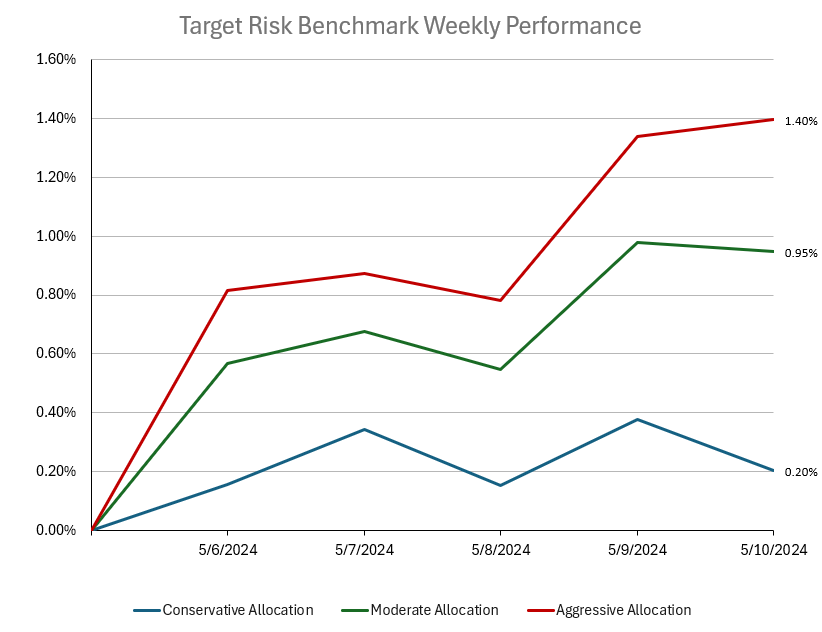

Balanced portfolios ended the week on a positive note despite rising inflation expectations and a weak US consumer sentiment report. For portfolios with a heavier bond weight, the returns were lower as yields rose following the University of Michigan's Consumer Sentiment report, which declined to a six-month low. Short-term inflation expectations have picked up, but slowdowns in other industries have again raised expectations for Fed interest rate cuts. Portfolios with higher allocations to equity markets had a strong week as the S&P 500 notched its third straight week of gains and the Dow Jones Industrial Average rose for an eighth straight session. The conservative target risk benchmark finished with a gain of 0.20%, the moderate target risk benchmark ended with a gain of 0.95%, and the aggressive target risk benchmark returned 1.40% for the week.

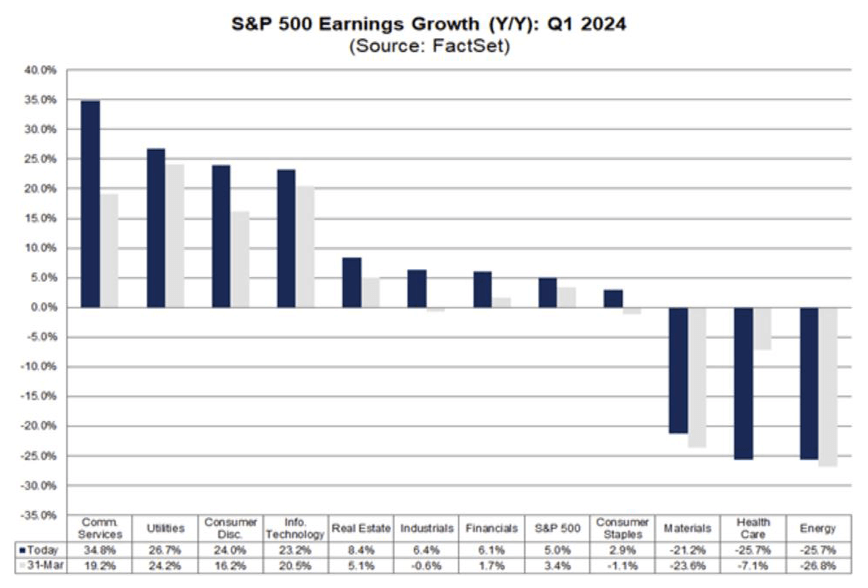

The latest updates on S&P 500 earnings reveals a continued strong performance relative to expectations during the first quarter of 2024. The majority of S&P 500 companies have reported earnings above estimates, with both the percentage of positive earnings surprises and the magnitude of these surprises surpassing 10-year averages. This has resulted in higher reported earnings for the index compared to previous periods, with the highest year-over-year growth rate since Q2 2022. Positive earnings surprises across multiple sectors, notably Health Care and Consumer Discretionary, have contributed significantly to the overall growth rate of the index. Regarding revenues, while a majority of S&P 500 companies have reported revenues above estimates, the percentage is slightly below historical averages. Positive revenue surprises, particularly from the Financials sector, have contributed to an increase in the overall revenue growth rate. Looking forward, analysts anticipate strong year-over-year earnings growth rates for subsequent quarters in 2024, with expectations for double-digit growth in CY 2024. The forward 12-month P/E ratio remains above historical averages but has decreased slightly since the end of the first quarter.

The Magnificent Seven group of major technology firms continued their stretch of strong earnings in the first quarter. These companies, including Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla, have contributed substantially to the S&P 500's overall performance. The robust earnings performance can be attributed to several factors, including resilient profit margins, particularly among large-cap companies with relatively low leverage and fixed debt structures. However, small businesses, with higher leverage and more floating debt, may face greater challenges in such economic conditions. While the strong earnings growth of the Magnificent Seven has driven overall market performance, there are indications that this trend may be losing momentum, with other companies beginning to strengthen. Bank of America analysts anticipate a slowdown in earnings growth for the major tech firms, suggesting a potential broadening of market performance.

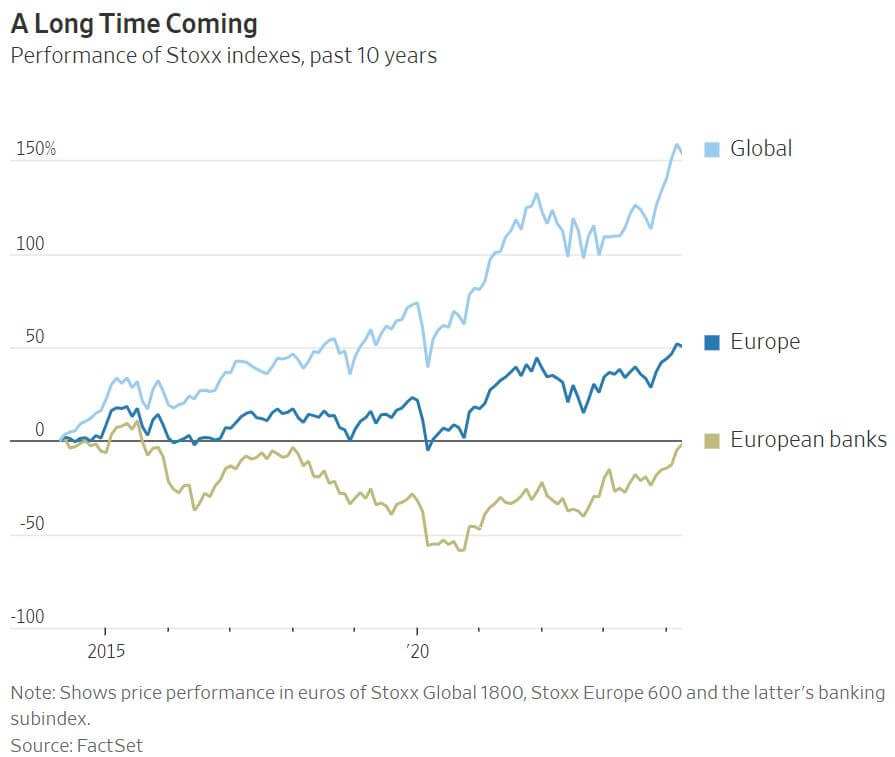

In recent years, European banks have undergone a remarkable transformation, emerging from a prolonged period of stagnation and adversity. This resurgence is marked by a series of strategic initiatives aimed at revitalizing the financial sector. European banks have diligently cleansed their balance sheets, implemented cost-cutting measures, and refocused efforts on enhancing loan profitability. The resurgence of European banks has not only benefited established investors but has also attracted a wave of new interest from both institutional and retail investors. The allure of potentially lucrative returns, coupled with still-depressed share prices and promising payouts, has enticed a diverse array of investors into the market. Leading the charge among investors are hedge funds like Basswood Capital Management and value investors such as Pzena Investment Management and Smead Capital Management, that foresaw the potential for growth in European banks when they were undervalued and out of favor. These early investors have reaped significant rewards from contrarian bets on the sector's recovery. The turnaround can be attributed to a combination of factors, including rigorous cost-cutting measures, the disposal of non-performing assets, and stricter regulatory standards that have bolstered capital reserves. This improved financial footing has positioned European banks to capitalize on favorable market conditions, particularly as benchmark interest rates turned positive in 2022. Reflecting newfound stability and profitability, European banks are expected to allocate substantial sums toward dividends and share buybacks this year, underscoring their commitment to enhancing shareholder value. Moreover, the prospect of increased merger and acquisition activity could further amplify investor returns, particularly for stakeholders in smaller lenders. While challenges remain, particularly regarding future interest rate changes, the prevailing sentiment is one of cautious optimism, with investors increasingly recognizing the potential for substantial returns in the sector's ongoing recovery.