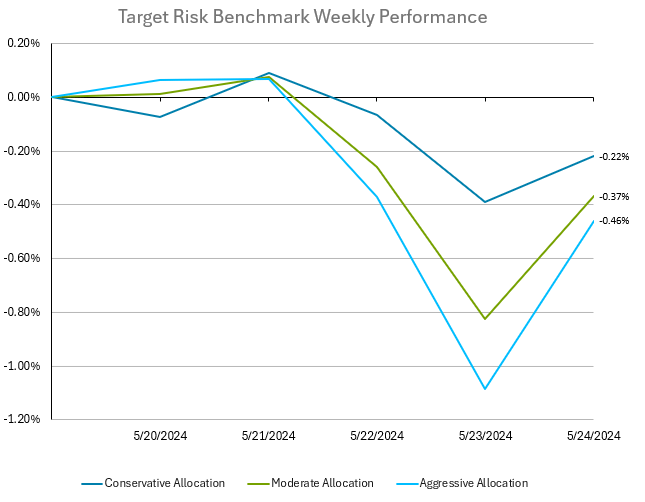

Investors in balanced multi-asset portfolios experienced mild losses last week after several strong weeks across all asset classes. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation bonds. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Recent data indicating that American consumers have tempered their inflation expectations has positively impacted stock markets, fostering optimism about potential Federal Reserve rate cuts within the year. The University of Michigan reported that consumers now anticipate a 3.3% annual inflation rate over the next year, down from the previous 3.5% projection. This revision has lessened pessimism about inflation and suggested that consumer spending might slow, thereby reducing inflationary pressures from demand. Consumer sentiment in May reflected growing concerns about the labor market and the likelihood of prolonged high interest rates. This sentiment could potentially lead to reduced consumer spending in the coming months. Market analysts emphasized the ongoing anxiety surrounding Fed policies. Despite this, corporate earnings have remained resilient. While US stocks as represented by the Russell 3000 Index recovered Friday to limit losses for the week to -0.16%, international equities, represented by the MSCI ACWI ex USA Index, ended down -1.02% for the week. The Bloomberg US Aggregate Bond Index had a loss for the week of -0.2%.

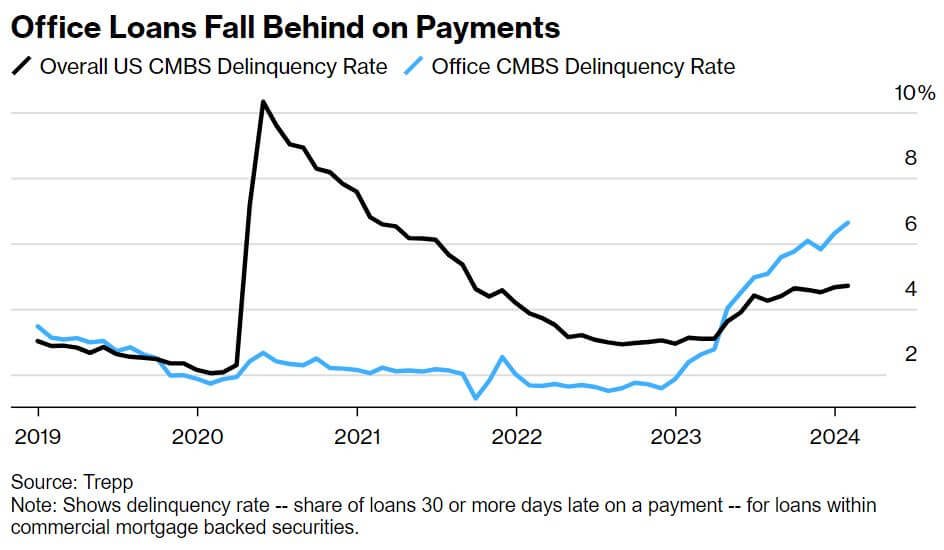

For the first time since the financial crisis, AAA-rated commercial mortgage-backed securities (CMBS) are experiencing significant losses. This is highlighted by the recent performance of a $308 million note secured by a mortgage on the 1740 Broadway building in Manhattan. Investors received back less than 75% of their initial investment, marking a historic post-crisis loss for top-rated bonds, as reported by Barclays Plc. Lower-tier creditors faced total losses. This event underscores the severe distress in segments of the US commercial real estate market, particularly older office buildings with a single anchor tenant, such as 1740 Broadway. Analysts predict more losses as additional loans are sold at significant discounts. With $700 billion in non-agency CMBS and $3 trillion in commercial mortgages on bank balance sheets, even minor increases in losses could impact the financial system long-term, though a repeat of the 2008 financial crisis is not expected. The delinquency rate for office loans in CMBS reached 6.4% in April, the highest since 2018, while 31% of all office loans in CMBS were distressed as of March, up from 16% the previous year, according to KBRA Analytics. Cities like Chicago and Denver are particularly affected, with delinquency rates of 75% and 65%, respectively. Factors contributing to these losses include rising interest rates and decreasing cash flow, resulting in significant equity losses and impaired secured debt investments, according to Harold Bordwin of Keen-Summit Capital Partners. Industry experts warn that similar losses may affect other AAA-rated CMBS tied to malls and office spaces. The ongoing challenges in the commercial real estate market are expected to extend, affecting numerous office deals and revealing hidden risks in the market.

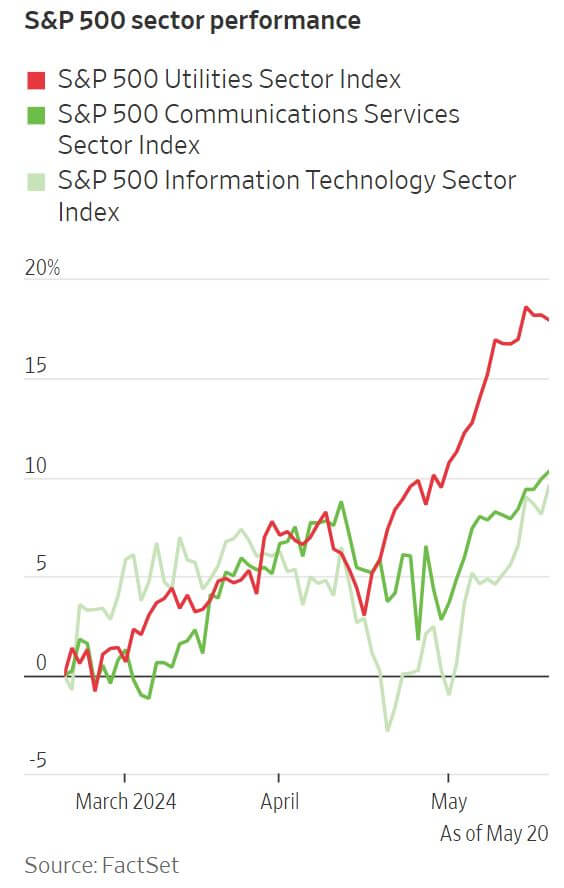

Utilities have emerged as a surprising leader in the stock market this spring, outperforming even in a year filled with unexpected developments on Wall Street. This rise is partly a recovery from a difficult 2023 and partly due to increased confidence that the U.S. economy can withstand higher interest rates and capitalize on the artificial intelligence (AI) boom. Recent economic data shows job growth slowing and inflation easing without a significant economic downturn, which would potentially pave the way to interest rate cuts and lower bond yields. This stability has shifted investor focus to power companies, which are expected to supply energy to the growing number of data centers driven by AI advancements. Over the past three months, the S&P 500 utility sector has surged 18%, surpassing the 11% gain of the information-technology sector. Notably, Texas-based Vistra has seen a 145% increase in its stock price this year, outshining even Nvidia's well-publicized 93% rise. While utility stocks are not anticipated to reach the high price/earnings multiples of tech giants, there is a strong belief that the sector will benefit from the expected surge in U.S. electricity demand driven by AI-related data centers. Citi analysts project that data centers could account for 10.9% of U.S. electricity demand by 2030, up from the current 4.5%. The rise in utility stocks marks a significant shift from the previous year when the Federal Reserve's interest rate hikes made higher yielding bonds more attractive, drawing investors away from utilities. Despite continuing low returns on utility dividends compared to government debt, projections of increasing electricity demand have drawn investors back to the sector. This shift has turned traditionally defensive utility stocks into a surprising growth bet. The rally started with independent power producers and has spread to regulated utilities. However, analysts caution that companies with less exposure to data centers or those manufacturing grid equipment might not perform as well. There is also concern that if the U.S. economy slows or AI enthusiasm wanes, utilities might face challenges before they can capitalize on the anticipated growth. If power demand growth falls short, consumers could face higher costs, and regulators might limit utility returns, affecting the sector's investment appeal. Overall, while utilities present a promising growth opportunity linked to the AI-driven increase in electricity demand, potential regulatory and economic risks remain significant considerations for investors.