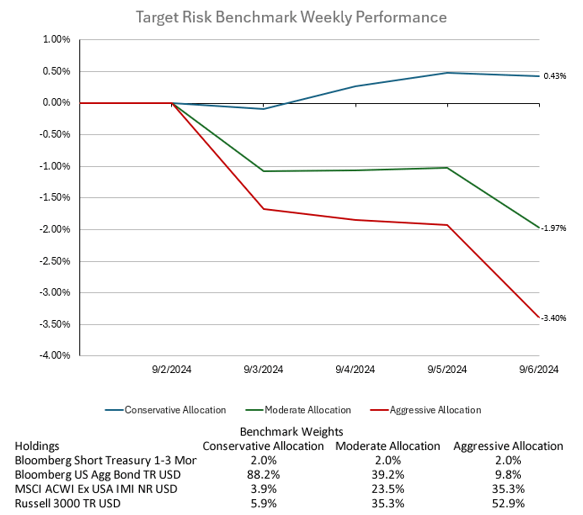

Stocks pulled back but bonds rallied following downbeat U.S. economic releases and a continuing slump in Chinese domestic demand. Friday’s non-farm payrolls indicating a slowing hiring climate may not point towards a recession, but it presents the Federal Reserve with a dilemma in having to balance the risks of slowing labor market conditions while trying to achieve price stability. U.S. Treasuries rallied with yields on two-year notes falling by up to 26 basis points to 3.66%. The 10-year yield settled at 3.72%, down from 3.90% the prior week. This sharp movement in rates continues to support market expectations of a significant easing cycle, with traders now pricing in 1.50% rate cuts by the end of January 2025, possibly including a 50-basis-point reduction at the September FOMC. U.S. stocks were weighed down by a more somber outlook for artificial intelligence-driven spending and news reports of antitrust probes targeting large semiconductors as well as downbeat earnings releases from retailers focused on lower income segments. For the week ending 9/6/2024, the S&P 500 returned -4.14%, underperforming the international markets with MSCI ACWI ex USA returning -3.64%. The Bloomberg U.S. Aggregate Bond Index returned 0.94%, benefiting from this week’s sharp drop in interest rates. The aggressive target risk benchmark returned -3.40%, while the moderate target risk benchmark returned -1.97%. The conservative benchmark benefited from its higher allocation to bond, returning 0.43% for the week.

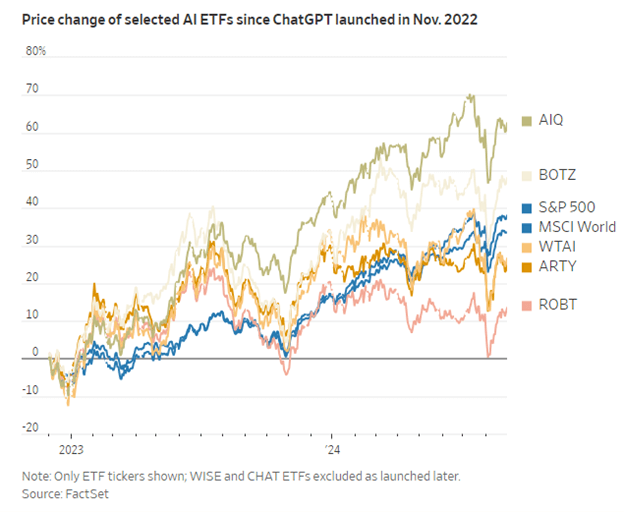

Despite correctly identifying AI as a dominant market trend, many investors in artificial intelligence focused ETFs have faced losses. Notably, three AI ETFs lost money this year, and most others underperformed compared to broader indices like the S&P 500 and MSCI World. This underperformance came even before doubts emerged about the valuation of leading AI stocks, such as Nvidia and Super Micro Computer. The struggle of AI ETFs illustrates a broader cautionary tale about thematic ETFs, which cover various trends, from Californian carbon permits to pet care. Many investors may find that thematic ETFs do not deliver the expected returns, are hard to time correctly, and are difficult to hold over the long term. One key issue with AI ETFs is their structure. Some, like First Trust’s AI-and-robotics fund, have limited exposure to key stocks like Nvidia due to equal weighting or caps on individual holdings. For example, the fund holds only 0.8% in Nvidia, while others, like BlackRock’s iShares Future AI & Tech fund, recently changed from an equal-weighted to a market-value-weighted approach to increase its Nvidia exposure. Such differences in fund strategy can result in significant performance differences between funds. Selecting the right fund within a theme is challenging, relying on both luck and careful examination of fund documents. Furthermore, selecting the right theme itself is difficult, and even more so is the timing. Thematic ETFs often launch during market bubbles, leading to poor returns as prices correct. Research has shown that "specialized" ETFs, on average, typically lose 6% annually over their first five years due to poor timing. Long-term commitment to a thematic fund is also problematic. Many thematic funds are wound up, merged, or change strategies when they lose popularity. The dot-com bubble in the late 1990s and the recent wave of "metaverse" funds, many of which have already shut down, exemplify this risk. When choosing a thematic ETF, it is important for investors to look beyond a fund's name, examine its holdings and structure, and consider whether the ETF truly aligns with their investment goals. High fees and poor historical performance suggest that thematic ETFs are often not worth the cost for most investors.

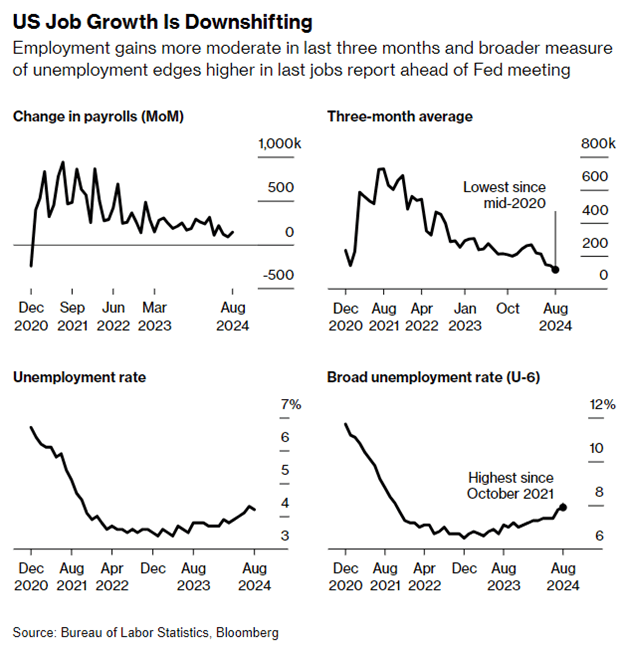

In August, U.S. job growth rebounded, with the economy adding 142,000 jobs, according to the Labor Department, up from a revised figure for July that had sparked fears of an economic slowdown and volatility in global financial markets. The unemployment rate dipped slightly to 4.2%. The Labor Department also revised down its June and July job growth estimates by a total of 86,000 jobs, indicating a weaker labor market during the summer. The latest job report, closely watched by Wall Street, did not provide a definitive answer regarding the size of the Fed’s expected interest rate cut later this month. While the August job growth fell short of economists' expectations of 161,000, it wasn’t weak enough to warrant a larger-than-usual half-percentage-point rate cut. New York Fed President John Williams, speaking after the release of the report, reiterated that rate cuts are forthcoming. However, he did not suggest a heightened urgency for a more significant cut, indicating that the Fed may opt for a more measured approach. Williams emphasized that the data must align with a slowing economy and cooling labor market, allowing the Fed to lower rates gradually to a neutral level that neither stimulates nor restricts economic growth. Job gains in August were primarily driven by hiring in construction and healthcare, while the labor-force participation rate remained stable. Year-over-year wage growth increased to 3.8%. The report was highly anticipated as it followed months of concern over a cooling labor market amidst tapering inflation, which had shifted the focus of economists and investors away from inflation signals to labor market trends. The weaker-than-expected July employment report had reignited fears of a slowdown, with declining job openings and softer economic data causing significant volatility in financial markets in early August. This raised concerns about whether the observed economic slowdown was a temporary reaction, possibly influenced by external factors like Hurricane Beryl, or indicative of a more prolonged downturn. The Fed’s response to the job market data will be closely watched as a key factor in shaping the economic and political landscape.