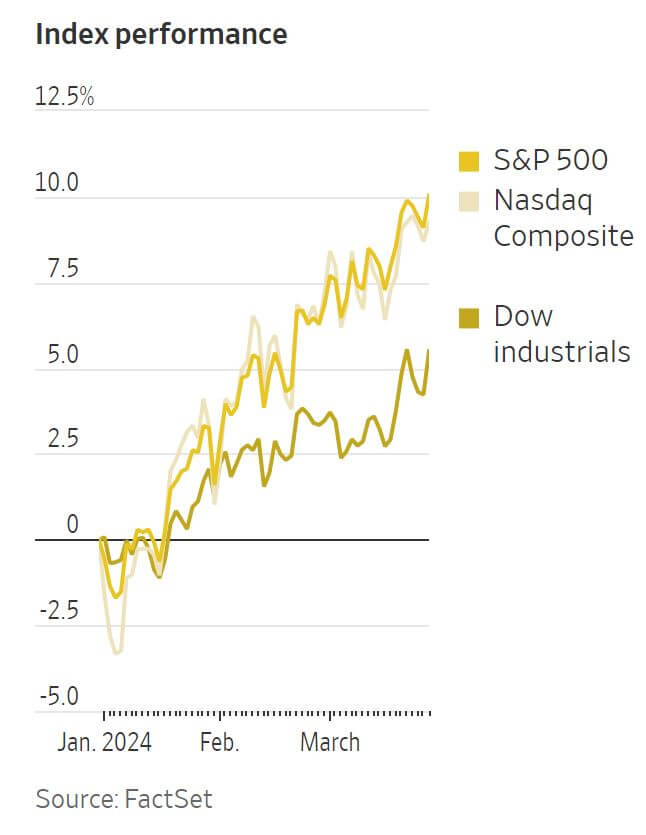

In the early months of 2024, investors witnessed an extraordinary surge in financial markets, surpassing even optimistic expectations. The S&P 500, a bellwether of U.S. equities, surged by an impressive 10% in the first quarter alone, marking its strongest start to a year since 2019. This surge was not confined to equities; cryptocurrencies like bitcoin and traditional safe-haven assets like gold also reached new highs, reflecting a broad-based rally across asset classes. What's particularly noteworthy is the breadth of this rally recently. It wasn't solely driven by a handful of large technology companies, as had been the case in previous years. Instead, nearly all sectors of the S&P 500 experienced gains, demonstrating the resilience and diversity of the market rally. Even small-cap and value stocks outperformed in recent weeks, indicating a broader market participation beyond the tech giants. Contributing to this bullish sentiment were factors such as robust corporate profits, advancements in artificial intelligence, and expectations of monetary policy easing by the Federal Reserve. Investors, buoyed by these factors, continued to pour capital into the markets, undeterred by occasional dips, which were quickly bought up. Despite the optimism, some investors are cautious about the sustainability of such momentum. They wonder whether future returns will be as lucrative, given the substantial gains already realized. Additionally, concerns linger about the valuation of stocks, particularly if corporate profits fail to meet expectations. Analysts anticipate continued earnings growth, but if fundamentals fail to keep pace with market optimism, the momentum could reverse swiftly. Nonetheless, experts remain optimistic about the market's prospects, citing historical trends and the underlying strength of the economy.

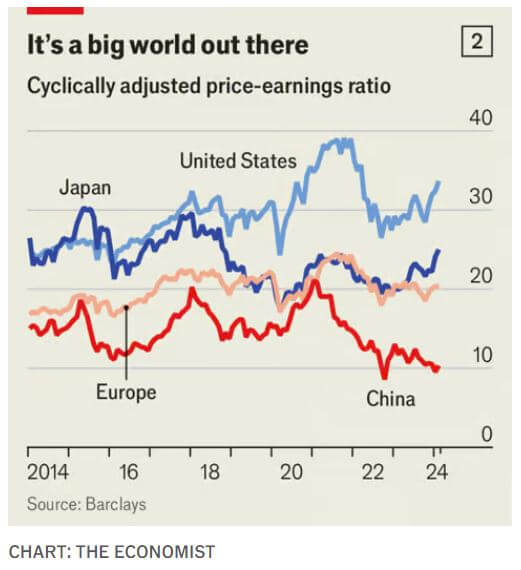

US stocks have continued to march higher this year, prompting skepticism among professional investors. Bank of America's monthly survey of fund managers reveals concerns among 40% of fund managers that AI stocks may be in a bubble, prompting doubts about future gains in the S&P 500 index. This apprehension raises questions about the availability of stocks offering good value in the current market environment. Value stocks, traditionally defined by low prices relative to underlying assets or earnings, have fallen out of favor compared to growth stocks in recent years. Despite brief periods of resurgence, value stocks have consistently underperformed, leading some to declare value investing obsolete. Critics argue that traditional valuation metrics overlook intangible assets and research spending crucial to modern firms, while investment tools quickly arbitrage potential returns. The cyclically adjusted price-to-earnings (CAPE) ratio, a key metric indicating overvaluation, is historically high for the S&P 500, raising concerns about future returns. Victor Haghani of Elm Partners suggests diversifying investments globally, as valuations are lower outside the U.S. He highlights disparities in market valuations despite similar earnings contributions from American and non-American companies, suggesting potential for repricing for international stocks. Hugh Gimber of J.P. Morgan Asset Management challenges the notion that lower valuations of European firms reflect sectoral differences, noting persistent discounts compared to American counterparts across sectors. This suggests potential undervaluation rather than lack of dynamism. Similarly, emerging markets offer value opportunities, benefiting from global trends with more reasonable valuations than in the U.S. Examples such as Mexico, Vietnam, South Korea, Taiwan, and Japan illustrate regions with undervalued assets potentially poised for growth. Despite the perceived natural superiority of American markets, the March Bank of America survey showed increased rotation into European and emerging-market stocks suggests a shifting investor sentiment toward undervalued assets globally.

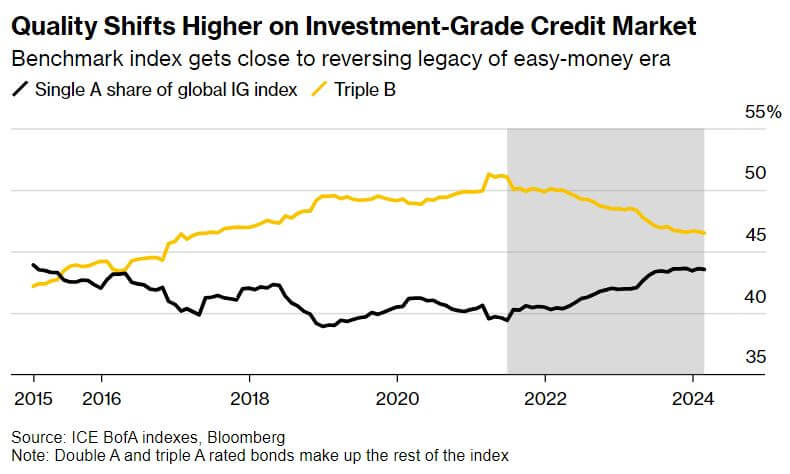

The current state of the global high-grade credit market reflects a notable enhancement in quality, reminiscent of the early phases of the era marked by abundant liquidity. Single A bonds are close to becoming the largest part of investment grade indexes for the first time in roughly a decade, while the share made up of the riskiest BBB credits is shrinking. This shift lends credence to assertions that valuations may not be as overstretched as perceived, due to the overall increase in credit quality. Thomas Neuhold of Gutmann Kapitalanlage AG notes that rating agencies are monitoring companies' debt ratios, which exhibit an improving trajectory. This favorable development contributes to the perception of reasonable spreads. The prospect of further rate reductions by central banks bolsters confidence, allowing for a potential tightening of spreads. While the compensation for investing in global investment-grade companies vis-à-vis government bonds has dwindled to a two-year low, the quality of the index has markedly improved. This contrasts sharply with the easy-money era, characterized by a proliferation of debt issuance even by the most vulnerable firms to take advantage of low interest rates. Although remnants of that period persist, recent years have witnessed a recuperation in credit ratings. Data suggests that major rating agencies are on pace to issue more credit upgrades than downgrades among high-grade firms for the fourth consecutive year. Despite lingering uncertainties such as upcoming elections and geopolitical tensions, the prevailing sentiment remains buoyant, supported by expectations of rate cuts and subdued inflation. Market observers anticipate sustained demand for bonds from well-capitalized portfolio managers, a factor likely to exert continued pressure on spreads. While challenges and uncertainties persist, the prevailing demand dynamics are poised to sustain tight valuations in the foreseeable future.