Market sentiment has shifted from expecting a soft landing to concerns that the Fed's high rates are overly cooling the labor market. Last week, the S&P 500 experienced its steepest two-day decline since March 2023, and the Nasdaq 100 entered a correction by falling 10% from its peak. The volatility surge was accompanied by a flight from riskier investments. Treasuries saw a seven-day rally as traders anticipated a full percentage point rate cut by the Fed in 2024. The Cboe NDX Volatility Index spiked to its highest level since March 2023, reflecting increased market volatility.

Investors are increasingly worried about a potential recession, although some analysts believe the economy is merely hitting a rough patch rather than heading for a downturn. The Nasdaq 100 Index has lost over $2 trillion in value in just over three weeks as traders withdrew from Big Tech investments. High spending on AI has contributed to the tech selloff. Alphabet’s capital expenses exceeded estimates by $1 billion, prompting investors to exit due to concerns over unrestrained spending and delayed revenue prospects. Microsoft and Amazon signaled similar heavy AI investments, further unsettling investors. Notable stocks like Nvidia and Tesla have fallen over 20%, entering bear-market territory, while Microsoft and Amazon have each declined more than 10%. Despite the broader tech downturn, some companies like Apple and Meta Platforms have shown resilience, with Apple rising following a positive earnings report and Meta also gaining earlier in the week.

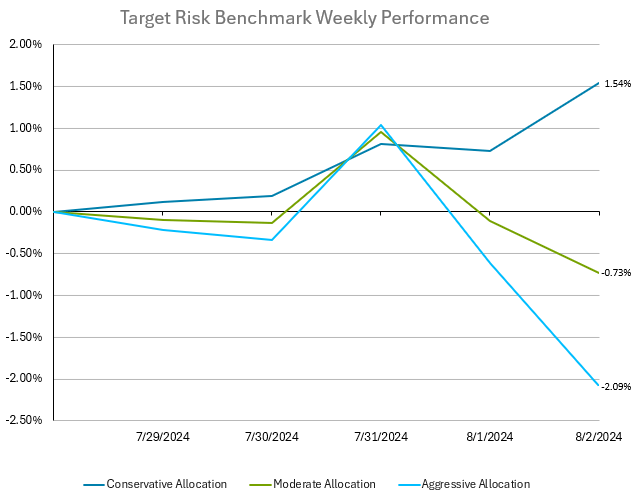

The sudden flight to safety led to a sharp divergence in returns for aggressive and conservative investors, as shown by the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to global equities, with a small allocation to bonds. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. The equity selloff resulted in a -2.09% loss for the aggressive target risk benchmark, while the fixed income rally limited losses in the moderate target risk benchmark to -0.73% for the week. The conservative target risk benchmark benefited from the large drop in bond yields, leading to a weekly gain of 1.54%.

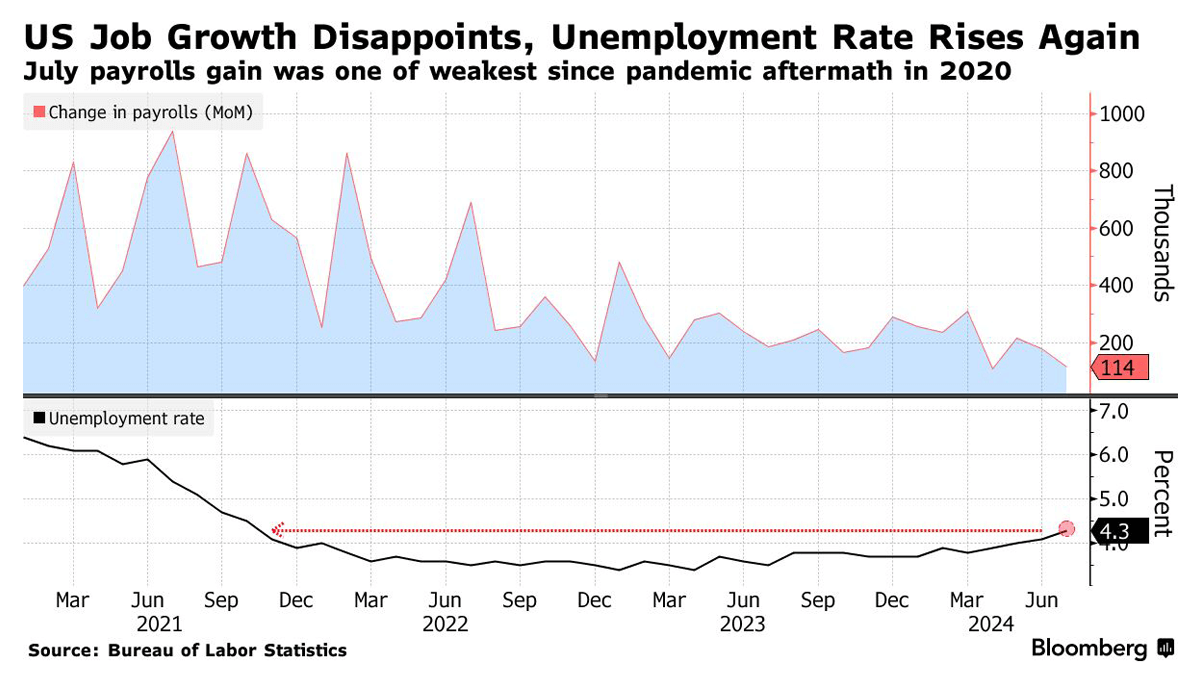

The Federal Open Market Committee (“FOMC”) unanimously decided to maintain rates in the 5.25% to 5.5% range last week, although Federal Reserve Chair Jerome Powell noted that some officials favored a rate cut during the two-day meeting. During the press conference following the FOMC meeting, Powell highlighted improved inflation data, a desire to prevent rising unemployment, and the belief that Fed policy is increasingly slowing economic activity. Powell stated that “the broad sense of the committee is that the economy is moving closer to the point at which it will be appropriate to reduce our policy rate.” The Fed’s policy statement reflected progress in combating inflation, describing it as “somewhat elevated,” a downgrade from previous descriptions. This change signals a shift toward balancing the Fed’s dual mandate of controlling inflation and maintaining a strong labor market. The Fed faces two risks: easing too soon, allowing inflation to remain above the 2% target, or delaying too long, causing economic strain from high rates. The economy has shown resilience, with GDP growth at 2.1% in the first half of the year and recent inflation data indicating a slowdown in price growth. However, new data released after the FOMC meeting showed that the US labor market exhibited significant weakening in July, with nonfarm payrolls increasing by just 114,000, a figure lower than nearly all predictions and one of the weakest since the pandemic's onset. The unemployment rate rose to 4.3%, the highest in almost three years. This unexpected uptick in unemployment, alongside lower-than-forecast average hourly earnings, suggests a faster-than-anticipated labor market deterioration. The disappointing jobs report contributed to a broader week of underwhelming economic data, spurring a stock market sell-off and reducing Treasury yields. Economists, including those from Bloomberg and LH Meyer/Monetary Policy Analytics, highlight that the labor market is cooling more rapidly than desired, potentially necessitating more aggressive rate cuts.

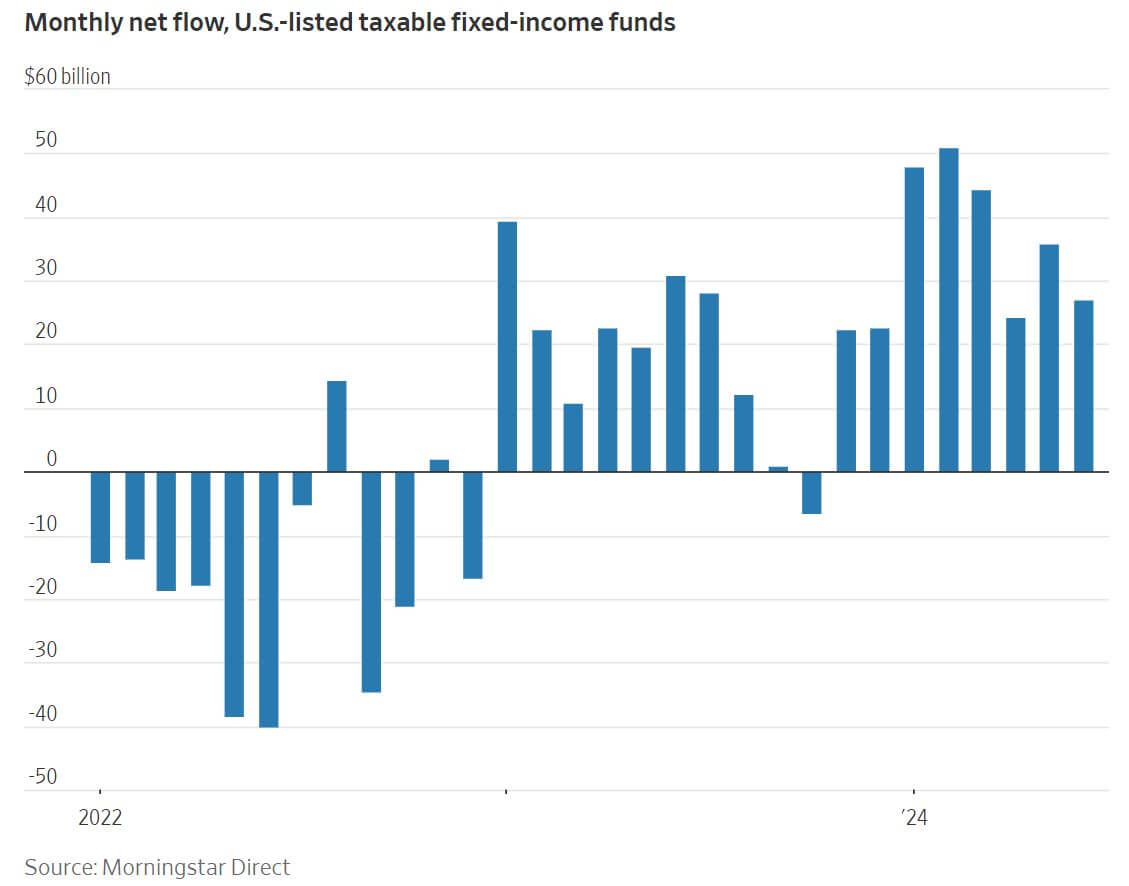

Wall Street has seen an unprecedented surge in bond fund investments this year, driven by the highest bond yields in a generation and an impending drop in interest rates. This has resulted in substantial inflows into both indexed and actively managed bond funds as investors seek to mitigate risk, especially retirees. U.S.-listed fixed-income ETFs alone have garnered nearly $150 billion by late July, marking a record influx. The environment of high rates and falling inflation presents a rare opportunity for substantial investment income, attracting significant interest in bond funds. Expectations of Fed rate cuts have shifted investor focus from cash-like investments to bonds, seizing the moment before yields decline further with rising bond prices. This trend is particularly benefiting actively managed bond funds. According to Morningstar, 74% of such funds have outperformed their benchmarks over the past year. Investors are diversifying their bond fund choices, ranging from Treasury ETFs for interest-rate bets to actively managed funds in high-yield corporate debt and collateralized loan obligations. The renewed interest in bonds marks a stark contrast to 2022, when rising rates caused significant losses in bond funds and the classic 60/40 stock-bond portfolio suffered its worst performance since the Great Depression. However, with anticipated rate cuts and the bond market’s resurgence, Wall Street analysts advocate for renewed bond investments to capitalize on current yields before they potentially decline. This broad-based enthusiasm for bond funds is attributed to a combination of stock market gains prompting risk balancing and the strategic anticipation of rate cuts enhancing bond valuations.