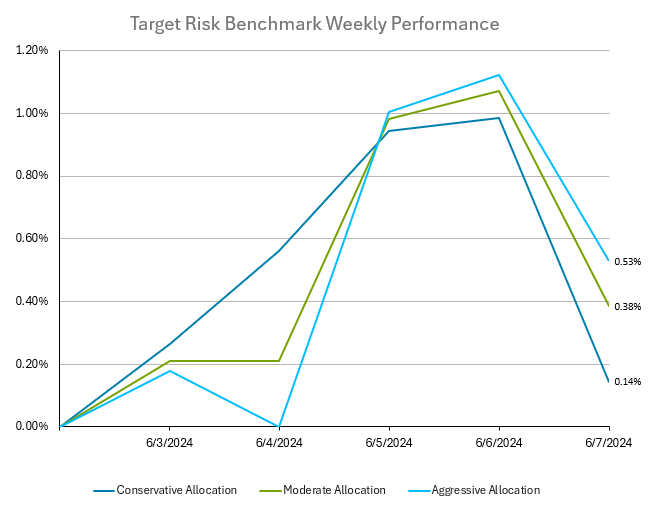

Investors in balanced multi-asset portfolios experienced dramatic reversals last week, with macroeconomic data driving shifts in risk sentiment. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. US mega cap technology stocks led the charge higher for US equities in the middle of the week. Bond yields dropped in the middle of the week as some US macro data came out softer than expected. International stocks also reacted positively when the European Central Bank delivered a rate cut as widely expected. This led to healthy gains in the target risk benchmarks across all risk tolerances and asset classes through Thursday. However, the jobs report on Friday came in hotter than expected, causing bond yields to jump sharply higher, reversing the decline in yields from earlier in the week. Short-term fixed income instruments saw a particularly large rise in yields. This led to a large loss on Friday in the conservative target risk benchmark relative to the more aggressive target risk benchmarks. The aggressive target risk benchmark held onto more of its gain from earlier in the week, finishing with a return of 0.53%. The moderate target risk benchmark ended the week with a gain of 0.38%, while the return in the conservative target risk benchmark was a muted 0.14%.

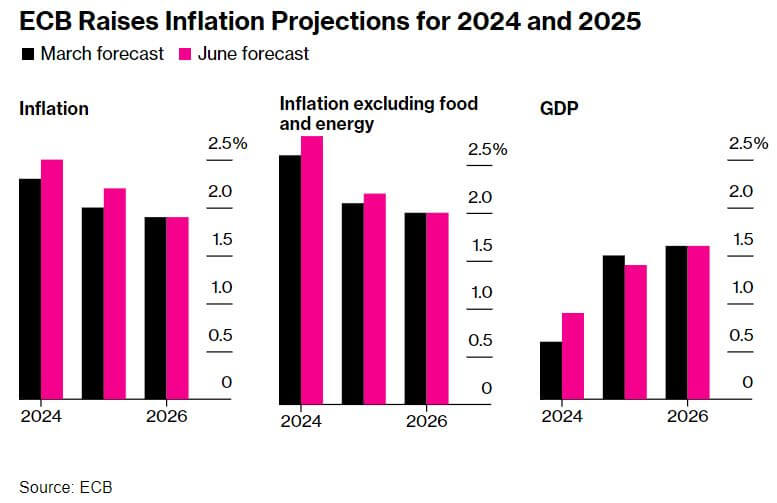

The European Central Bank (ECB) has decreased its key interest rate by a quarter point to 3.75%, marking its first rate cut in nearly five years and diverging from the U.S. Federal Reserve’s (Fed) policy trajectory. The ECB indicated future rate decisions would be data-driven, avoiding commitment to a fixed rate path. This cut is significant, signaling potential relief for households, businesses, and indebted governments, although it could complicate policymaking due to diverging paths between the ECB and the Fed. Recent data show persistent inflationary pressures in both Europe and the U.S., particularly in wages and services. Eurozone core inflation, excluding food and energy, increased to 2.9%, while U.S. core inflation decreased to 3.6%. Despite some economic improvement, ECB President Christine Lagarde acknowledged that inflation remains above the 2% target and is expected to do so well into the next year. Consequently, the ECB’s future rate cuts are probable but uncertain in timing and magnitude. The ECB’s decision, influenced by pre-communicated expectations and higher-than-anticipated economic growth and inflation, underscores a delicate balancing act. Analysts argue that the ECB’s communication strategy has inadvertently constrained its flexibility. A continued ECB rate reduction amid a static Fed rate could weaken the euro against the dollar, increasing import costs and potentially elevating eurozone inflation, thereby delaying further rate cuts in Europe. U.S. economic resilience contrasts with Europe’s stagnation. Despite significant rate increases, U.S. economic growth has been robust, reflected in strong job creation and stable wage growth. In contrast, Europe has faced economic stagnation since late 2022, though with some improvement noted in early 2024, particularly in southern regions benefiting from tourism. Investors are attuned to the policy divergence among major central banks, with market expectations suggesting limited divergence.

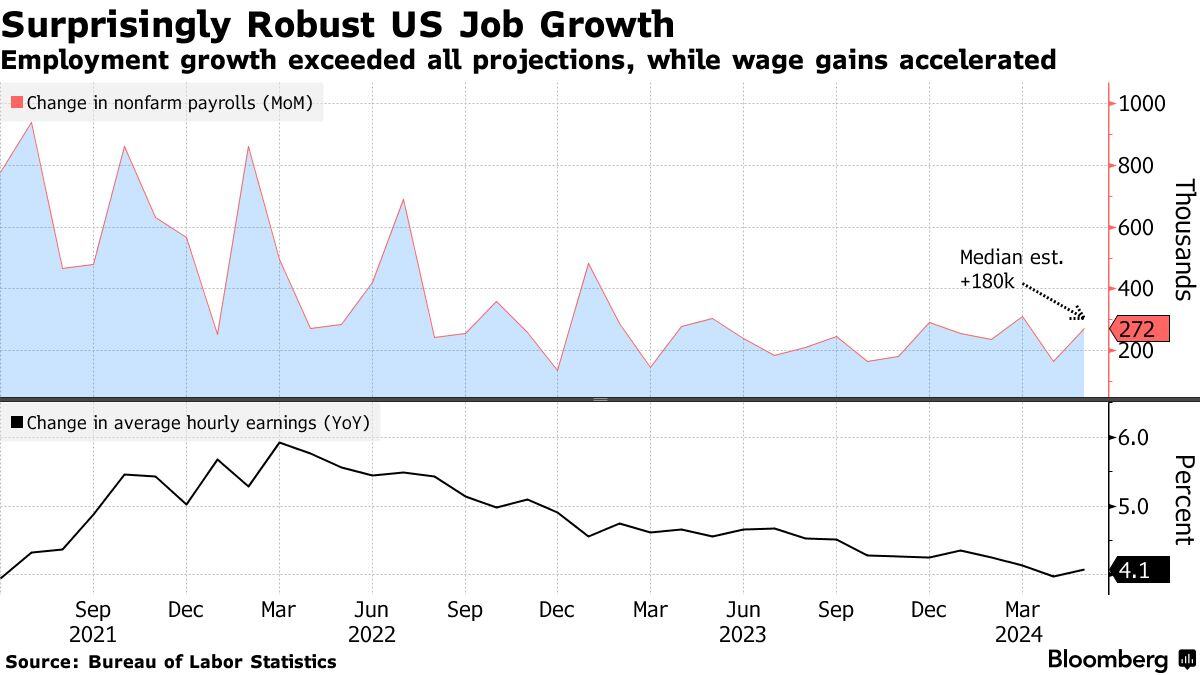

The U.S. labor market displayed unexpected strength in May, with nonfarm payrolls rising by 272,000, surpassing economists' predictions of 190,000. This notable increase, accompanied by a 4.1% year-over-year rise in average hourly earnings, overshadowed the slight uptick in the unemployment rate, which climbed to 4% from April's 3.9%, marking its highest point in over two years. The labor market's resilience contrasts with recent economic data suggesting a cooling trend, including weaker-than-expected figures for retail sales, consumer spending, construction, and industrial production. Additionally, there has been a modest rise in unemployment claims and a faster-than-anticipated decline in job openings, indicating an easing demand for labor. Despite these signs of a slowing economy, the labor market's unexpected vigor in May complicates the narrative of a steadily cooling economic landscape. This shift in sentiment could be seen in the market’s reaction, with bond yields rising and interest-rate futures indicating a greater probability of the Federal Reserve maintaining current rates past September. Fed officials, as reflected in the minutes from their April 30-May 1 meeting, have emphasized the need to keep rates steady for longer to ensure inflation continues its downward trajectory. With the Fed's next meeting approaching, it is widely expected that rates will remain unchanged, as officials reassess their projections and strategies to sustain economic stability and control inflation.