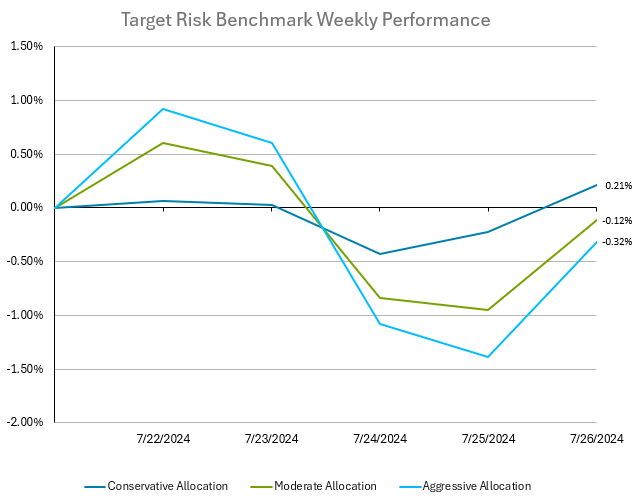

The stock market experienced a notable rise on Friday at the end of a tumultuous week, driven by economic data suggesting the Federal Reserve might initiate an interest-rate cut in September. This speculation fueled optimism across the S&P 500, which saw gains across all sectors, moving beyond its reliance on a few tech giants. Despite strong performances from big tech earlier in the year, concerns about concentration risk increased following a lackluster start to the earnings season for the mega-cap companies. This shift led investors to diversify into economically sensitive shares. Financials, industrials, and staples have outperformed tech in July, while small caps surged by 10%, benefiting from expectations of lower rates for their higher debt burdens. George Maris of Principal Asset Management noted this rotation’s potential lasting power, driven by forecasts for a broader earnings recovery in smaller companies. Quincy Krosby at LPL Financial highlighted the interest-rate sensitivity of small caps, but also the risks that an economic slowdown would pose for them. The upcoming earnings reports from major tech firms will be crucial in determining the market's direction amid mixed economic signals and a typically negative seasonal pattern. The recovery in markets on Friday benefited balanced multi-asset class investors, regardless of their risk tolerance. This can be seen in the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to global equities, with a small allocation to bonds. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Both cash equivalents and domestic bonds had positive returns for the week, which resulted in the conservative target risk benchmark having the best return for the week at 0.21%. The moderate and aggressive target risk benchmarks had significant losses through the middle of the week but recovered as equities bounced back. The moderate target risk benchmark finished with a loss of -0.12%, while the aggressive target risk benchmark cut its weekly loss to -0.32%.

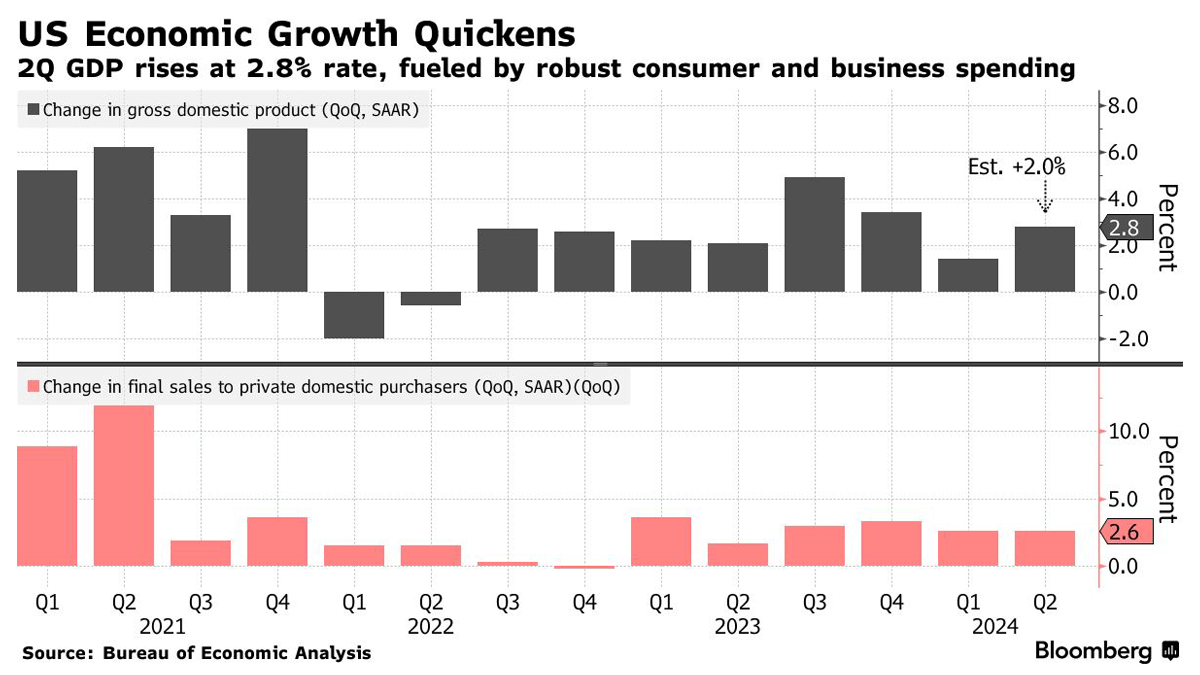

US economic growth rebounded in the second quarter of 2024, with GDP increasing at an annualized rate of 2.8%, surpassing forecasts and the previous quarter’s 1.4% rise. This growth was primarily driven by a 2.3% increase in personal spending, also exceeding projections. However, a key measure of underlying inflation rose 2.9%, slightly above estimates, although it did decelerate from the first quarter. Despite this acceleration, the economy showed signs of moderation from the previous year, as high interest rates curbed some underlying economic activity. Notably, consumer spending on durable goods like cars and furnishings rebounded, and government spending, particularly in defense, contributed more to GDP growth. Conversely, residential investment declined due to high mortgage rates. Business investment saw the fastest growth in almost a year, driven by significant advances in equipment orders. Factory orders for business equipment, excluding aircraft and defense, surged in June, recovering from a previous month’s decline. Additionally, inventories added to GDP for the first time since the third quarter of the previous year, offsetting a near-record trade deficit. Inflation-adjusted final sales to private domestic purchasers, which strips out government spending, trade, and inventories to provide a gauge of underlying demand, rose 2.6% for the second straight quarter. Looking ahead, economists predict a more pronounced economic slowdown in the latter half of the year as the labor market weakens and income growth decelerates, further impacting consumer spending. Recent corporate earnings reports suggest Americans are beginning to pull back on spending and facing increasing financial strain.

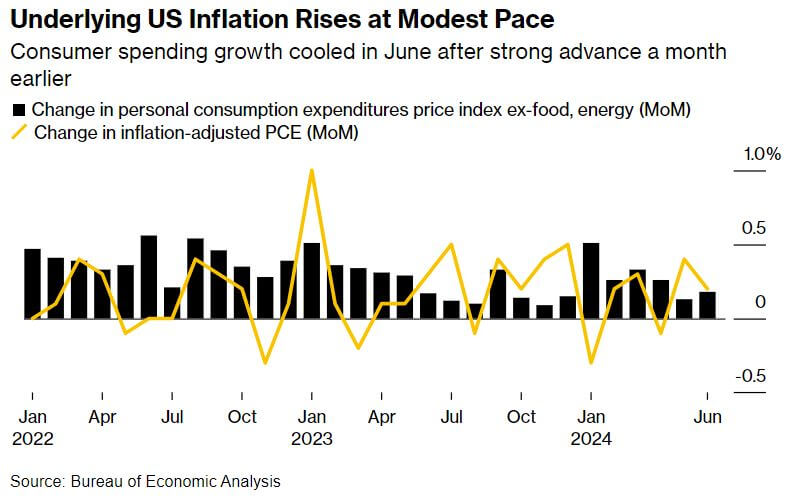

In June, the Fed's preferred inflation measure, the core Personal Consumption Expenditures (PCE) price index, increased by a modest 0.2% from May and 2.6% year-over-year, indicating underlying inflation rose at a manageable rate, and in line with forecasts. This measure excludes volatile food and energy prices, providing a clearer view of sustained inflation trends. Inflation-adjusted consumer spending also grew by 0.2%, while May's spending increase was revised higher, signaling robust consumer activity. Despite these positive signals, consumer sentiment, as measured by the University of Michigan, fell to an eight-month low in July, reflecting persistent concerns over high prices. Core inflation, on a three-month annualized basis, decelerated to 2.3%, suggesting the Fed's tightening measures are gradually influencing the economy without severe repercussions. Key factors included a 0.2% rise in services inflation, excluding housing and energy, and steady increases in inflation-adjusted outlays for services and goods, driven by housing, utilities, vehicles, and recreational items. However, wage growth slowed to 0.3% in June, half the previous month's rate, leading to a deceleration in disposable income growth to 0.1%. Bloomberg Economics analysts highlighted that consumer spending, though healthy, is slowing amid weaker income growth and a cooling labor market. The saving rate dropped to 3.4%, the lowest since December 2022, indicating diminished consumer capacity for future spending. Rising credit card delinquencies and upcoming employment data will further illuminate the economic outlook, particularly regarding income growth and consumer resilience. This data suggests that inflation and economic activity are cooling sufficiently to open the door for future interest rate cuts. The consensus among analysts is that the Fed will maintain its current interest rate at its upcoming meeting while setting the stage for potential rate cuts in September.