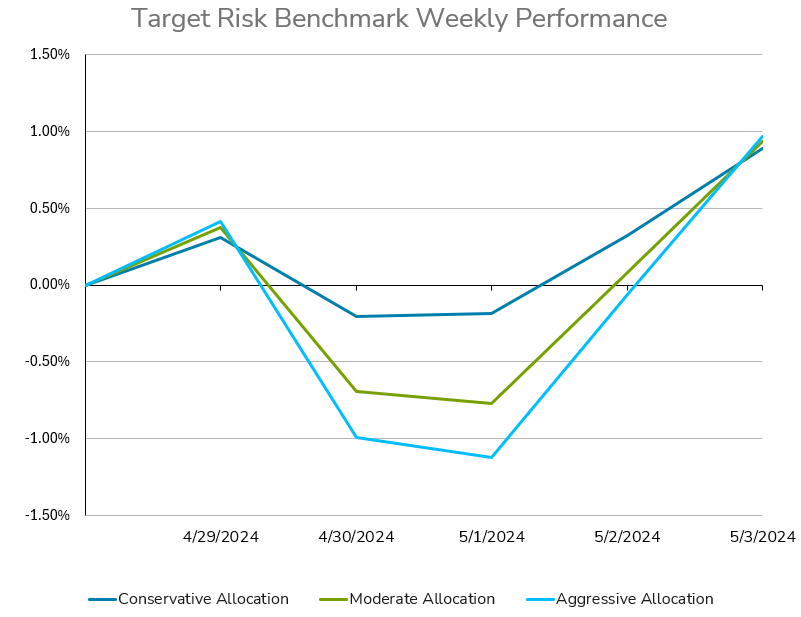

Investors in balanced multi-asset portfolios had a roller coaster week with markets on edge approaching the Federal Reserve FOMC meeting last week, as can be seen with the performance of the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to the Russell 3000 and MSCI All Country World Index Ex USA, with limited exposure to the US Aggregate Bond Index. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds.

Stubbornly high inflation has weighed on sentiment in recent weeks, leading to fears that the Fed may hold interest rates higher for longer, or even open the door to further interest rate hikes. Markets rallied in relief that the Fed did not adopt a more hawkish tone when holding rates steady last week, which led all three target risk benchmarks to recoup earlier losses on Thursday. More good news arrived on Friday, with updated labor market figures coming in softer than expected. That led to further relief that the US economy may still be trending towards a soft landing rather than overheating. This led to a significant decrease in bond yields, and a repricing in swaps implying two rate cuts by year end, up from just one cut earlier in the week. Equities rallied strongly, boosted in part by an announcement from Apple of a large share buyback program. The VIX equity volatility gauge also fell to a one month low.

All three target risk benchmarks recovered from earlier losses in the week to finish with gains. The conservative target risk benchmark finished with a gain of 0.89%, the moderate target risk benchmark ended with a gain of 0.94%, and the aggressive target risk benchmark returned 0.96% for the week.

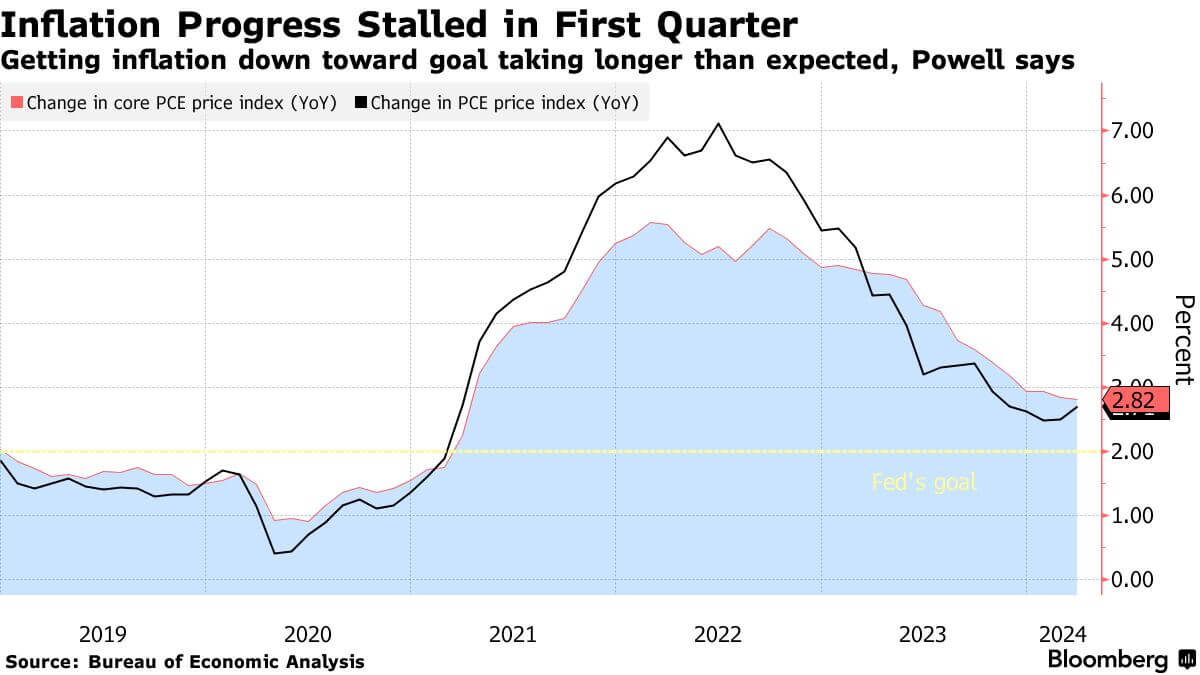

The Federal Reserve, led by Chair Jerome Powell, maintained its stance on interest rates last week, signaling a prolonged period of elevated borrowing costs amidst persistent inflation concerns. Following the latest Fed meeting, officials opted to keep the target range for the benchmark federal funds rate unchanged at 5.25% to 5.5%, where it has remained since July of last year. Powell emphasized the need for additional evidence of cooling inflation before considering any rate cuts from the current two-decade high. Powell dismissed suggestions that current Fed policies are overly restrictive, with continued strong economic growth and hiring. He reiterated the Fed's readiness to adjust borrowing costs as well if there's unexpected weakness in the labor market. Powell outlined that the next likely move by the Fed would not be an interest rate hike, and that any future rate hikes would require compelling evidence that current policies aren't effectively curbing inflation. Powell didn't commit to a timeline for rate reductions. This cautious approach signals a shift towards maintaining borrowing costs at current high levels for a longer duration. Previously, Powell had suggested potential rate cuts in the year, but his recent statements lacked specificity. Regarding the Fed's balance sheet, officials outlined plans to decelerate the reduction of assets in a welcome dovish shift for markets. The runoff of Treasuries will decrease to $25 billion per month starting in June from its current rate of $60 billion, aiming to mitigate potential financial market turbulence. However, the cap for the runoff of mortgage-backed securities remains unchanged at $35 billion per month. While the economy continues to expand, inflation progress has stagnated in 2024 after a rapid cooling towards the end of 2023.

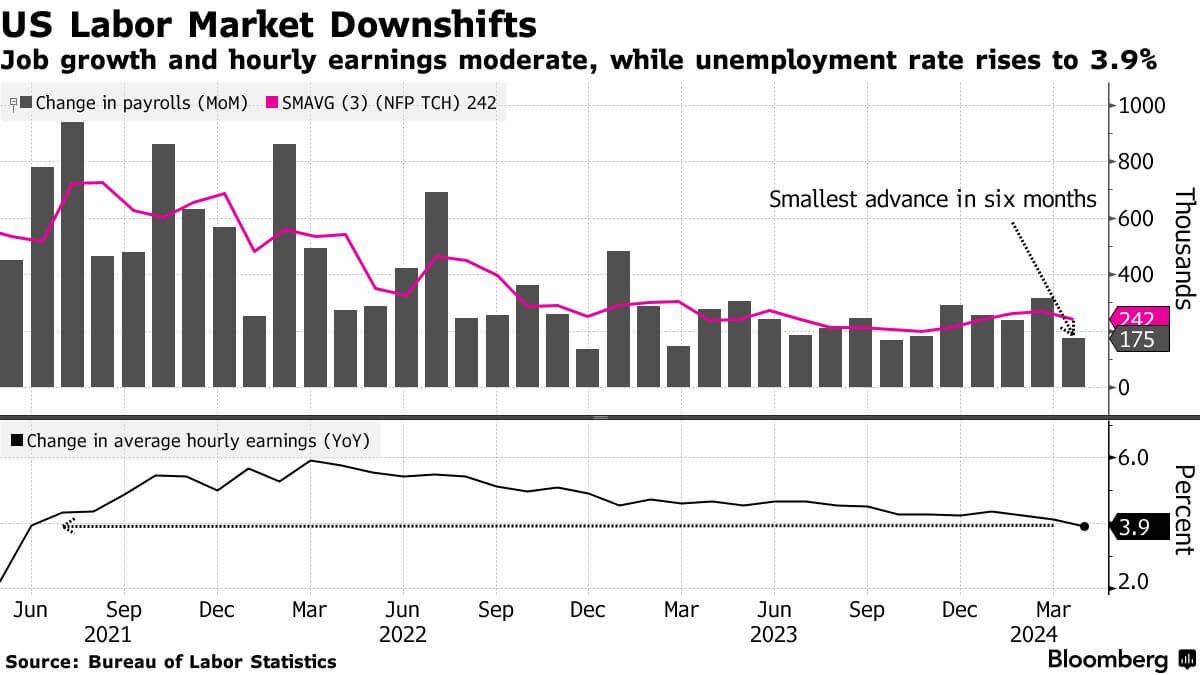

In April, US employers exhibited a reduction in hiring activity, leading to an unexpected rise in the unemployment rate, indicative of a potential moderation in the labor market following a robust start to the year. The Bureau of Labor Statistics on Friday reported a meager increase of 175,000 in nonfarm payrolls, marking the smallest gain in six months. That fell far short of the consensus estimate for an increase of 240,000. The first quarter of the year exhibited robust economic indicators, with an average of 269,000 payrolls added monthly. Wage growth also accelerated in the first quarter, with the employment-cost index rising 1.2% compared to the prior three months, and 4.2% from a year earlier. Powell, emphasizing the importance of moderating wage growth in achieving inflation objectives, noted the need for a gradual downward adjustment in wage growth rates. Despite expectations for stronger wage growth, April's report indicated a 0.2% increase from March and a 3.9% rise from a year ago, the slowest pace since June 2021. Moreover, the service-sector employment report by the Institute for Supply Management corroborated the weakening trend observed in the labor market, indicating a potential constraint on economic growth due to a moderation in demand. However, analysts caution against overinterpreting a single month's data, emphasizing the need for sustained trends before considering policy adjustments. Overall, April's weaker-than-expected nonfarm payrolls, combined with a higher unemployment rate, suggest a gradual normalization of the labor market, potentially influencing the Federal Reserve's monetary policy stance. A sustained moderation in hiring and wage growth, coupled with increased workforce participation, may temper inflationary pressures, and increase the likelihood of interest rate cuts later this year.