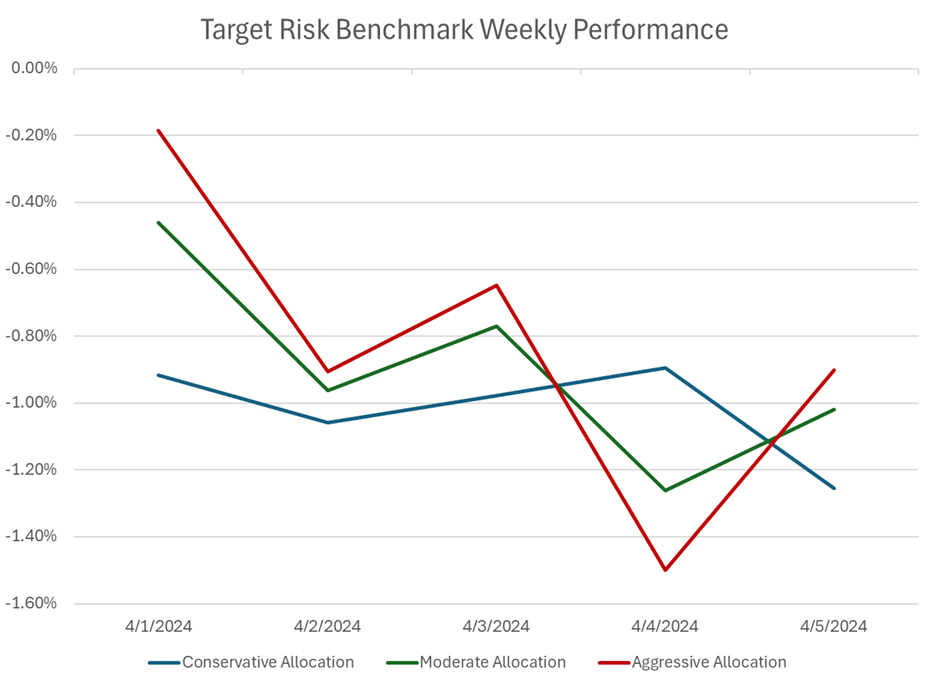

A volatile week for markets resulted in divergent results for investors with balanced portfolios with differing risk tolerances. The aggressive risk benchmark below has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. The moderate risk benchmark is made up of a roughly 60/40 global stock and bond split of the same indices, while the conservative risk benchmark has a roughly 90% allocation to the US Aggregate Bond Index and a small exposure to global equity benchmarks. All three risk tolerances fell for the week as geopolitical tensions in the Middle East continued to drive up oil prices. Those concerns dragged down the prices of both stocks and bonds. However, on Friday the strong US jobs report showcased continued momentum in the US economic trajectory. That resulted in a rally in equity prices, but a selloff in bonds as the prospect of interest rate cuts was pushed back further into the year. Notably, international equities had a smaller loss for the week, even after the strong rally in the Russell 3000 on Friday. This resulted in both the aggressive and moderate risk tolerances trimming weekly losses to end the week, while the conservative allocation lost more ground. The aggressive allocation limited its loss for the week to -0.9%, while the moderate allocation lost -1.02% and the conservative allocation gave up -1.25%.

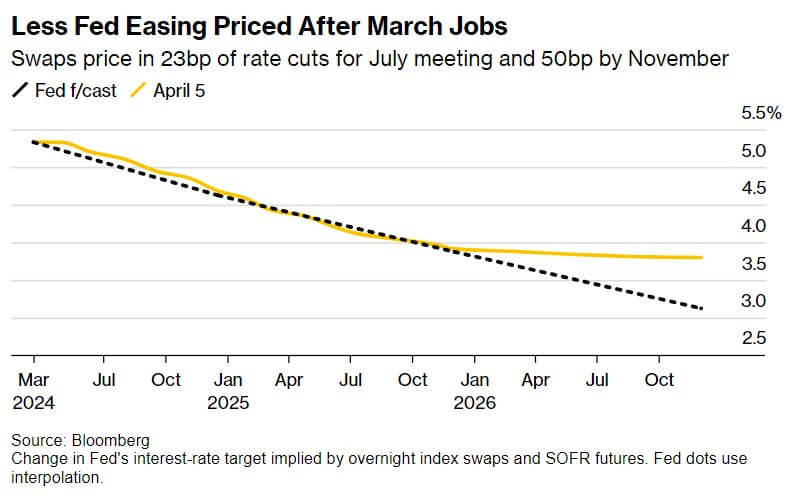

The latest US employment report, released by the Labor Department, indicated robust job growth in March, surpassing economists' expectations. The addition of 303,000 jobs contributed to a decrease in the unemployment rate to 3.8%. However, wage growth has remained modest, with average hourly earnings rising by 0.3% from the previous month and 4.1% from a year earlier, representing the smallest yearly increase since June 2021. The labor force participation rate also ticked up to 62.7%, the first increase since November. Contrary to conventional wisdom, sustained job creation has occurred alongside cooling wage gains and a rising unemployment rate over the past year. This divergence suggests a potential increase in the supply of available workers, possibly influenced by factors such as immigration. Despite a high number of job openings, the rate of job quits has returned to pre-pandemic levels, indicating a moderation in labor market competitiveness among businesses. Moreover, employment growth has been concentrated in "high-touch" sectors such as private education, healthcare, leisure, and hospitality, which require in-person interactions. While employment in these sectors initially declined during the pandemic, recent growth suggests a potential recovery, particularly in healthcare due to the aging population's increasing needs. Nonetheless, investors remain cautious, particularly regarding the potential impact on Federal Reserve interest-rate policy. A strong labor market could heighten concerns about inflation, as increased consumer spending power may fuel price pressures. Additionally, a robust job market provides the Fed with greater flexibility in delaying interest-rate cuts. Following the release of the jobs data, Treasuries sold off across the yield curve, but the relatively modest wage gains limited the increase in yields. Swaps contracts indicate that traders now only put a 52% chance of a rate cut from the Fed in June, but a near 100% chance of a cut in July. The monthly survey by BMO Capital Markets showed that 57% of investors would buy bonds if yields rose following the jobs report, indicating that the current level of yields is considered attractive by some despite a possible delay in the Fed cutting rates.

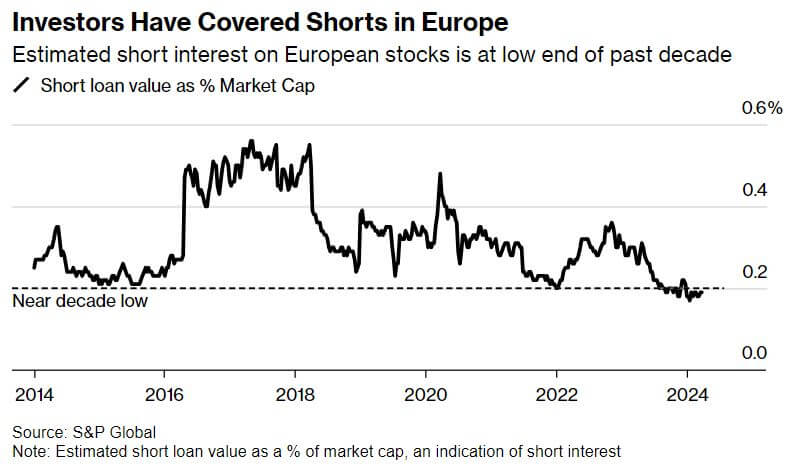

Investors are increasingly turning their attention towards European equities, anticipating a shift in the global equity rally from the US to Europe. Hedge funds, in particular, are exhibiting the highest exposure ever to European stocks relative to a global benchmark, while mutual funds are also significantly increasing allocations to the region. This trend is partly fueled by concerns about the US market's valuation resembling that of the dot-com bubble era, prompting investors to seek alternatives. Euro area shares have recently outperformed their US counterparts, with a 4% rise in March, and investors foresee further gains driven by an anticipated rebound in economic growth stimulating corporate profits. The current reliance of the S&P 500 Index on a select group of expensive tech stocks heightens the appeal of Europe's more diverse market composition. The Stoxx 600 Index, despite its recent gains, still appears attractively valued with a forward 12-month price-to-earnings ratio only slightly above its long-term average. Europe's heavier weighting in cyclical sectors positions it favorably as economies like Germany and the UK show signs of avoiding prolonged recession, coupled with anticipated global growth. Moreover, declining short positions on European stocks suggest improving sentiment towards the region, with short interest at its lowest level in at least a decade. Looking ahead, both the US and Europe are expected to witness robust earnings growth, with analysts projecting an 8.3% increase for S&P 500 firms and a 4% growth for Stoxx 600 earnings in 2024. Despite the optimism for the US market, there is recognition of the potential for Europe to catch up, offering intriguing investment opportunities for those seeking diversification and relative value.