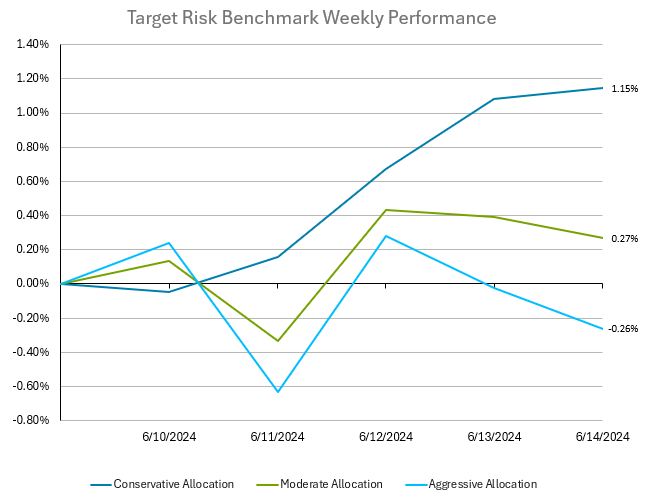

Investors in multi-asset class balanced portfolios experienced sharp divergence last week in returns depending on risk tolerance, as shown by the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. US bonds performed very well last week, with May inflation coming in cooler than expected, though the Fed declined to cut interest rates for now. The Bloomberg US Aggregate Bond Index returned 1.35% for the week, and the yield on the US 10 Year Treasury Note fell from 4.4% down to 4.22%. While US equities also posted a strong week following positive steps on the inflation front, international equities had a much more challenging period. The call for a snap election in France worsened investor sentiment for Europe, leading to significant losses. The MSCI ACWI ex UMA IMI Index fell 2.8% for the week, which overshadowed the positive performance of US assets in more aggressive balanced portfolios. The improving interest rate environment and flight to safety boosted the weekly return for the conservative target risk benchmark to 1.35%. More aggressive portfolios performed worse in contrast, due to their international equity exposure. The moderate target risk benchmark had a limited gain of 0.27% for the week, while the aggressive target risk benchmark fell -0.26%.

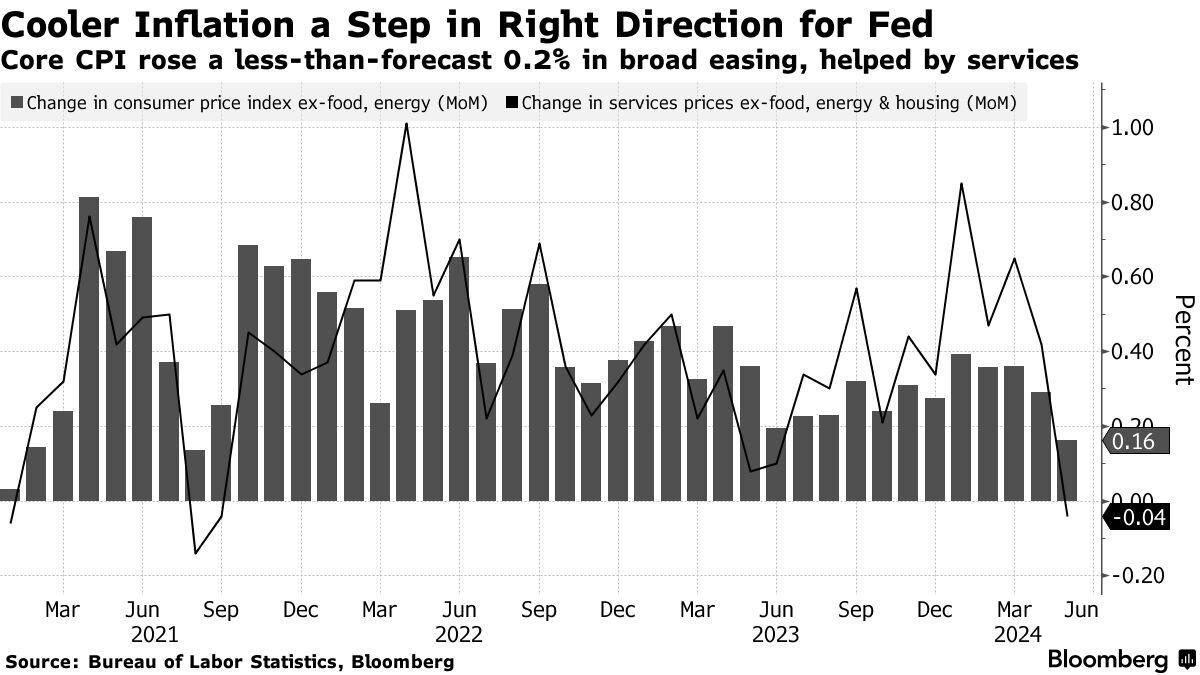

Federal Reserve officials have decided on a more conservative approach to interest-rate cuts this year, projecting only one reduction instead of the three previously forecasted in March. The federal funds rate remains at 5.25% to 5.5%, the highest level in two decades, first reached last July. The Fed’s updated projections now includes four rate cuts in 2025, up from the previously expected three. Despite the Federal Open Market Committee's (FOMC) unanimous vote to maintain the current rate, the individual perspectives on future cuts vary. The Fed’s dot plot revealed that four officials foresee no cuts this year, seven predict one, and eight expect two reductions. Market traders, influenced by earlier softer consumer price data, continued to expect two rate cuts this year, with the first anticipated in November. Economic indicators released before the FOMC meeting showed signs of aligning with the Fed's inflation goals. The core Consumer Price Index (“CPI”), which excludes volatile food and energy prices, increased by 0.2% in May and 3.4% annually, marking the slowest rise since 2021. The Fed also updated its inflation forecast, slightly raising it to 2.8% from the previous 2.60%, while keeping growth and unemployment rate forecasts steady at 2.1% and 4.0%, respectively. Despite a rise in the unemployment rate to 4.0% in May, some Fed officials believe that higher borrowing costs may not be sufficiently slowing the economy. This is evident in robust job market data, with nonfarm payrolls increasing by 272,000 in May, exceeding expectations. The Fed also confirmed it would continue reducing its balance sheet at a reduced pace, allowing its Treasury holdings to decline by up to $25 billion per month, while the cap for mortgage-backed securities remains unchanged at $35 billion.

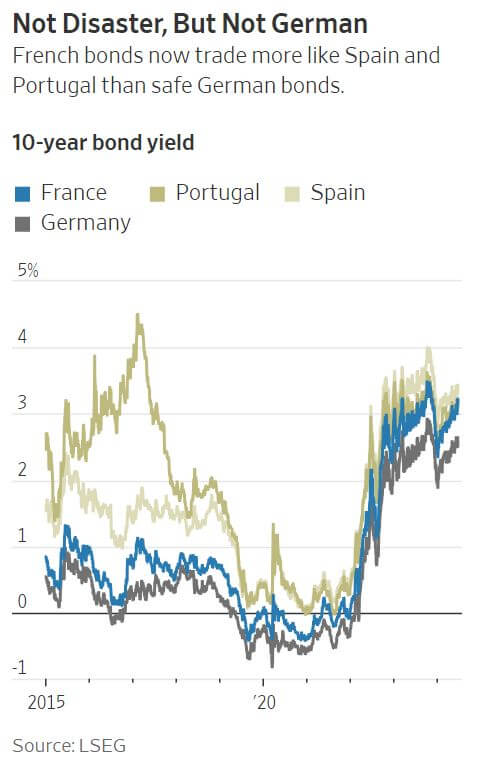

France is facing increasing economic challenges, drawing comparisons to the troubled eurozone countries of the past. Unlike Greece, which faced immense pressure to control its finances during the 2010-2012 euro crisis, France has largely avoided such scrutiny, resulting in substantial budget deficits and mounting debt. Though not as severe as the past eurozone crisis, President Macron's surprise call for snap elections last week has unsettled markets. Investors have begun to treat France similarly to Spain and Portugal, rather than as a stable economy. Last week, France experienced a minor financial tremor reminiscent of the euro crisis, with bond yields rising, the euro dropping, and bank stocks falling. France's deteriorating fiscal situation was highlighted by a recent downgrade from S&P Global and impending criticism from the European Commission for its failure to curb borrowing. If populists win the election, further increasing borrowing, investor confidence could plummet. Meanwhile, countries like Greece, Portugal, Ireland, and Spain, once at the eurozone's economic periphery, have made significant fiscal reforms and now exhibit healthier economies with government surpluses and current-account surpluses. France risks needing a shock to instigate necessary reforms. Macron's disregard for European deficit rules, with plans to spend significantly more than the government earns, exemplifies the issue. The far-right National Rally party, led by Marine Le Pen and Jordan Bardella, proposes even higher spending and less compliance with European fiscal oversight. French voters should heed the example of the U.K. from just a few years ago, where ill-conceived financial policies led to market turmoil and economic repercussions. France's extensive banking system is vulnerable to similar feedback loops between rising bond yields and financial instability, and may result in the country learning the same unfortunate lesson as the U.K.