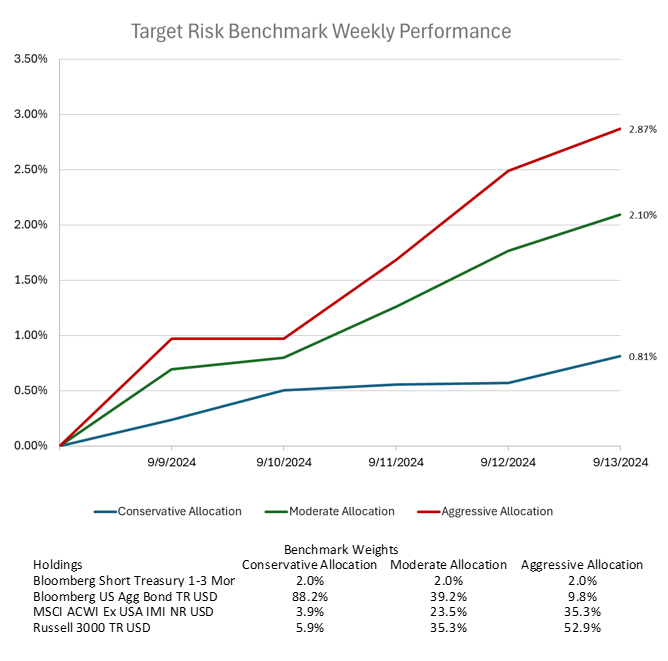

Wall Street traders have revived expectations for a half-point Federal Reserve rate cut, driving a significant stock rally last week. This shift has led to a rotation in the market, with economically sensitive stocks, especially small-cap firms, outperforming the tech megacaps that previously dominated. Investors are optimistic that a Fed rate cut will further fuel broader participation in the rally beyond just the tech sector. The likelihood of a 50-basis-point cut rose from 4% to 40% by the end of the week, leading to lower Treasury yields, a drop in the dollar, and a rise in gold prices. Small-cap stocks, due to their higher leverage compared to larger firms, are expected to benefit more from rate cuts, as this would ease their debt burdens. Despite the broader rotation into defensive sectors like utilities and real estate, the tech giants—referred to as the "Magnificent Seven"—remain strong players, with growth expectations still high. Some analysts argue that tech stocks remain difficult to fade, even though cracks are beginning to show in long-term growth leaders. The ongoing rotation is seen as a potential sign of leadership shifting from growth to value stocks. However, some analysts warn that this market rotation may not offer true diversification, as artificial intelligence (AI)-centric stocks have seeped into other sectors like utilities and industrials. Market movement will likely remain uncertain until clearer signs of US employment data emerge, which will help determine the next direction of risk for investors. Expectations of upcoming rate cuts benefitted multi asset class investors across all risk tolerances, as seen in the target risk benchmarks below. Both domestic and international equities had a strong showing for the week, propelling the aggressive target risk benchmark to a substantial gain of 2.87%. The moderate target risk benchmark was not far behind with a sizeable return of 2.1%. Even the conservative target risk benchmark had a strong week due to falling bond yields, ending with a gain of 0.81%.

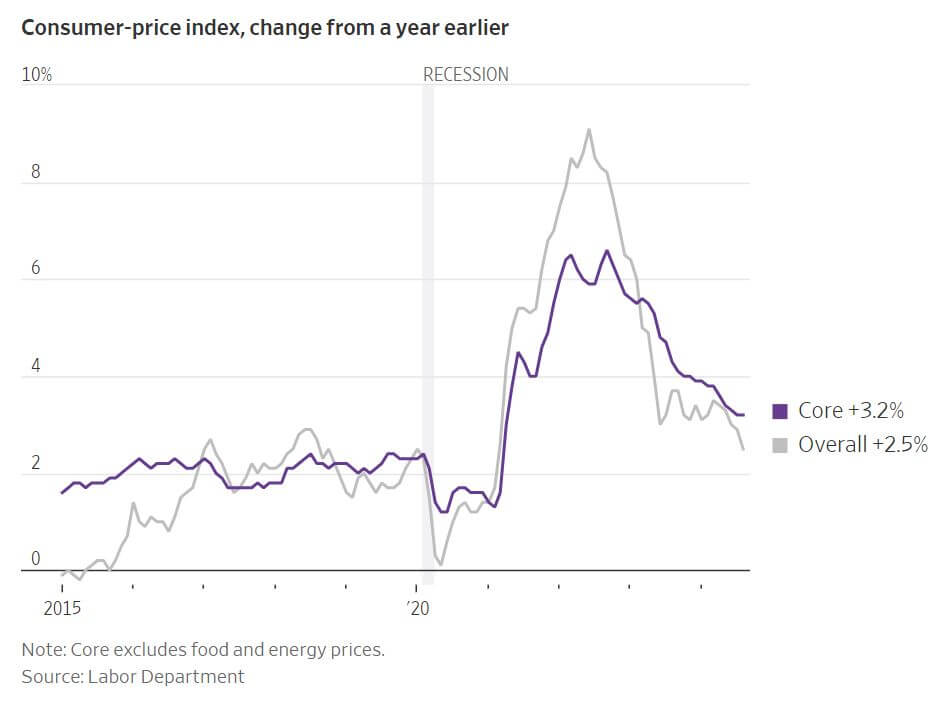

U.S. inflation eased to its lowest level in three years in August, setting the stage for the Federal Reserve (Fed) to consider gradually reducing interest rates at its upcoming meeting. The consumer price index (CPI) rose by 2.5% from a year earlier, down from 2.9% in July, marking five consecutive months of declining inflation. Core inflation, which excludes volatile food and energy prices, remained steady at 3.2%. In August, U.S. producer prices also showed minimal growth, with the Producer Price Index (PPI) for final demand rising by 0.2% month-over-month, slightly above economists' expectations of 0.1%. This follows a flat reading in July, which was revised lower. Annually, the PPI increased by 1.7%, marking its lowest rate since early 2024. Excluding food and energy, the PPI rose 0.3% in August and 2.4% year-over-year. The latest data supports a shift in the Fed's focus from inflation, which has receded from its recent 40-year highs, to a cooling labor market where hiring has slowed. While most central bankers have signaled their readiness to cut rates, the latest CPI data may deter the Fed from a more significant rate reduction, such as a half-percentage-point cut, and push for a more traditional 0.25-point decrease instead. Market participants expect the Fed to lower rates by at least 1 percentage point this year, including a possible 0.5-point cut in November or December. Meanwhile, inflation in key areas, like food, used vehicles, and energy, has slowed. Falling oil prices suggest further declines in gasoline costs, potentially alleviating consumer concerns over economic conditions. Additionally, price increases for housing are expected to moderate as more renters sign new leases, which could help bring overall consumer prices closer to the Fed’s 2% inflation target. The Fed's impending decision on interest rates will be pivotal, especially as investors look for clarity on the direction of U.S. monetary policy amid mixed economic signals and a volatile market environment.

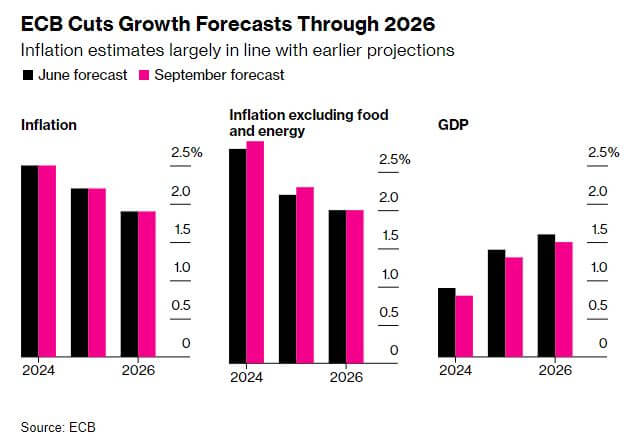

The European Central Bank (ECB) lowered its key deposit rate by 25 basis points to 3.5%, marking the second rate cut this year. This decision aligns with expectations as inflation trends toward the 2% target, but concerns about the euro area economy persist. ECB President Christine Lagarde emphasized the need for a data-dependent approach given the uncertainty in the economic outlook, cautioning that a downward path for rates is not guaranteed in terms of sequence or volume. Traders have adjusted their expectations, predicting an additional 36 basis points of easing by the end of the year, suggesting a quarter-point cut is likely, though further cuts are less certain. The ECB's confidence in reaching its inflation target has grown, but the region's economy shows signs of weakness, with lackluster household support for the recovery and continued challenges in manufacturing due to subdued external demand. Consequently, the ECB has downgraded its growth forecasts for 2024, 2025, and 2026, projecting a 0.8% GDP expansion this year, down from the prior 0.9% forecast. The inflation outlook remains broadly stable, although wage growth is expected to stay high and volatile. In addition to the deposit rate cut, two other rates were reduced by 60 basis points each, reflecting a strategic shift with limited immediate impact. The ECB's measures come just ahead of anticipated policy easing by the U.S. Federal Reserve and the Bank of England. Despite inflation falling to 2.2% in August in the EU, service-price growth accelerated, partly due to the Paris Olympics, raising concerns among ECB officials about declaring victory over inflation. Some, like Executive Board member Isabel Schnabel, stress the need for careful, data-driven decisions on future rate cuts, while Chief Economist Philip Lane warns that the return to 2% inflation is not yet assured. Analysts forecast continued rate reductions until mid-2025, though economic uncertainties persist.