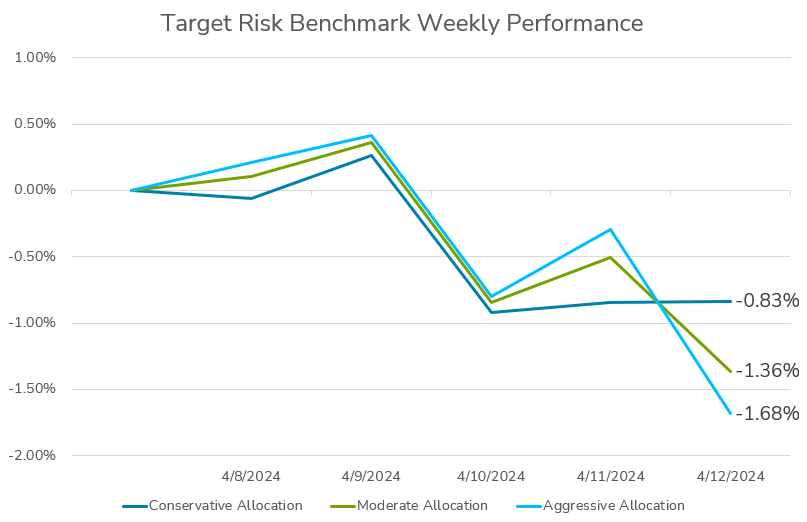

Last week proved to be another difficult week for investors with balanced portfolios. The aggressive risk benchmark below has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. All three risk tolerances experienced small gains to start the week as investors awaited the release of the March Consumer Price Index data on Wednesday. When inflation came in hotter than expected for a third consecutive month, stocks and bonds sold off in tandem, resulting in comparable losses across the three risk benchmarks. Equities recovered somewhat on Thursday, with the aggressive and moderate risk benchmarks benefiting most. However, geopolitical tensions came to the fore on Friday, with fear of an imminent direct attack on Israel from Iran weighing heavily on risk appetite. The flight to safety saw strong demand for haven assets such as bonds, pushing the yield on the US 10 Year Treasury note back below 4.5%, while stocks sold off again. The conservative risk benchmark benefitted from this dynamic, limiting its weekly losses to -0.83%. The larger equity allocation in the moderate and aggressive risk tolerances benchmarks resulted in their losses increasing for the week to -1.36% and -1.68%, respectively.

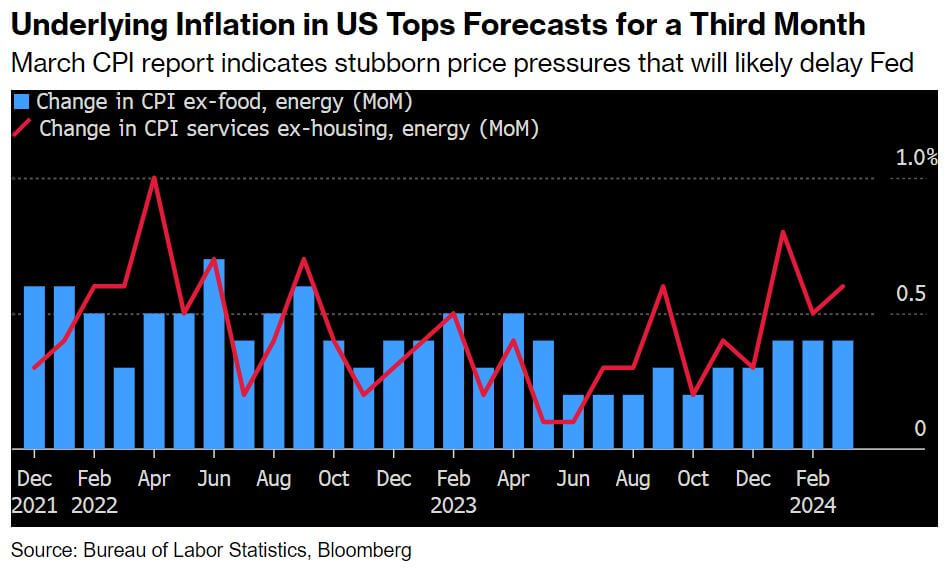

The Consumer Price Index (CPI), a pivotal metric gauging the cost of goods and services across the economy, surged by 3.5% in March compared to the previous year, slightly surpassing economists' projections and marking an escalation from February's 3.2%. Core prices, excluding volatile food and energy sectors, increased more than expected on both monthly and yearly scales, holding steady at 3.8% year on year. Consequently, financial markets reacted with a downturn in stocks and yields on U.S. government bonds rose, reflecting anticipation that the data might delay or mitigate future interest rate reductions. Futures contracts linked to the federal funds rate revealed a consensus among traders projecting rates to conclude the year around 5%, implying a possibility of merely one or two quarter-point cuts for the year, a stark contrast to earlier expectations of six or seven rate reductions. Although previous inflation readings in January and February were dismissed by Fed officials as potentially influenced by seasonal factors, the consecutive third month of above-expectations inflation data undermines such explanations. Consequently, the Fed may hold rates at their current level, the highest in 23 years, until clearer economic vulnerabilities emerge. Analysts highlighted concerning details within the report, particularly noting the unexpected rise in the overall core index despite declines in certain goods prices. Furthermore, persistent increases in shelter costs contradicted predictions of a slowdown, contributing to ongoing inflationary pressures.

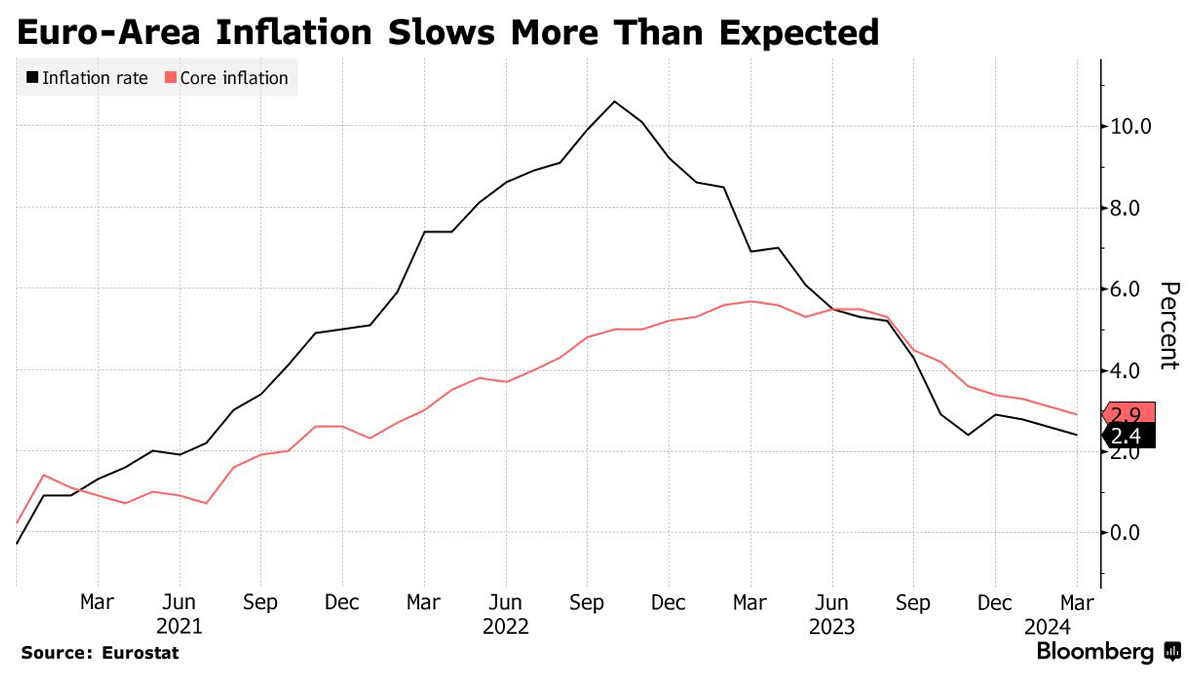

The European Central Bank (ECB) opted to maintain its record high interest rates last week but hinted at a possible shift towards rate cuts, contrasting with the Federal Reserve's less clear trajectory regarding monetary easing. The ECB's stance reflects a divergent economic environment compared to the Fed, with cooling inflation and stagnant economic growth in Europe. ECB officials are considering lowering the key rate as early as June to stimulate the economy amid declining inflation across the continent, potentially positioning the ECB ahead of the Fed, which has yet to specify a rate cut timeline. The ongoing debate holds significant implications for financial markets, as evidenced by fluctuations in bond yields and currency exchange rates. ECB President Christine Lagarde's assertion of the ECB's autonomy in rate decisions notwithstanding, the interconnectedness of the global economy, particularly its reliance on the U.S. dollar, imposes constraints on divergence from the Fed's policy trajectory. Although a preemptive rate cut by the ECB could stimulate the European economy, it may trigger capital outflows and further weaken the euro. While beneficial for exports, this could inadvertently elevate inflation by increasing import costs, necessitating a delicate balance between promoting economic growth and stabilizing inflation. Investors currently anticipate multiple ECB rate cuts this year, with a June cut almost fully priced in, contrasting with subdued expectations for Fed rate cuts.