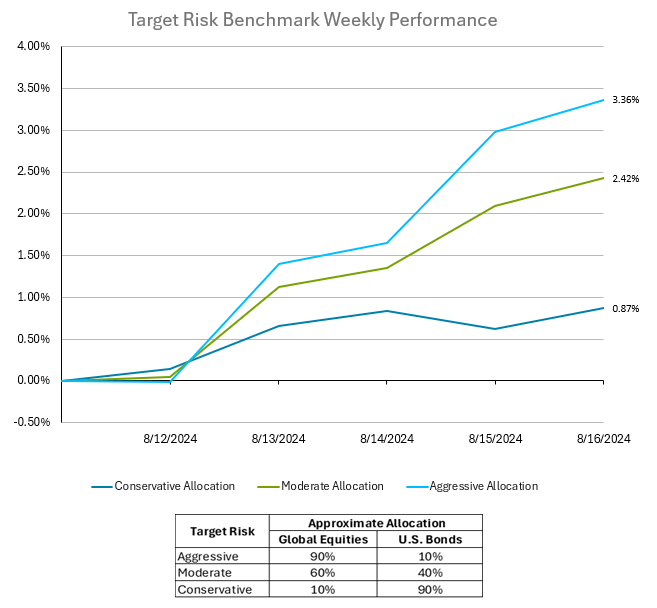

This past week saw strong equity returns, primarily within U.S. large caps, which helped aggressive and moderate multi-asset class balanced portfolios outperform, as shown by the target risk benchmarks below. U.S. bonds also generated positive returns last week, on the heels of benign inflation reports confirming the continued slowdown from post-pandemic peak levels. The Bloomberg U.S. Aggregate Bond Index returned 0.57% for the week, as the yield on the U.S. 10 Year Treasury Note dropped slightly lower, ending the week at 3.88%. U.S. equities started the week on a strong note, as global markets move past the prior week’s volatile session sparked by the Bank of Japan’s decision to raise its benchmark rate and the subsequent unwinding of the yen-carry trade. U.S. technology stocks continued their advance over optimism in artificial intelligence spending, as well as further evidence that U.S. economic growth remains on firmer footing with this past week’s advanced retail sales release. The Russell 3000 Index rose 3.80% for the week. International markets continue to lag the U.S. despite U.S. dollar weakness, as further evidence of Chinese economic slowing weighed on emerging market sentiment. The MSCI ACWI ex UMA IMI Index rose 3.67% for the week, slightly underperforming the U.S. market. The moderate portfolio gained 2.42% for the week, while the aggressive target risk benchmark rose 3.36%, both helped by the greater weight in equities. The conservative portfolio returned 0.87% for the week.

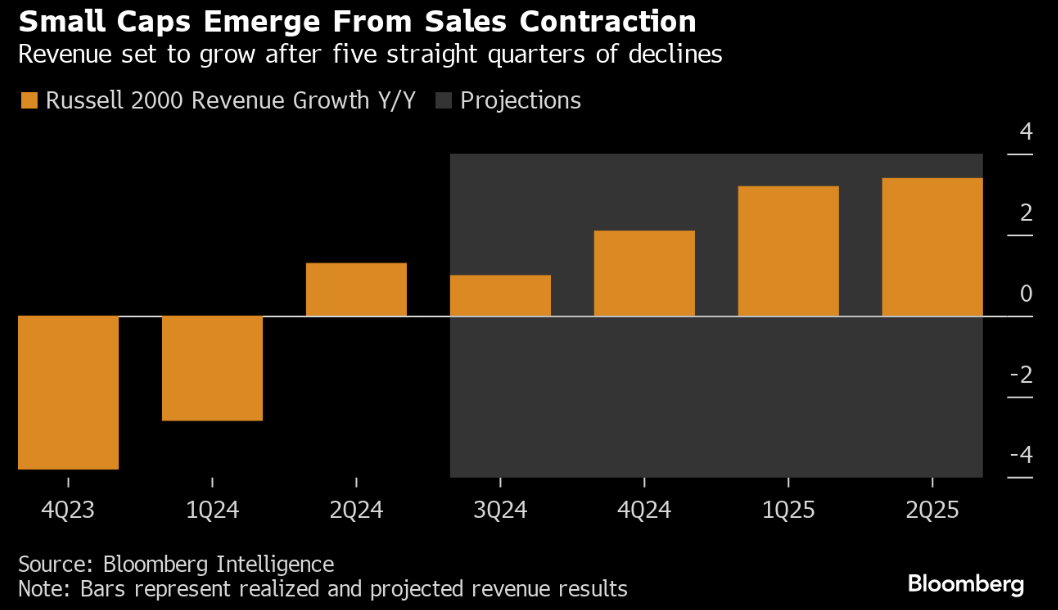

The Russell 2000, a benchmark for small-cap stocks, has bounced back, posting a 3% gain this past week after early month losses. Improved earnings and benign economic data are supporting this rally, indicating optimism about a "soft landing" for the economy as the Fed decides whether to cut its benchmark rate at the September FOMC. The current fundamental backdrop is also supportive for small caps as 2nd quarter sales growth for the Russell 2000 is expected to rise 1%, which now exceeds earlier expectations.

However, the future outlook for small-cap stocks has dimmed slightly, with revenue growth forecasts for the third quarter reduced to 1%. Broader concerns about a slowing U.S. economy could pose risks to these firms, although proactive monetary easing by the Fed would help alleviate higher borrowing costs. Despite these concerns, the Russell 2000 remains attractively valued compared to the S&P 500, which may entice investors looking for long-term recovery opportunities.

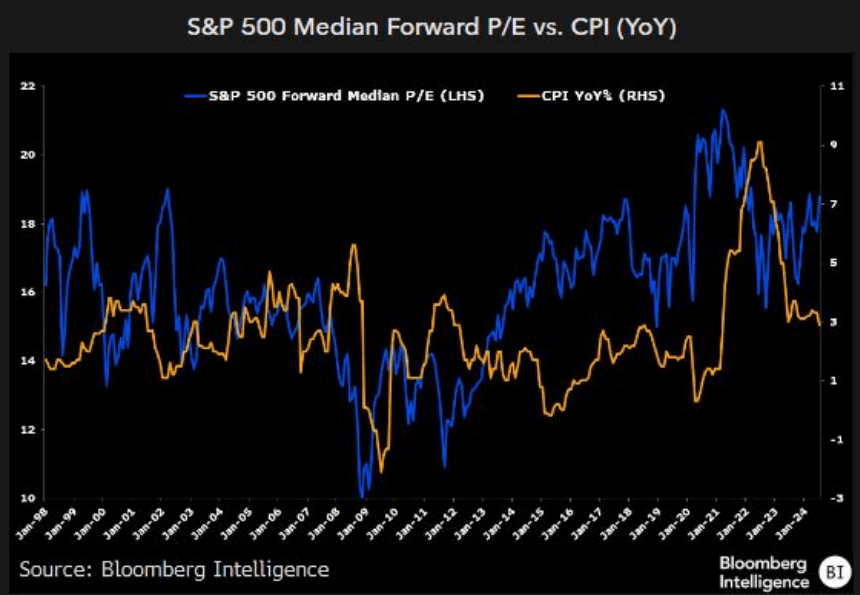

Inflation's declining influence on equity markets may be nearing an end, according to Gina Martin Adams, Bloomberg's Chief Equity Strategist.

While price/earnings (P/E) ratios for U.S. large-cap stocks have surged as inflation has slowed from post-pandemic peak levels, the impact of slowing inflation on these multiples is expected to be more subdued now that inflation is running below 3%. According to Bloomberg, historically, P/E ratios have only been moderately negatively correlated with inflation, and significant disruptions occur primarily during sharp inflation shifts, as seen in 2022 when rising CPI drove a drop in S&P 500 P/E ratios.

With inflation now stabilizing, the S&P 500 P/E forward median ratio has steadied around 18x, near the high end of its range going back to 2008, with limited upside potential as inflation continues to fall. Historically, the P/E has averaged 15.9x when CPI was at 2.5-3.0%. On average, stocks had the biggest gains during periods when inflation slowed towards 3% but saw those gains stall when inflation dropped below 3%.