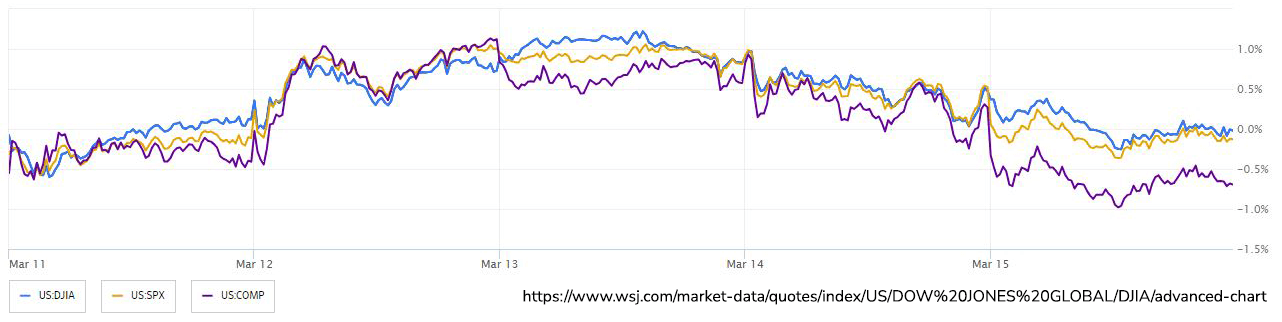

Amid a volatile week's end, stock markets experienced a downturn primarily driven by a sell-off in the technology sector, compounded by the expiration of a significant volume of options contracts on Friday. The quarterly event, known as triple witching, involved the maturity of derivatives linked to stocks, index options, and futures, amounting to approximately $5.3 trillion, as reported by Rocky Fishman of firm Asym 500. This convergence of events prompted heightened market volatility and made predicting market direction particularly challenging, as noted by Matt Maley of Miller Tabak. The market context was further complicated by the looming Federal Reserve policy meeting, with investors closely monitoring signals regarding potential interest rate adjustments amidst rising inflation concerns. The S&P 500 and Nasdaq 100 indices experienced declines, with notable tech companies such as Adobe Inc. facing setbacks due to weaker sales forecasts. However, Nvidia Corp. continued its upward trajectory ahead of its upcoming artificial intelligence conference. In the fixed income market, Treasury 10-year bonds had their worst week of the year, reflecting shifting investor sentiments and expectations regarding future Fed actions. The 10-Year US Treasury finished the week with a yield of 4.31%. Economic indicators pointed to unexpected slowing in the US economy, coupled with inflation deceleration, adding to market uncertainty. Analysts at JPMorgan Chase & Co. revised their projections for Fed rate cuts in 2024, anticipating a total reduction of 75 basis points, down from the previous estimate of 125 basis points. The timing and extent of rate cuts remained contingent on evolving economic data, with potential implications for market dynamics. Despite market optimism fueled by expectations of Fed easing, concerns persisted regarding the Fed's response to inflationary pressures. A more hawkish stance from the Fed could dampen market sentiment, particularly if it deviates from investors' expectations of three rate cuts starting in June.

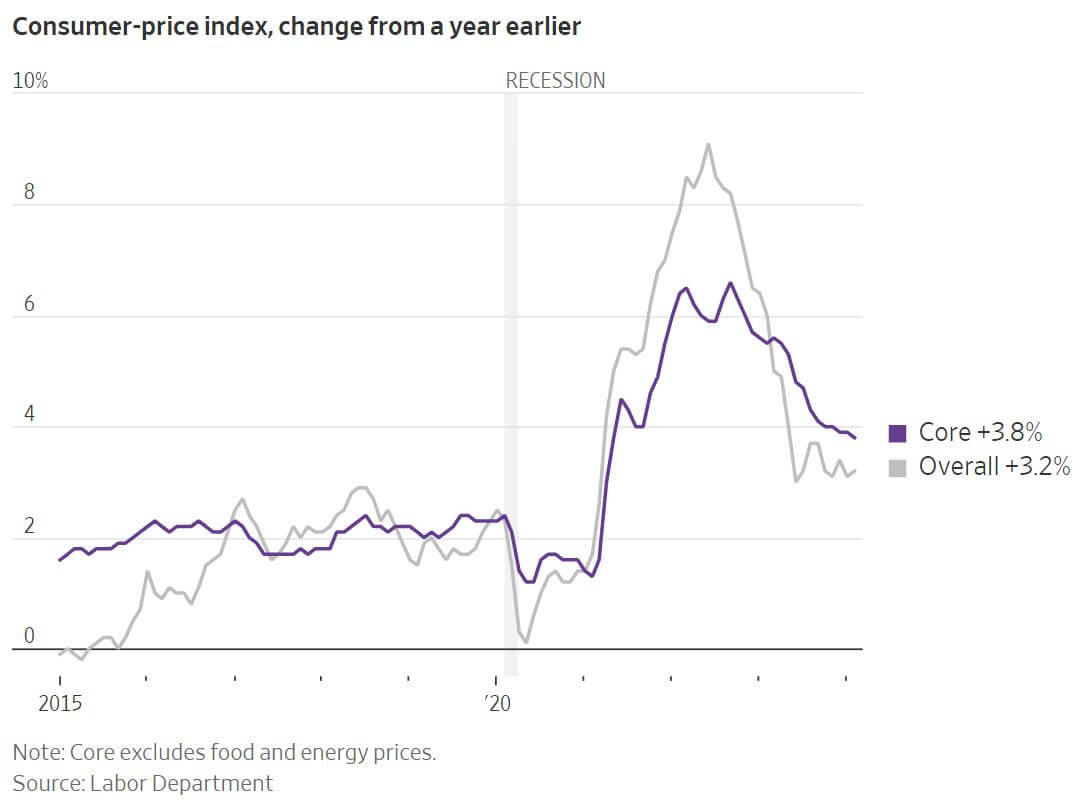

The latest U.S. inflation report revealed a slight uptick, with consumer prices rising 3.2% in February compared to the previous year, slightly exceeding economists' expectations of 3.1%. This second consecutive month of stronger-than-anticipated inflation is expected to reinforce the Federal Reserve's cautious stance on potential rate cuts later this year. Despite this, the focus remains on when to implement rate reductions rather than considering rate hikes, as inflation has eased from recent highs. Eric Rosengren, former head of the Boston Fed, noted that while the inflation report indicates a gradual improvement in core inflation, the expectation of three rate cuts this year remains unchanged. The stock market reacted positively to the report, indicating investors' confidence in a potential rate cut in June. However, the report poses challenges for the Fed's upcoming deliberations. Core prices, excluding food and energy, rose more than expected, raising concerns about inflation not reaching the 2% target. There's uncertainty regarding whether most Fed officials will still anticipate three rate cuts this year or if there will be a shift towards only two cuts. The Fed's inflation target of 2% is measured against the Personal Consumption Expenditures Price Index (PCE), which tends to be cooler than the Consumer Price Index (CPI) reported by the Labor Department. While the CPI report doesn't directly influence the Fed's target, it provides insights into inflation trends. Additionally, the divergence in CPI and PCE indices complicates forecasting, with economists projecting lower core PCE prices for February compared to January. Fed officials are closely monitoring labor-intensive services prices to gauge wage pressures. The February jobs report showed a cooling in average hourly earnings growth, which could mitigate concerns about wage inflation. Fed Chair Jerome Powell has indicated that while inflation readings need not improve significantly for rate cuts to occur, the degree to which core prices rise this year will be critical.

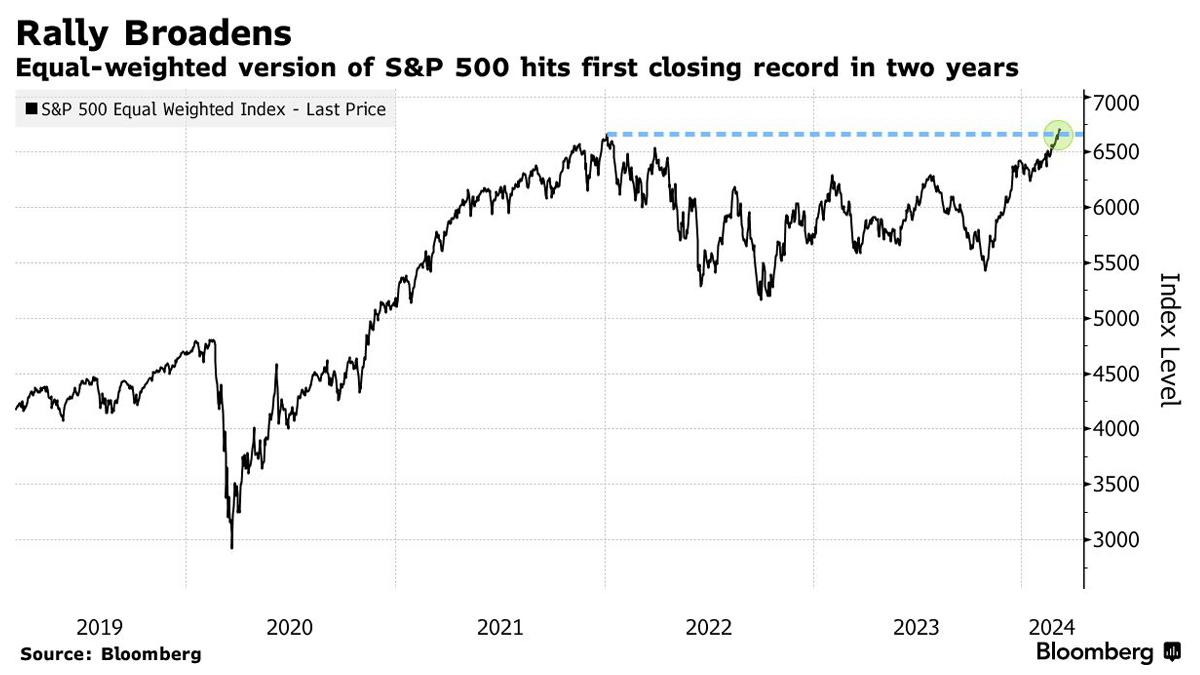

The recent surge in US stocks has prompted concerns reminiscent of past boom-and-bust cycles, raising questions about the potential overheating of the market. Notably, the S&P 500 Index has hit record highs frequently in 2024, with the AI company Nvidia Corp. witnessing a staggering 80% increase in stock value, adding approximately $1 trillion to its market capitalization. Additionally, speculative assets like Bitcoin have experienced significant surges. However, there are indications suggesting that the current strength in the market, driven largely by the economy's resilience and strong corporate earnings, may not necessarily indicate a speculative frenzy. Several of the leading stocks, known as the "Magnificent Seven," have shown signs of faltering, suggesting that investors are not indiscriminately pouring money into the market. Apple, Tesla, and Alphabet have experienced declines, suggesting a shift in investor sentiment. Furthermore, broader market indicators suggest a widening rally beyond just technology stocks. The S&P 500 Equal Weight Index, which treats each constituent equally, has reached a historic high, indicating broad-based market strength. Additionally, data shows an increasing number of S&P 500 stocks reaching all-time highs, though still leaving room for further market participation. The IPO market also presents a contrast to previous bubble periods, with fewer instances of significant first-day price pops for newly listed companies. This suggests a more cautious investor sentiment compared to previous euphoric periods. Valuation metrics, such as price-to-earnings ratios and price-to-sales multiples, indicate that while certain tech stocks remain relatively stretched, they are not at levels seen during past market peaks. Overall, these factors suggest that while concerns about market overheating exist, the current market environment may not necessarily indicate a bubble formation akin to previous cycles.