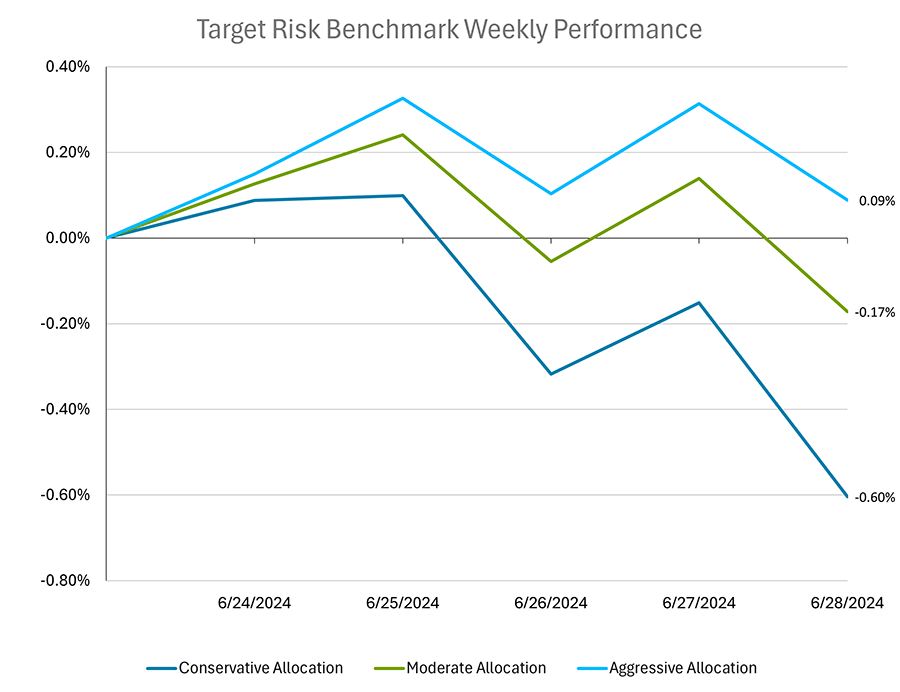

Investors in balanced multi-asset class portfolios experienced a week of choppy trading to close out what had otherwise been a strong month overall. The aggressive risk benchmark below has a roughly 90% allocation to global equities, with a small allocation to bonds. Meanwhile, the moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Bonds started the week with small gains but declined on Wednesday, followed by a small rally Thursday through Friday midday, before ultimately finishing the week down -0.71%, as measured by the Bloomberg US Aggregate Bond Index. US equities were choppy throughout the week, bouncing between gains and losses, before finishing essentially flat. International equities fared better with strong gains to start the week before giving some back, with the MSCI ACWI ex USA IMI Index finishing with a gain of 0.45%. Ultimately the tough stretch for bonds for the week weighed on the conservative target risk benchmark more heavily, which ended with a loss of -0.6% for the period. The moderate target risk benchmark held up better with a small loss of -0.17%, while the aggressive target risk benchmark benefitted most from the positive stretch for international equities, finishing with a gain for the week of 0.09%.

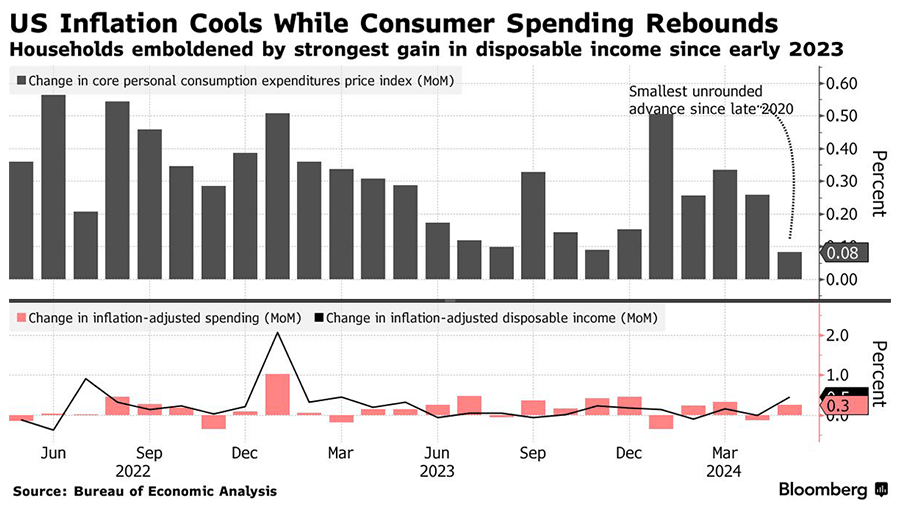

In May, the Federal Reserve's preferred measure of underlying US inflation, the core personal consumption expenditures (PCE) price index, rose by only 0.1% from the previous month, marking the smallest increase in six months and indicating the potential for lower interest rates later in the year. This measure, which excludes volatile food and energy prices, showed a mere 0.08% increase on a two-decimal basis, the smallest since late 2020. On an annual basis, core PCE rose 2.6%, in line with forecasts and lower than the prior month’s 2.8% increase. Simultaneously, household spending rebounded from a decline in April, supported by solid income growth. Inflation-adjusted consumer spending growth was particularly strong in goods, driven by increased incomes. This combination of slower price increases and robust spending provides some optimism for Fed officials, who had seen signs of economic slowdown earlier in the week. Bill Adams, chief economist at Comerica Bank, noted that the economy is showing positive signs with persistent growth, moderating inflation, and a more balanced job market. This kind of data supports the Fed's view that inflation may be returning to normal levels. Central bankers are closely monitoring services inflation excluding housing and energy, which tends to be more persistent. This metric rose by 0.1% in May, the smallest increase since October. Household demand has remained strong despite higher borrowing costs affecting some economic sectors. Inflation-adjusted outlays for services increased by 0.1%, driven by airfares and healthcare, while spending on goods rose by 0.6%, led by purchases of computer software and vehicles. Despite some labor market cooling, strong wage growth continues to fuel consumer spending, with wages and salaries rising by 0.7%. Real disposable income, adjusted for inflation, increased by 0.5%, the most significant rise since January 2023. However, Bloomberg economists expressed skepticism about the persistence of the disinflation process, citing the likelihood of core services categories maintaining inflation levels in the latter half of the year. The saving rate also rose to 3.9%, the highest since the beginning of the year, while separate data indicated a slight decline in consumer sentiment and moderated inflation expectations in June.

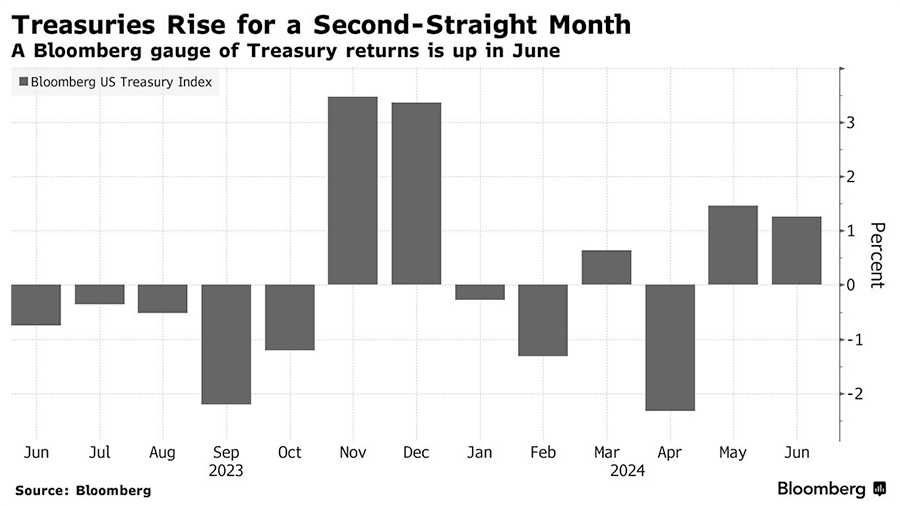

The US Treasury market saw a notable shift on the last trading day of June, with yields climbing as bond indexes rebalanced. Longer-maturity yields rose over 10 basis points, influenced by international inflation pressures and currency volatility. Gregory Faranello of AmeriVet Securities noted the volatility but indicated that yields aren’t being driven significantly lower despite weaker data. Ten-year yields, which initially dropped earlier in the day, surged by up to 12 basis points late in the session, fueled by high trading volumes during Bloomberg Indices' rebalancing. This process, impacting bond trading, involves adding and removing bonds, creating unpredictable market movements. Despite the day's selloff cutting short a major monthly bond rally, ten-year yields were down 12 basis points in June after a larger drop in May. This week’s developments paused a two-month Treasury rally supported by indications of easing inflation and labor market conditions. The PCE price index showed no change in May, suggesting inflation might be stabilizing. However, the 10-year yield remained above 4.2%, with Federal Reserve officials signaling caution before reducing interest rates. Richmond Fed President Thomas Barkin emphasized ongoing inflation concerns, and San Francisco Fed President Mary Daly pointed to effective monetary policy but cautioned against premature rate cuts. While bond investors initially anticipated six rate cuts for 2024, expectations have moderated to about 45 basis points, with a quarter-point cut likely by November. Looking ahead, traders will focus on June employment data and ongoing economic indicators to assess the Fed's policy trajectory, amidst uncertainty surrounding the US presidential election. Jason Williams from Citigroup remains neutral, awaiting further labor market data to justify yields below 4%.