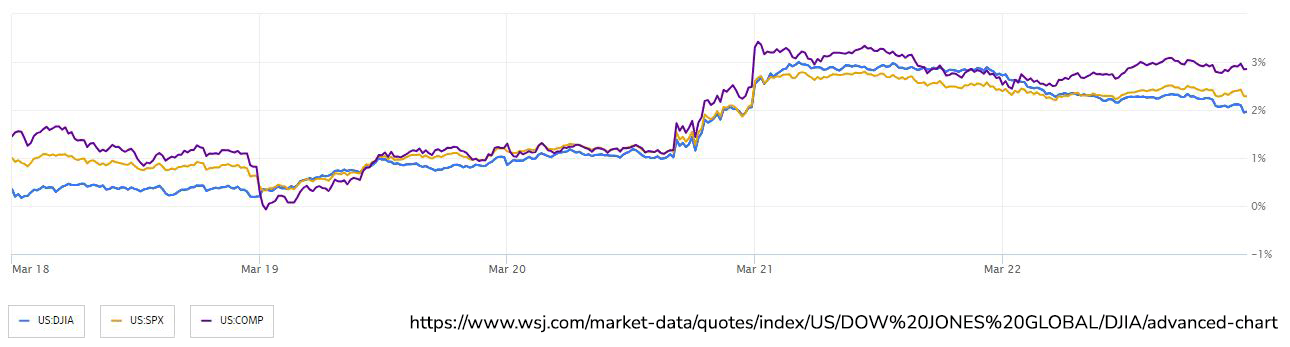

In the midst of a record-breaking surge in the stock market, US equities experienced a momentary pause on Friday, despite marking their most successful week in 2024. Speculation regarding the Federal Reserve's potential interest rate cuts as early as June fueled this rally. The S&P 500, having soared approximately 10% this year, exhibited a weekly gain of over 2%, prompting analysts to revise their targets amidst calls for a potential consolidation or pullback. The week concluded with traders closely monitoring statements from Federal Reserve officials, particularly focusing on any hints regarding monetary policy adjustments. Although Fed Chair Jerome Powell's remarks during a "Fed Listens" event omitted discussions on monetary policy, comments from Michael Barr, the Fed's vice chair for supervision, suggested forthcoming significant changes to capital requirements for lenders. Throughout this period, the S&P 500 closed below 5,235, with notable performers including Nvidia Corp., extending gains for an impressive 11th consecutive week, and FedEx Corp., bolstered by robust earnings and a substantial buyback plan. Conversely, companies like Nike Inc. and Lululemon Athletica Inc. faced declines due to weaker outlooks. Against this backdrop, Treasury 10-year yields declined, while the dollar approached its highest level of the year. However, amid this relative calm, US equity funds experienced significant outflows leading up to the highly anticipated Fed policy meeting, recording redemptions of approximately $22 billion. Following the Fed's decision, a market rally ensued as investors perceived the central bank's stance as less hawkish than anticipated, maintaining their forecast for three rate cuts in the year. Despite lingering concerns over elevated rates, recent data on housing, manufacturing, and labor markets pointed towards a resilient economy. Markedly, there has been a shift in market sentiment, with positive data viewed as indicative of a "soft landing," while lackluster data reinforces expectations of rate cuts.

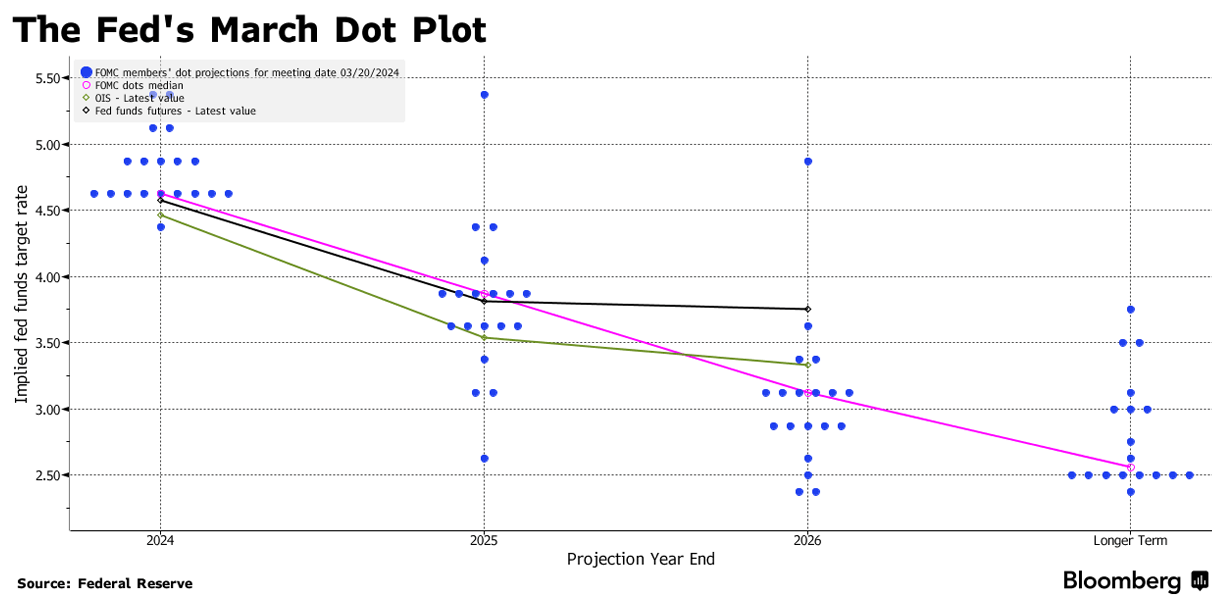

Despite solid growth and firmer-than-anticipated inflation, the Federal Reserve maintained its outlook for delivering interest-rate cuts later in the year. Most officials projected three rate cuts for the year while holding the benchmark federal-funds rate steady between 5.25% and 5.5% at last week’s meeting. The economic projections were closely watched by investors, particularly regarding the impact of recent inflation readings. Stocks rose following the Fed's announcement in relief that it did not exhibit any hawkish shift in rhetoric. Expectations for rate cuts remained high among investors, with speculation that the first cut could occur by June. Fed officials also adjusted their inflation and growth projections, expecting inflation to end the year slightly higher than previously anticipated and forecasting higher growth for 2024. However, some officials signaled fewer rate cuts than initially expected for this year and a slower pace for reductions next year. Fed Chair Jerome Powell emphasized progress in bringing down inflation but cautioned against premature action, stressing the importance of confirming sustained progress. The Fed's strategy of raising rates over the past two years aimed to combat high inflation but also led to concerns about economic downturns. Despite these concerns, economic growth has remained resilient, with inflation showing signs of decline recently. The debate within the Fed continues over whether to preemptively adjust rates amid mixed economic data. While housing prices and the stock market have surged, other indicators such as consumer spending and hiring surveys present a more tempered outlook. Fed officials must balance the risks of easing too soon or too slowly, with political pressure adding another layer of complexity.

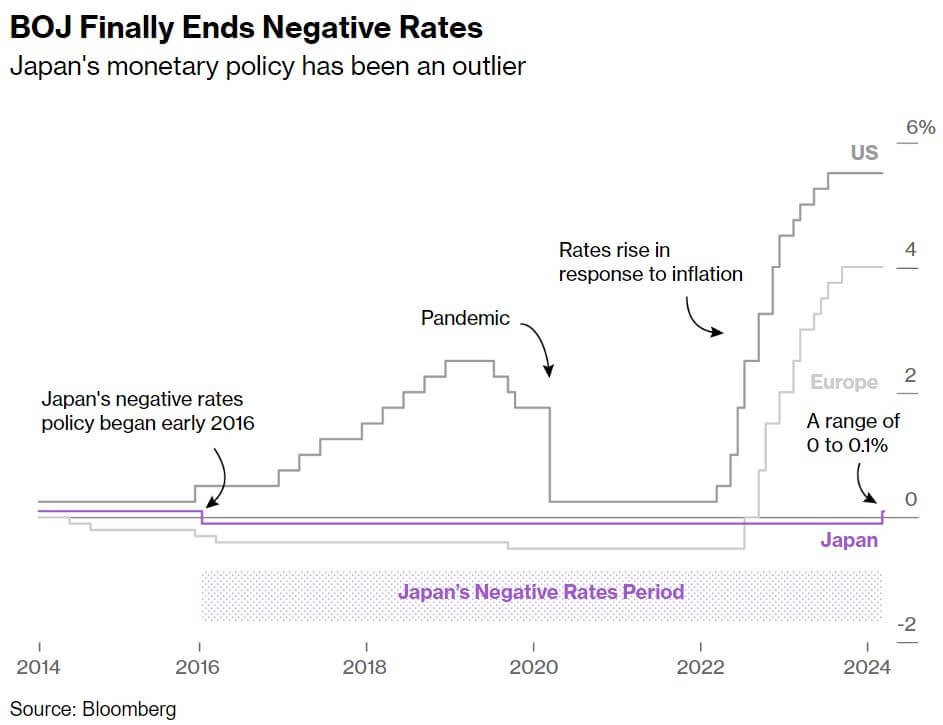

The Bank of Japan (BoJ) recently made a significant policy shift, signaling the end of its radical monetary experiment aimed at combating deflation. This move comes as inflation has consistently exceeded the BoJ's 2% target for the past 22 months and wage growth has reached its highest level in decades. The policy changes enacted by the BoJ include raising the key interest rate from negative to between zero and 0.1%, discontinuing the purchase of exchange-traded funds, and abandoning its yield-curve-control framework. The shift in policy reflects changes in the Japanese economy, which has gradually moved away from deflationary pressures. Although the economy still faces hurdles, such as sluggish consumption, positive signs such as rising inflation and wage growth indicate a departure from the deflationary trend. Notably, the BoJ's governor emphasized that the shift represents a return to "normal" monetary policy rather than the beginning of a tightening cycle. Japan's journey into deflation dates back to the 1990s following an asset bubble burst and financial institution failures. Now, with inflation seemingly embedded and the economy resilient enough to withstand the withdrawal of extreme measures, the BoJ's decision reflects confidence in the economic outlook. Despite being a major policy change, the immediate impact on financial markets is likely to be limited, as the change was well communicated ahead of time. The BoJ is not expected to embark on a major tightening cycle, meaning that Japanese rates will likely remain lower than the rest of the world. That should continue to keep a cap on the yen and Japanese benchmark government bond yields have remained stable in the range of 0.7% to 0.8%. Though interest rates are higher than they were previously, Japanese investors can still invest at higher rates abroad. This means that Japanese investors are unlikely to sell their large holdings of US government debt in favor of domestic bonds soon. Looking ahead, the BoJ aims to maintain an accommodative stance, with gradual adjustments to its policy framework expected.