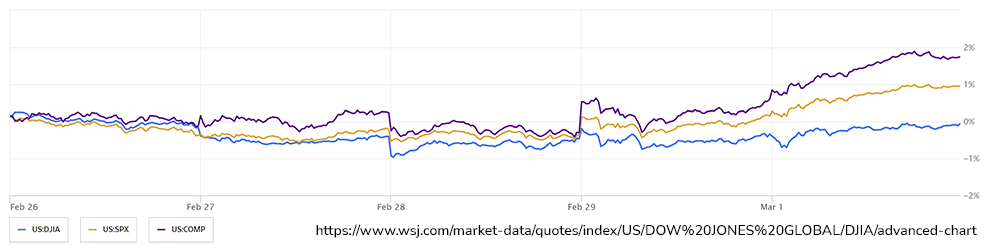

Equity markets finished February on a high note as the S&P 500, Nasdaq, and Dow Jones Industrial Average all posted positive returns for the second consecutive month. Nvidia continues to dominate markets in the AI mania as the market cap for the company exceeded $2 trillion for the first time on Friday. Equity markets have rallied despite hawkish repricing of the Fed’s expected rate-cutting cycle and the market has priced out approximately half of the easing that was expected earlier in the year. Expectations for how many cuts and how much now fall more in line with the central bank's guidance as recent Fed speakers have stressed the need to remain patient as there may be bumps along the way.

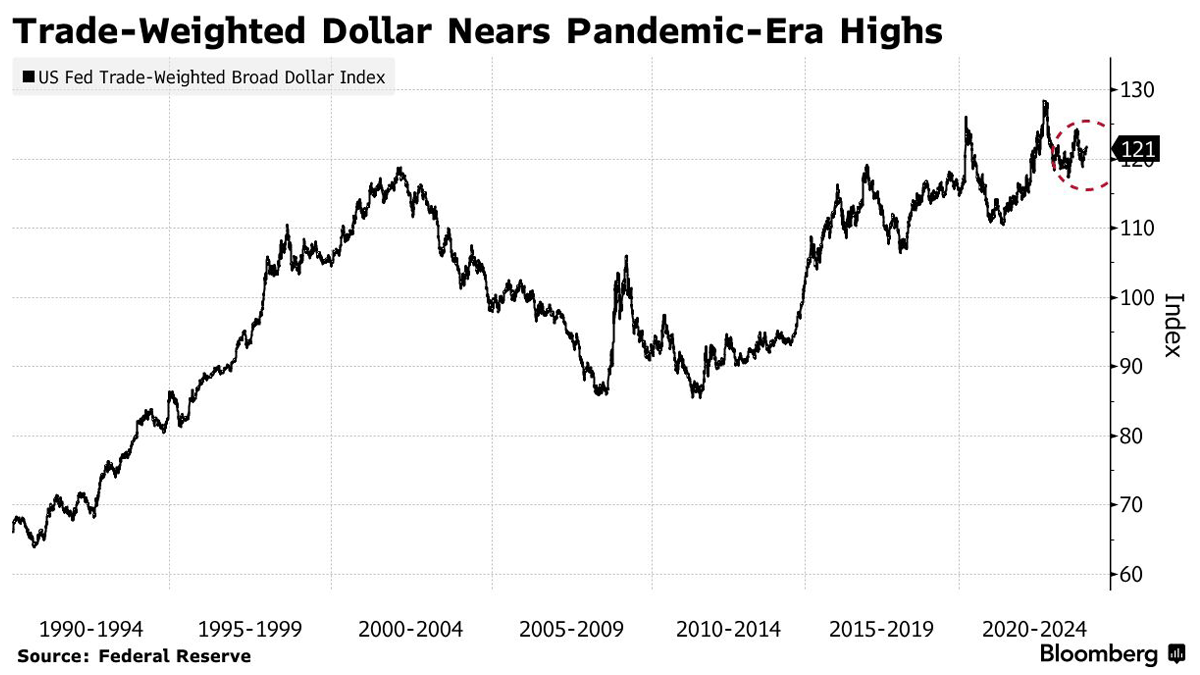

The recent surge in US risk assets has underscored a significant underlying theme: the unparalleled appeal of the US dollar, which has emerged as the preeminent choice for investors among currencies. The dollar's current trajectory places it near pandemic-era highs and on track for its strongest performance since 2020. Notably, against major trading partners' currencies, it stands 17% above its average over the last two decades, indicating its robustness. Several factors contribute to the dollar's resilience. Firstly, indicators signaling sustained US economic strength have buoyed its value, prompting a swift reassessment among traders regarding the Federal Reserve's monetary policy outlook. Expectations for immediate monetary easing have dwindled, with the likelihood of prolonged periods of elevated benchmark rates favoring the dollar's strength. Moreover, the dollar's dominance is rooted in fundamental pillars such as US productivity growth, economic dynamism, substantial inflows into American assets, and advancements in critical sectors like artificial intelligence. These factors fortify the dollar's status as the world's primary reserve currency, mitigating the impact of potential Fed rate cuts and upholding the narrative of "American exceptionalism." Recent market dynamics reflect a significant shift, with major players abandoning bearish dollar positions, contributing to its upward trajectory. Economic forecasts have also been revised upward, further supporting the dollar's outlook. The surge in US equity markets, particularly notable in tech stocks like Nvidia, has attracted substantial capital inflows, reinforcing the dollar's position. While some indicators suggest the dollar's momentum may be waning in the options market, its dominance presents both opportunities and challenges. For the US, a stronger dollar can weigh on corporate profits by suppressing overseas sales, while for other nations, it can elevate import costs and inflationary pressures, potentially necessitating tighter monetary policies. Geopolitical factors, including potential policy shifts under a Donald Trump presidency, and concerns over fiscal profligacy, could influence the dollar's trajectory. However, despite these considerations, the global primacy of the US currency remains largely intact, underscoring its pivotal role in international markets.

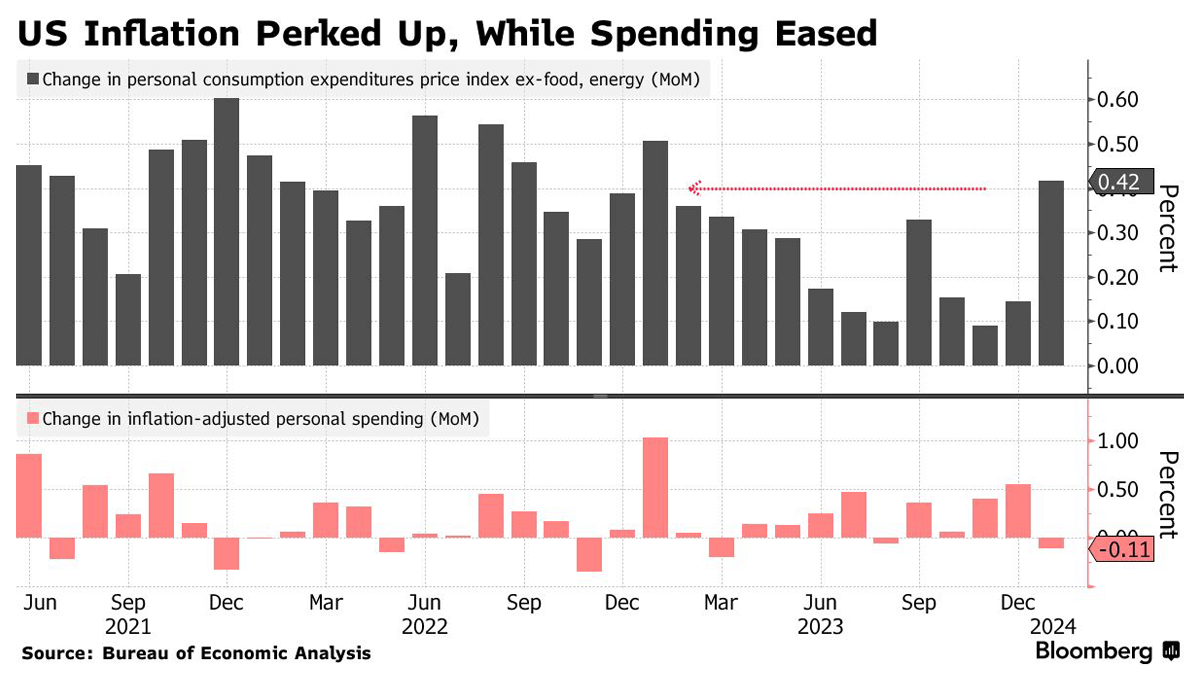

The Federal Reserve’s preferred measure of underlying inflation, the core personal consumption expenditures (PCE) price index, saw a notable uptick last month. Stripping away the volatile food and energy components, the index surged by 0.4% in January compared to the prior month, marking its most significant increase in nearly a year. Year-on-year, this index advanced by 2.8%, a figure economists regard as a more accurate reflection of underlying inflation trends than the CPI index. Real consumer spending experienced a decline for the first time in five months, following a robust holiday shopping season. Despite this, real disposable income remained relatively stable, indicating a sustained but cautious approach to spending. Federal Reserve officials have consistently emphasized their hesitance to reduce interest rates until they are confident in a sustainable cooldown of inflation. The latest report reinforces their cautious stance, particularly with the core PCE data surpassing the Fed’s 2% target, registering at 2.5% on a six-month annualized basis in January. Of particular interest to policymakers is services inflation excluding housing and energy, which increased by 0.6% from the previous month, the most significant uptick since March 2022. Notably, costs for portfolio management and accommodation saw substantial increases. Despite the robust labor market, the economy faces challenges such as high borrowing costs and persistent inflation, which may be dampening consumer spending. The decline in goods outlays, notably in motor vehicles purchases, contributed to this restraint, while services spending continued its ascent, albeit with variations across sectors. Looking ahead, Fed Chair Jerome Powell and colleagues have signaled no immediate plans for a rate cut at their upcoming March meeting, with June being the more likely timeframe.