The stock market experienced its biggest back-to-back gains in 2024 after a volatile week marked by significant fluctuations. Early in the week, panic selling led to sharp declines, but by the end of the week, the S&P 500 nearly recovered its losses. Market turbulence was driven by concerns over the Federal Reserve’s response to weak economic data and uncertainty around Japan’s economic policy. The yen carry trade also caused instability across various asset classes. Meanwhile, the VIX, Wall Street’s fear gauge, subsided after a spike on Monday.

Global bond markets experienced a volatile week as well. Early in the week, concerns over the U.S. economy led to a huge rally in U.S. Treasuries. However, as the week progressed, the market regained composure, with the yield on the 10-year U.S. Treasury note returning to around 4%, erasing most of the earlier declines. Traders reduced expectations for aggressive Fed rate cuts. Trading volumes in Treasuries hit record highs, signaling the market’s nervousness. The market remains on edge as investors attempt to predict the timing and scale of potential Fed rate cuts, with upcoming inflation data expected to be a critical factor. However, the overall sentiment remains cautiously optimistic, with expectations that the bull market could persist if economic fundamentals stay solid.

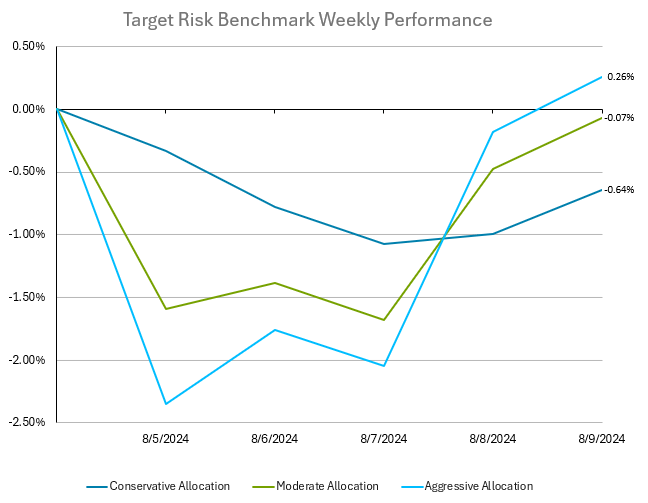

Investors in multi-asset portfolios trimmed losses by a significant margin to end the week, as seen in the target risk benchmarks below. The aggressive risk benchmark has a roughly 90% allocation to global equities, with a small allocation to bonds. The moderate risk benchmark is a 60/40 split of global equities and bonds, while the conservative risk benchmark has a roughly 90% allocation to US bonds. Counterintuitively, the aggressive target risk benchmark fared better for the week than the conservative risk benchmark as equities recovered while bonds gave back much of the aggressive rally seen earlier. The aggressive target risk benchmark finished the week with a gain of 0.26%, while the moderate benchmark lost -0.07%. The conservative target risk benchmark in contrast ended the week with a loss of -0.64%.

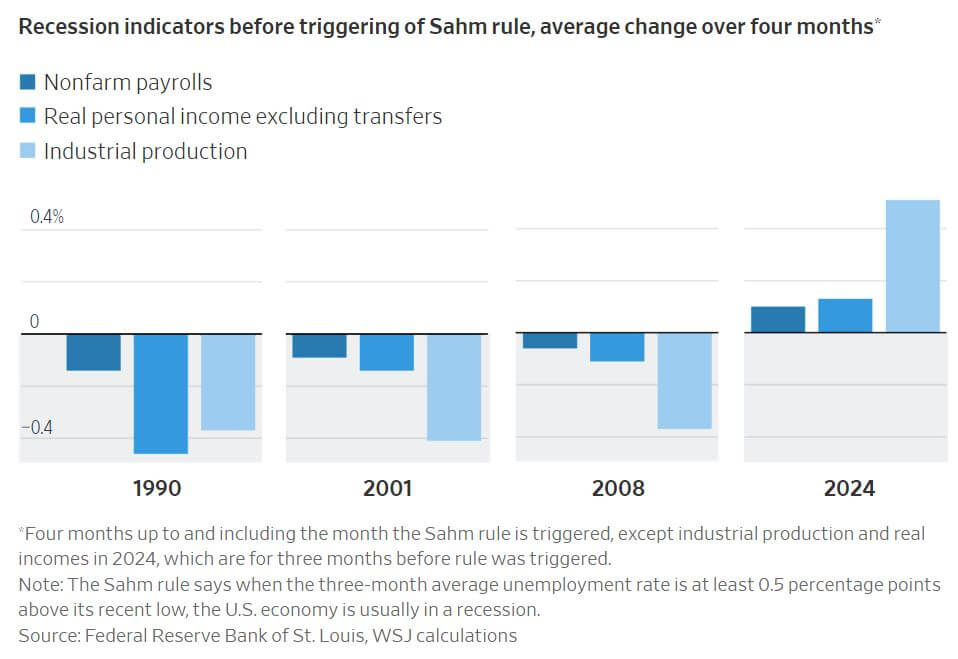

The unemployment rate is rising, stock markets are declining, and bond yields are falling below short-term interest rates, which are often indicative of a potential recession. However, a deeper analysis suggests that the U.S. is not currently in a recession, highlighting the importance of timely intervention from the Fed to prevent a downturn. Two significant events have fueled recession concerns: a stock market selloff triggered by the Bank of Japan's decision to tighten monetary policy, and a rise in the U.S. unemployment rate to 4.3% in July from 4.1% in June. The increase in unemployment aligns with a rule of thumb by economist Claudia Sahm, which historically correlates with recessions but is not a definitive indicator. More accurate measures, such as payroll employment, industrial production, and real incomes, show growth, suggesting the U.S. has not yet entered a recession. While stock market declines precede most recessions, not all stock slumps lead to recessions. Falling stock prices can directly impact spending and employment, potentially triggering a negative feedback loop. The Fed can mitigate this by cutting interest rates to boost demand and investment, though it remains cautious due to inflation concerns.

While it's uncertain whether the recent market turmoil is due to a rising yen or actual economic weakening, there are reasons to believe any potential recession may not be severe. Three factors determine a recession's severity: pre-existing economic conditions, the recession’s cause, and the policy response. Currently, the U.S. economy is robust. Despite being at high levels, the households and corporations are not overly leveraged, unlike in 2008, suggesting resilience even in a downturn. Households are spending a relatively low share of their disposable income on debt service and corporate debt stands at a low level relative to the market value of equity. Although there are long-term economic concerns, such as high government debt and political instability, these are not immediate threats. Recessions can be triggered by supply shocks, but none are expected soon. Current interest rates are not excessively high by historical standards. Historical precedents, such as the Fed's intervention in 1997 following stress in the foreign exchange market, show that timely actions can prevent financial crises. Future fiscal policies, whether under a Trump or Harris administration, are expected to be loose, potentially addressing recessionary pressures but risking inflation. While markets have anticipated a recession since 2022, there are strong indications that any upcoming recession could be relatively mild and short-lived.

Global stock markets have been volatile amid American recession fears, with Japan experiencing the most dramatic fluctuations. On August 5th, the Topix index plunged 12%, the worst since 1987, as the yen strengthened from a 37-year low. The following day, stocks rebounded by 9% as investors bought undervalued shares. Monetary policy changes are driving these market swings. Over 18 months, the yen weakened as the U.S. Federal Reserve raised interest rates while Japan's central bank did not, encouraging a "carry trade" where investors borrowed cheaply in yen for higher returns in dollars or euros. This weakened yen boosted Japanese firms' foreign earnings and attracted foreign investment, with ¥9 trillion ($60 billion) in stocks purchased in 2023 and early 2024. The situation shifted when the Bank of Japan raised its rate from 0.1% to 0.25% on July 31st, while the Fed was expected to cut rates soon. This expectation grew after a disappointing U.S. jobs report on August 2nd. Speculators heavily invested in short yen trades had to quickly reverse their positions, driving up the yen and causing a stock market slump, particularly for exporters. Leveraged margin bets on Japanese stocks, which were at their highest since 2006, were rapidly unwound. On August 6th, investors reentered the market, believing the sell-off was driven by debt-laden forced selling. Stocks like Tokyo Electron and Japanese banks saw significant swings. Analysts do not foresee deep distress for Japanese firms or financial instability. However, Japan's role as a major global creditor means its market changes can impact foreign markets, especially if Japanese investors need to sell foreign assets to cover domestic liabilities. The extent of Tokyo's market turmoil remains uncertain, but choppy conditions are expected as speculative bets unwind. JPMorgan Chase reports that three-quarters of the global carry trade has already been unwound following the recent market selloff. This downturn has wiped out gains made year to date for the trading strategy. Returns on carry trade baskets, including those in the Group-of-10 and emerging markets, have declined by about 10% since May, significantly reducing profits accumulated since late 2022.