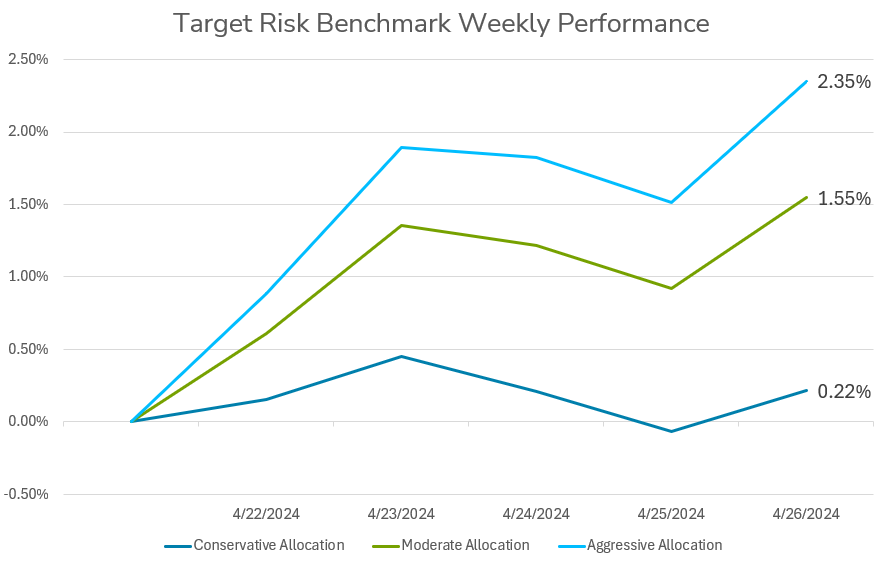

Investors in balanced multi-asset portfolios enjoyed a substantial recovery last week after two consecutive weeks of losses, as shown by the performance of the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Hotter-than-anticipated quarterly inflation data prompted a bond selloff in the middle of the week, driving yields on the 10-year Treasury note above 4.7%, and causing U.S. stock indices to decline. That bond selloff weighed on the conservative target risk benchmark in particular. However, the aggressive and moderate target risk benchmarks benefitted from the recent rally in major technology companies, including Microsoft and Alphabet, which buoyed the stock market, leading to the best week for equities in 2024. Both companies emphasized that investments in AI and cloud computing were benefiting profits, supporting enthusiasm for the AI trade and reassuring investors about the technology sector's fundamentals amidst concerns about the macroeconomic environment. Those two companies’ strong quarterly results contrasted with Wall Street’s adverse reaction to both Netflix and Meta, which fell last week following earnings releases. That shows a continuing divergence in the market performance of the former Magnificent Seven as the companies’ bottom lines follow differing trajectories. Bond yields declined on Friday in relief that the March PCE figures didn’t come in worse than forecasted, allowing the conservative target risk benchmark to recover from its earlier losses.

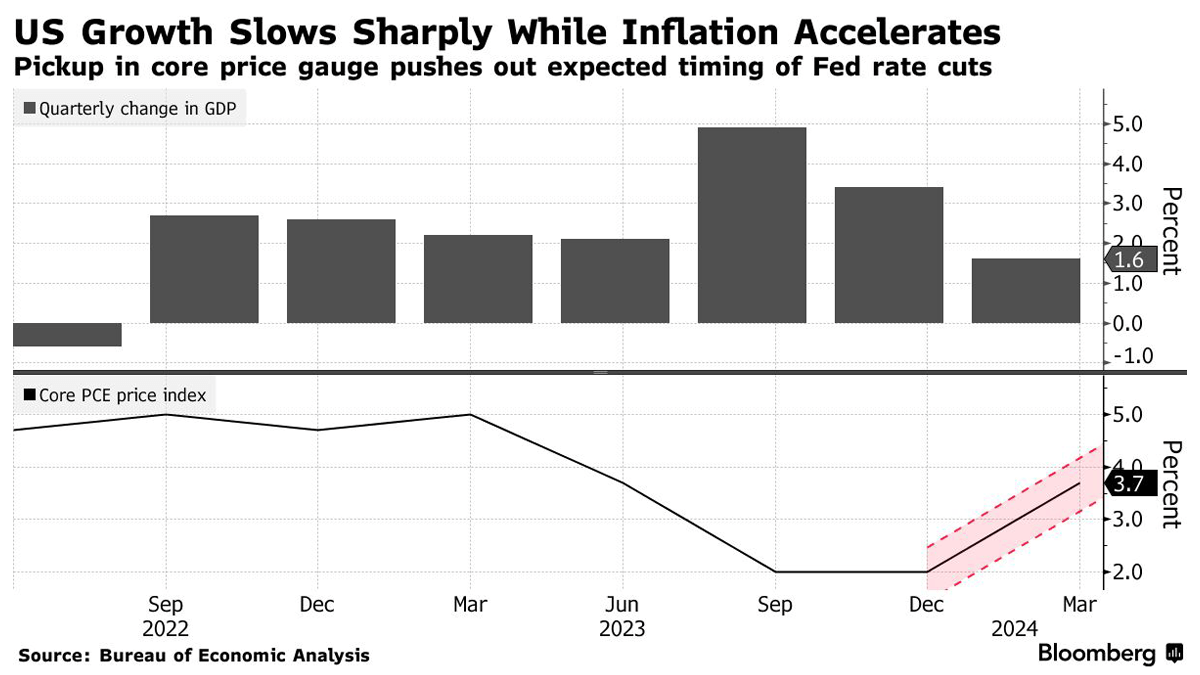

The U.S. economy witnessed a notable slowdown in the first quarter of 2024, with Gross Domestic Product (GDP) expanding at a modest annualized rate of 1.6%, falling short of economists' expectations. This deceleration was primarily attributed to slower-than-forecasted growth in personal spending, which increased by 2.5%. Additionally, a widening trade deficit had a significant negative impact on growth, marking the largest subtraction since 2022. Of particular concern was the acceleration of underlying inflation, as indicated by a 3.7% annualized increase over the first quarter in the Personal Consumption Expenditures (PCE) price index, excluding food and energy, surpassing expectations for an increase of 3.4%. This uptick in inflation may intensify pressure on Federal Reserve policymakers to delay potential interest rate cuts, with market participants adjusting their expectations accordingly. Notably, the surge in service-sector inflation, excluding housing and energy, contributed significantly to the overall inflationary pressure. The GDP report highlighted several noteworthy trends, including the first decline in federal government spending in two years and consecutive quarters of drag from business inventories. Though a decrease in inventories could signal positive news for future economic performance, caution prevailed among economists regarding the volatility of such figures throughout the year. Adjusting for these factors, inflation-adjusted final sales to private domestic purchasers, a key indicator of underlying demand, rose at a 3.1% rate, underscoring continued resilience in underlying demand in the economy. Consumer spending remained robust, particularly in healthcare, insurance, and other services, indicating sustained strength propelled by years of hiring and wage growth. However, a slowdown in spending on goods like cars and gasoline restrained overall growth. Persistent inflation, coupled with signs of economic cooling such as declining low-income savings rates, subdued home sales, and sluggish wage growth, presents a challenging landscape for policymakers and investors alike, especially amidst uncertainty surrounding future interest rate adjustments and their potential impact on various sectors of the economy.

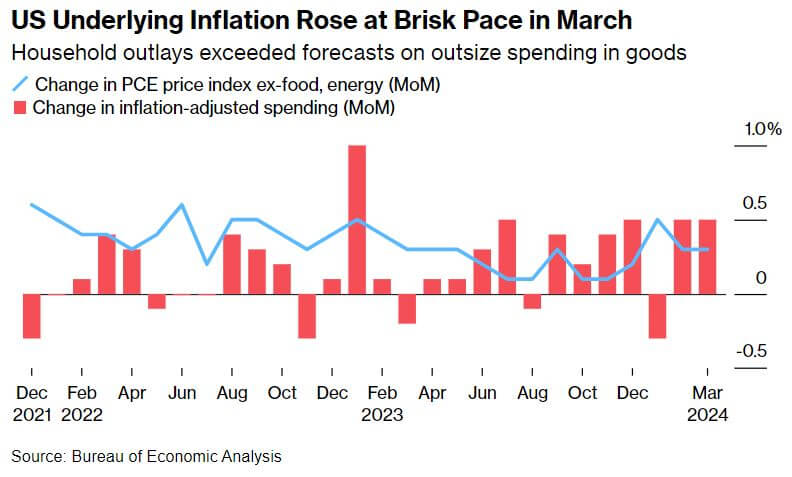

In March, the United States witnessed a notable uptick in its preferred metric for gauging underlying inflation, a concerning development likely to prolong any consideration of interest rate reductions by the Federal Reserve. The core personal consumption expenditures (PCE) price index, excluding volatile food and energy components, surged by 0.3% compared to the previous month, and by 2.8% from the preceding year. The broader PCE price measure also exhibited a comparable 0.3% rise from February, reaching a 2.7% increase from the previous year. Inflation-adjusted consumer spending registered a substantial 0.5% increase, the largest surge observed this year. These figures may lead Federal Reserve policymakers to defer any interest rate cuts until later in the year. Investor response to the data was largely positive, as the inflation figures came in in-line with estimates, providing relief following Thursday's quarterly data suggesting upside risks. Of particular significance to central bankers is the services inflation excluding housing and energy, which experienced a 0.4% uptick from February, indicating a potential acceleration compared to the preceding month. The robust labor market continues to underpin household spending, despite elevated interest rates and rising prices. Notably, merchandise spending surged by 1.1% in March, driven by sustained spending on durable goods, while services spending saw a modest 0.2% increase. Wage growth remains supported by healthy demand for workers, with overall incomes rising by 0.5%, primarily fueled by a 0.7% increase in wages and salaries.

However, the decline in the saving rate to 3.2%, the lowest since October 2022, underscores the strain on households amid persistent inflationary pressures. Looking ahead, policymakers aim to temper inflation to their 2% target without derailing economic growth.