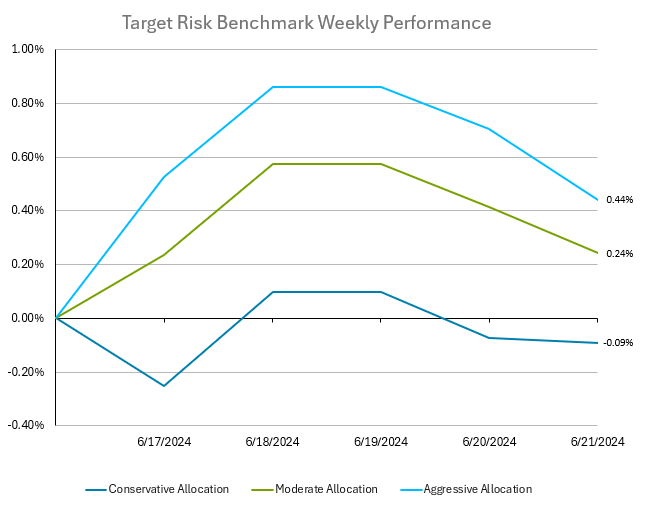

Positive equity returns, primarily in the U.S., helped aggressive and moderate multi-asset class balanced portfolios outperform this past week, as shown by the target risk benchmarks below. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. US bonds were marginally down last week, as slowing retail sales and housing activity were offset by strong business sentiment and industrial production. The Bloomberg US Aggregate Bond Index returned -0.16% for the week, and the yield on the US 10 Year Treasury Note was slightly higher, ending the week at 4.26%. US equities started the week on a strong note, fueled by optimism over artificial intelligence spending, but then faded through the end of the week as an estimated $5.5 trillion in equity options expired on Friday, leaving stock traders more cautious. The Russell 3000 Index rose 0.66% for the week. International markets continue to lag the U.S. due to continued strengthening in the U.S. dollar as well as the fallout from the prior week’s elections, particularly in France where borrowing costs have risen following the strong electoral gains made by populist parties. The MSCI ACWI ex UMA IMI Index rose 0.30% for the week, underperforming the U.S. market. The flat interest rate movement and underperformance of corporate credit contributed to a moderate down week for the gained 0.24% for the week, while the aggressive target risk benchmark rose 0.44%, both helped by the greater weight in equities.

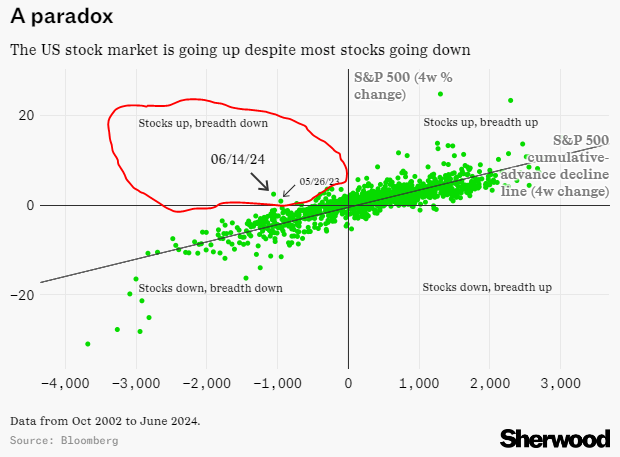

The US stock market has experienced a unique situation where the overall market is rising despite a significant number of individual stocks declining. Notably, there has been a stark divergence between the performance of market-cap weighted and equal-weighted versions of the S&P 500. Over the past month, the S&P 500 rose 2.4% while the cumulative advance-decline (A/D) line (the running total of the number of stocks rising versus falling each day) fell by over 1000, a rare occurrence based on data since 2002. Historical data offers little guidance on navigating such a market scenario.

Nvidia's performance, driven by the AI boom, is a major factor in this trend, reminiscent of similar market behavior in May 2023. Additionally, the Citi US economic surprise index has significantly dropped, indicating that economic data has fallen short of expectations. Despite these divergences, mega-cap stocks are still expected to show strong profit growth, and the US economy's GDP growth estimates remain stable at 2.4% for 2024.However, the heavy reliance on mega-cap stocks like Nvidia suggests increased market vulnerability should these stocks face a downturn if they are not able to meet lofty growth expectations. And if the broader market does not catch up with the run-up in mega-cap technology, there could be increased volatility should mega-cap stocks experience a correction. Diversification might become more crucial to mitigate risks associated with the concentration of market gains in a few large-cap stocks.

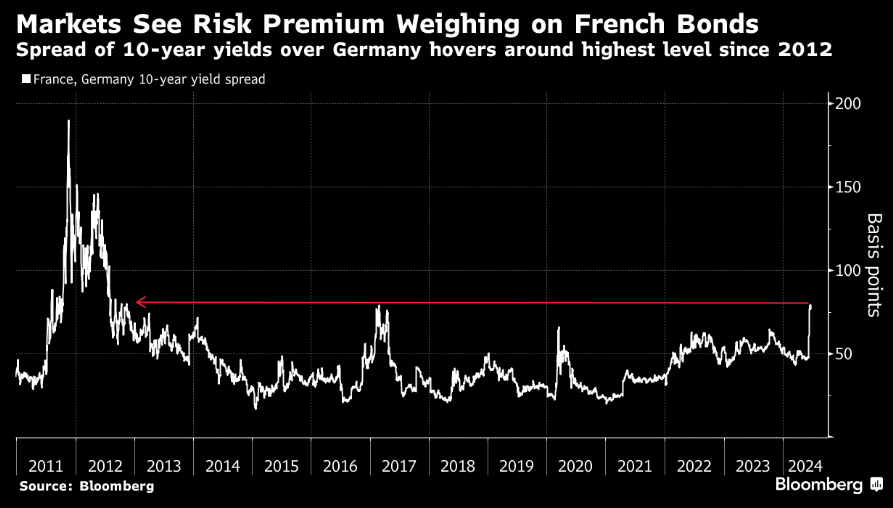

Investors are expected to impose higher interest rates on French government borrowing, which could have long-term consequences for France’s economy. Even if Le Pen's National Rally does not secure a majority in next month’s snap elections for the National Assembly, the market will likely continue demanding higher yields for French debt due to political uncertainty. This situation is expected to persist until the 2027 presidential election. This month, the yield on French 10-year bonds has risen by over 30 basis points, reaching levels last seen during the euro-area debt crisis. Bond investors hold concerns over Le Pen’s proposed budget measures and potential strains on France’s relations with the EU, which could challenge the euro-area's stability. Even if Macron’s party secures a parliamentary majority, a strong far-right presence could still obstruct legislative processes and hinder reforms, maintaining the risk premium on French bonds.

Higher bond yields demanded by investors will also pose further budgetary strains. The French finance ministry estimates that increased borrowing costs could add €800 million annually to the state’s expenses, potentially reaching €4-5 billion in five years and €9-10 billion in ten years. France’s finances are already strained, with the IMF projecting debt to rise to 112% of GDP by 2024, increasing by 1.5 percentage points annually. The EU has criticized France for exceeding the budget deficit limit, and S&P Global Ratings recently downgraded France's sovereign credit score.

While the current French-German spread is not alarming, it signifies increased risk perception. According to Fidelity International, a spread reaching 120 basis points would be concerning, but the market does not foresee an imminent sovereign crisis. France’s most recent bond sale raised €10.5 billion, indicating that current yields are attracting buyers, though this does not eliminate underlying concerns.