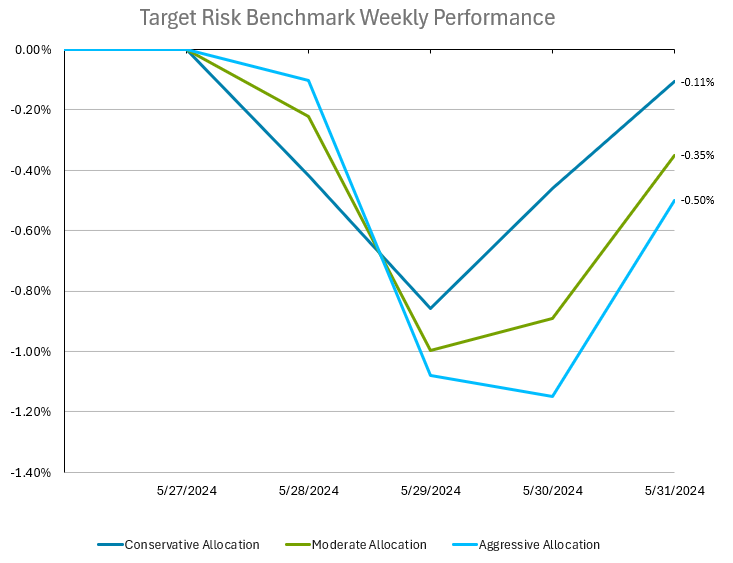

Investors in balanced multi-asset portfolios had losses for the second week in a row, though a rally to end the week on Friday reduced those declines by a significant amount. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. The first two trading days of the week saw significant declines in the Bloomberg US Aggregate Bond Index. Those losses were compounded by declines in both US and international stocks on Wednesday. The stock market experienced a downturn due to a sell-off in major technology companies, including Nvidia and Microsoft, ending a five-week winning streak. Disappointing quarterly earnings results from companies like Dell and Salesforce contributed to the decline. Bank of America strategists warned that investors heavily reliant on tech stocks might face challenges as other sectors gain traction. Value stocks could outperform growth stocks, potentially causing pain for those concentrated in tech. The top six stocks now make up a larger share of the S&P 500 than ever before. However, macroeconomic data came in soft on Thursday and Friday, suggesting a potential easing in inflation, which led both stocks and bonds to recover much of their losses from earlier in the week. The conservative risk tolerance benchmark ended the week with a small loss of -0.11%, while the moderate and aggressive allocations ended with larger losses of -0.35% and -0.5%, respectively.

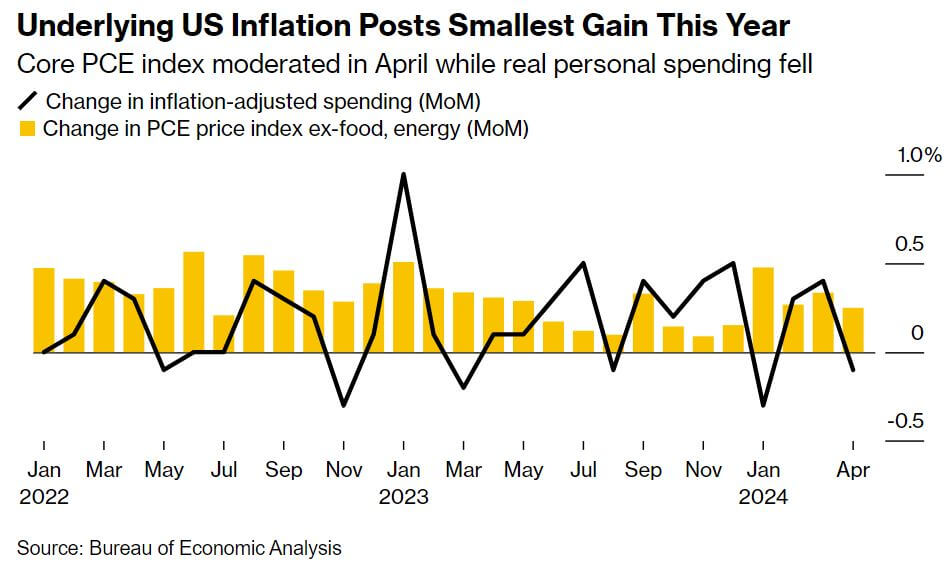

In April, the Federal Reserve's preferred measure of underlying U.S. inflation, the core personal consumption expenditures (PCE) price index, increased by just 0.2% from the previous month, marking the smallest monthly advance this year according to data from the Bureau of Economic Analysis (BEA). This measure, which excludes volatile food and energy prices, indicates a potential easing of inflationary pressures, providing some reassurance to Fed officials regarding the inflation trajectory after a period of disrupted progress in the first quarter. Concurrently consumer spending saw an unexpected decline of 0.1%, influenced by reduced spending on goods and a softer increase in services spending. Despite healthy demand for workers, wage growth has decelerated, with overall incomes rising by 0.3% and wages and salaries advancing by 0.2%, the smallest increase in five months. The decline in spending, combined with moderated wage growth, suggests a cooling in household demand despite steady job and income growth. The modest rise in services outlays of 0.1% was the smallest since August, with a 0.4% decrease in goods spending, primarily due to lower expenditures on gasoline and vehicles. Although healthcare spending supported services outlays, other areas like dining out, recreation, and transportation experienced declines. Financial markets responded to this data with lower Treasury yields, a rise in S&P 500 index futures, and a decline in the dollar index. Traders in swaps markets continue to anticipate at least one interest rate cut by the Fed this year, reflecting expectations of a more accommodative monetary policy in light of the recent data.

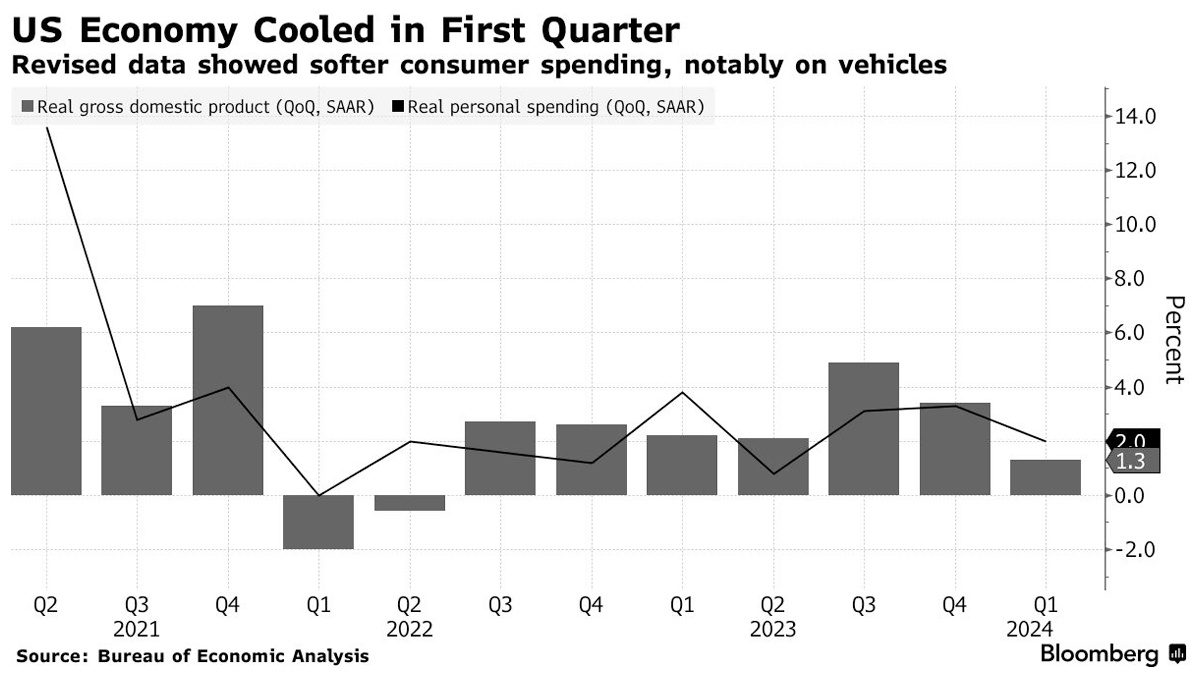

In the first quarter of 2024, the U.S. economy expanded at a revised annualized rate of 1.3%, down from an initial estimate of 1.6%, according to the Bureau of Economic Analysis in a separate report. This slowdown is primarily due to weaker consumer spending, especially on goods such as automobiles, reflecting high interest rates, reduced pandemic-era savings, and slower income growth. Personal spending, a crucial driver of economic growth, increased by 2.0%, lower than the previously reported 2.5%. Despite the reduced consumer spending, other economic indicators provided mixed signals. Federal government spending decelerated, and net exports detracted from growth for the first time in two years. Conversely, business and residential investments showed stronger-than-expected growth, with nonresidential investment rising by 3.3% and residential investment surging by 15.4%. A critical measure of domestic demand, final sales to private domestic purchasers, increased by 2.8%, down from an initial estimate of 3.1%. This metric's resilience suggests underlying demand remains robust, even as the headline GDP figures indicate a mild slowdown. Additionally, the BEA's report on gross domestic income (GDI), which complements GDP by measuring income generated and costs incurred in production, indicated a 1.5% increase in the first quarter. Corporate profits, however, showed a decline, with pre-tax profits falling by 0.6% and after-tax profit margins remaining stable at 15.2%. Economists, including Nationwide Financial Markets Economist Oren Klachkin, anticipate continued GDP growth throughout 2024, albeit at a moderated pace. Klachkin noted that while there are cautionary signs in the economic outlook, they do not warrant significant pessimism.