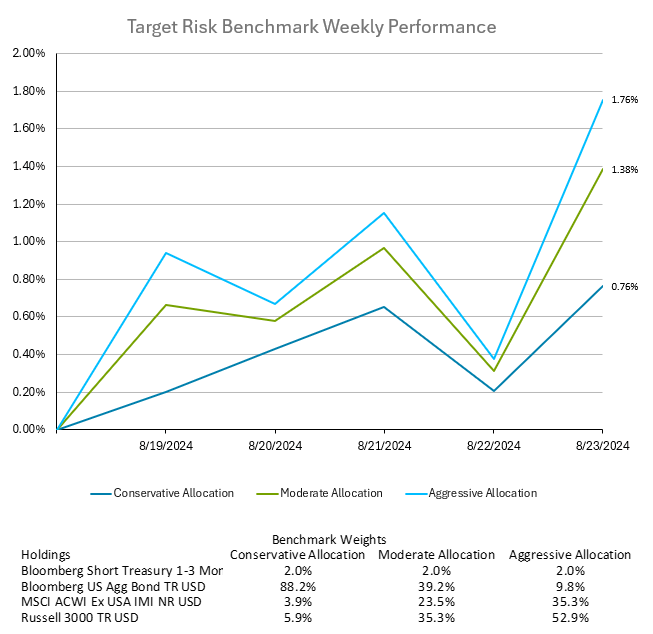

Stocks rallied and bond yields fell following Federal Reserve Chair Jerome Powell’s indication that rate cuts will begin in September. Powell’s comments at the Jackson Hole symposium led to a rally in U.S. Treasuries, with yields on two-year notes falling by up to 9 basis points to 3.91%. The 10-year yield settled at 3.806%, down from 3.862% Thursday. This movement supported market expectations of a significant easing cycle, with traders now pricing in 101 basis points of cuts by the end of the year, possibly including a 50-basis-point reduction. The rally in Treasuries, which began in May, was driven by cooling inflation and a weakening labor market, prompting bets on the Fed's policy shift. The market is now factoring in a total of 210 basis points of easing by September 2025. Despite the lack of specifics on the final destination for the federal funds rate, the market responded positively, with all major S&P 500 groups gaining. Global equities remained near all-time highs on Friday, while both the Magnificent Seven and small caps rallied in response to the news. Investors in multi-asset class portfolios across all risk tolerances enjoyed healthy gains for the week as a result, as seen in the target risk benchmarks below. Aggressive investors benefitted the most from the substantial positive weekly return in both domestic and international equities, with the aggressive target risk benchmark gaining 1.76%. The moderate target risk benchmark wasn’t far behind, with a return of 1.38%. Conservative investors also saw positive returns from the decrease in bond yields across the yield curve, ending the week up 0.76%.

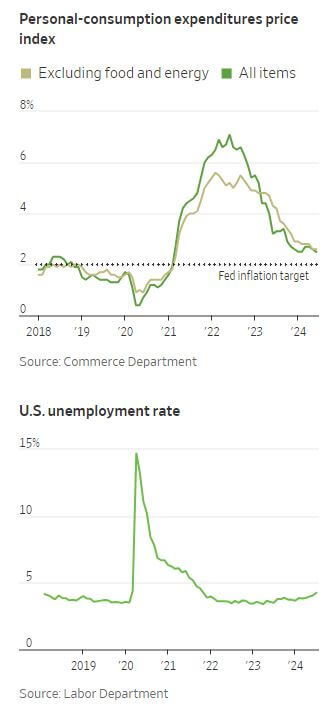

Federal Reserve Chair Jerome Powell has signaled a pivotal shift in monetary policy, stating that the time has come to cut the Fed's key policy rate, likely beginning in September. His remarks at the Kansas City Fed’s annual conference in Jackson Hole underscore the Fed's intention to prevent further deterioration in the labor market while continuing its progress toward the 2% inflation target. Powell acknowledged recent improvements in inflation, which has been moderating after a period of stagnation, and expressed increased confidence that inflation is on a sustainable path back to the Fed's target. The central bank’s preferred inflation gauge, the personal consumption expenditures price index, rose 2.5% in June from a year earlier. Despite this progress, cracks in the labor market, highlighted by a disappointing July jobs report, have raised concerns among Fed officials that high interest rates may now be posing a threat to economic strength. U.S. job growth over the year through March was likely significantly overestimated, with a forthcoming revision by the Bureau of Labor Statistics (BLS) expected to reduce the payroll count by 818,000 jobs. This equates to about 68,000 fewer jobs per month, marking the largest downward revision since 2009. The initial figures had indicated a robust addition of 2.9 million jobs, or 242,000 per month, but the revised pace is now expected to be around 174,000 jobs per month, still strong but notably lower than previously thought.

The Fed's current benchmark rate, held in a range of 5.25%-5.5%, is the highest in over two decades and has been instrumental in controlling inflation. However, with inflation receding and employment weakening, Powell’s comments suggest a policy pivot aimed at balancing the dual objectives of price stability and a strong labor market. While Powell’s speech provided clarity on the near-term direction of rate cuts, expected by investors to be 25 basis points in September, he offered little insight into the Fed’s strategy beyond that. The central bank's future actions will depend on incoming economic data, with the potential for more aggressive rate cuts if labor market conditions worsen. Powell emphasized the Fed's commitment to avoiding past policy errors, striving for a "soft landing" that reduces inflation without triggering a recession. The success of this delicate balancing act will be critical in determining the U.S. economy's trajectory in the coming months.

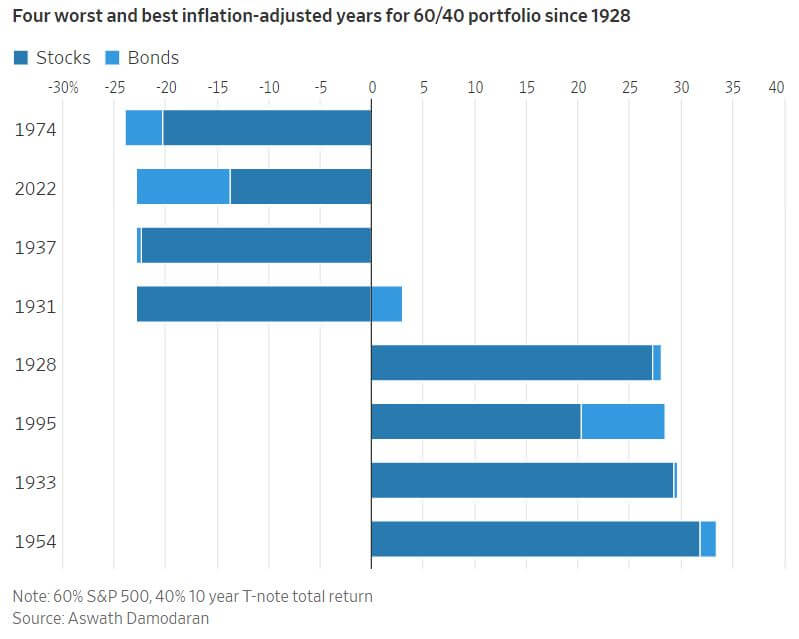

Vanguard's assertion that the classic 60/40 portfolio—a mix of 60% stocks and 40% bonds—would recover from its 2022 downturn has proven true, with the portfolio regaining its losses by February 2024. However, the need for reassurance highlights widespread misconceptions about this approach. The 60/40 mix, commonly understood as 60% in the S&P 500 and 40% in bonds like 10-year Treasuries, is intended to balance risk and return. Despite this, 2022 was the worst year for the 60/40 portfolio since 1974, challenging the belief that bonds always act as a cushion during stock market declines. A key issue is that lower bond yields during a stock downturn limit the potential for bond prices to rise, reducing their effectiveness as a buffer. Historical data shows that while diversification generally makes portfolios safer, it may not prevent investors from panicking during market downturns. Furthermore, bonds offer lower returns compared to stocks over the long term, which poses a different type of risk—lower growth in savings. The 60/40 portfolio is closely tied to the "4% Rule," a guideline suggesting retirees can withdraw 4% of their savings annually with little risk of outliving their money. However, this rule is based on historical U.S. market conditions that may not apply in the future. Recent studies suggest that in today's environment, a safer withdrawal rate might be closer to 2.26% to avoid the risk of financial ruin. As future returns are projected to be lower due to the high price to earnings ratio on equities currently, and with potential risks to Social Security benefits, retirees may need to reconsider their reliance on the 60/40 portfolio. While not obsolete, the 60/40 mix should be viewed with caution, as it is not a guaranteed solution for financial security in retirement.