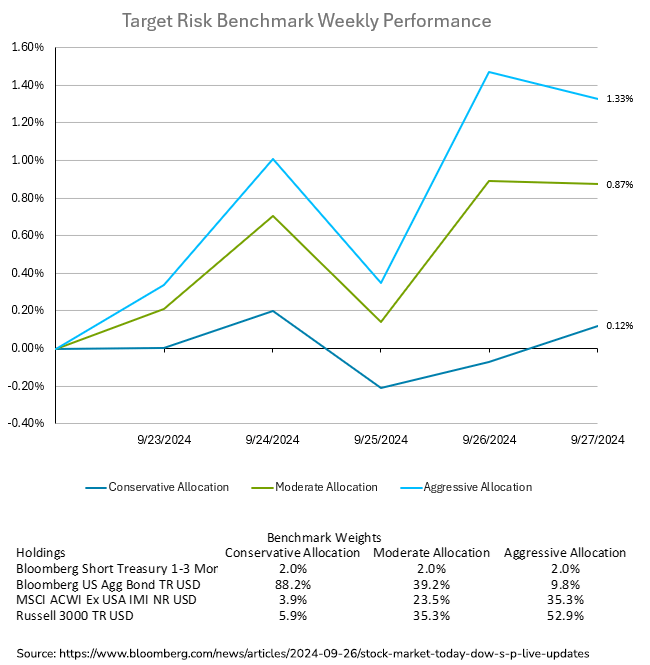

US stocks had their third straight week of gains last week, despite Friday's mixed performance, as investors gain confidence that the economy is cooling without a sharp downturn. Treasury yields fell as data reinforced expectations of further interest rate cuts by the Federal Reserve. The dollar had a fourth consecutive weekly loss, and the 10-year Treasury yield ended the week around 3.75%. Global central banks in Switzerland, Mexico, Hungary, and the Czech Republic cut interest rates, bolstering market sentiment. This week, US jobs data will be crucial in gauging the labor market's health. Chris Larkin of E*Trade noted that recent data supports a balanced economic environment, with inflation subdued and no signs of a sharp slowdown. Damian McIntyre of Federated Hermes emphasized the strength of recent economic indicators as a positive sign for investors. Globally, China’s CSI 300 Index saw its best week since 2008, and European stocks reached record highs, closing their best week in over four months. Oil prices rose following increased tensions in the Middle East after Israel struck Hezbollah’s headquarters in southern Beirut. The week was better for aggressive investors than for conservative investors, as seen in the target risk benchmarks below. Much of the improving inflation outlook is already baked into bond yields, meaning that last week’s personal consumption expenditures (PCE) release did not move bond prices much. The conservative target risk portfolio had a small gain of 0.12% as a result. Much of the weekly action was seen in large gains in international equities. This benefitted the moderate and aggressive target risk allocations, which saw gains for the week of 0.87% and 1.33% respectively.

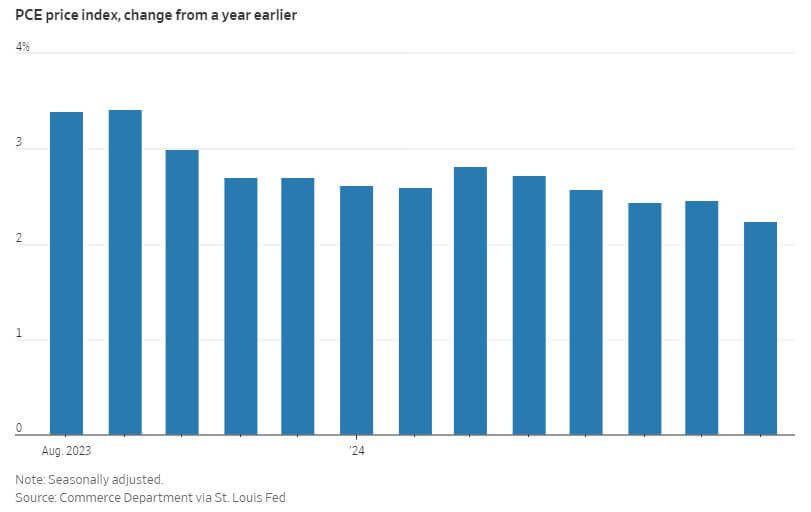

In August, the core personal consumption expenditures (PCE) price index, the Fed's preferred measure of underlying US inflation, rose modestly by 0.1% from July, indicating a cooling economy. On a three-month annualized basis, core inflation increased by 2.1%, aligning with the Fed's 2% target. Consumer spending, adjusted for inflation, also increased by 0.1%, while nominal personal income rose 0.2%. The personal saving rate declined slightly to 4.8%. The data suggests the Fed may continue its recent easing of monetary policy, as Treasury yields and the dollar fell in response. The Fed recently initiated a half-point rate cut, and market participants are divided on whether another significant cut will occur in November. The August data revealed broad cooling, with services prices excluding housing and energy rising 0.2% for the second consecutive month, and goods prices excluding food and energy dropping 0.2%, the most in three months. Bloomberg economists suggest that the cooling in income and inflation supports the Fed's recent decision to cut rates and predict a continued focus on employment to balance its dual mandate. Economists predict that U.S. inflation will reach the Federal Reserve's 2% target by early next year, closely aligning with the Fed's latest projections. The Fed's recent economic forecasts project the PCE index to average 2.1% in 2025 and 2% in 2026. Both the Fed and surveyed economists anticipate further rate cuts, totaling another half-point reduction by year-end. Regarding the labor market, both economists and Fed officials foresee the unemployment rate averaging 4.4% in 2025, slightly higher than the current 4.2%. While recession odds for the next year have decreased to 30%, the US economy is expected to slow, with GDP growth forecasted to decline from 2.6% this year to 1.8% in 2025, compared to the Fed's 2% estimate for 2024-2026.

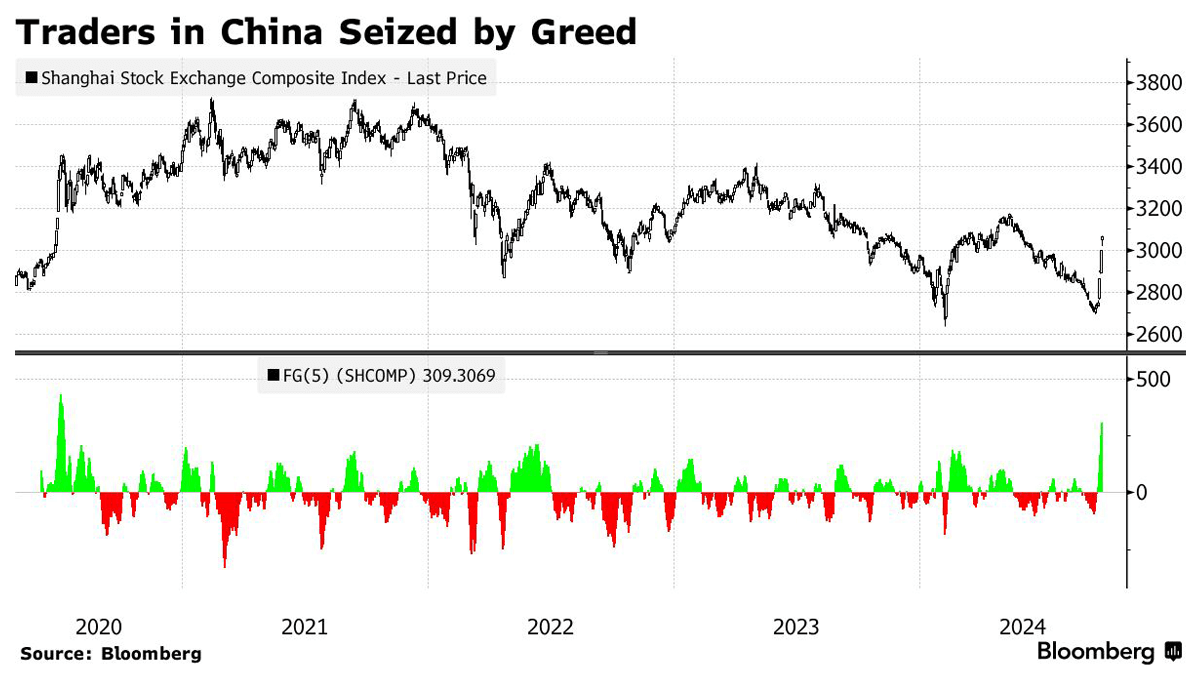

China's central bank, led by Governor Pan Gongsheng, introduced a major monetary stimulus package to revive the slowing economy, addressing concerns over reduced growth and declining investor confidence. Key measures include cutting a short-term interest rate and reducing the reserve requirement ratio (RRR) for banks to its lowest level since at least 2018, both announced simultaneously for the first time since 2015. Additionally, Pan announced plans to support the struggling property sector by lowering borrowing costs on $5.3 trillion in mortgages and easing rules for second-home purchases. The central bank will also provide at least 800 billion yuan ($113 billion) in liquidity support and is considering establishing a market stabilization fund.

These stimulus measures led to a surge in market activity, overwhelming the Shanghai Stock Exchange. Early Friday, trading volume reached 710 billion yuan ($101 billion) within the first hour, causing order processing delays and system glitches. Despite these issues, the overall sentiment remains positive as investors rush to capitalize on the rapid market gains following China's boldest policy actions in decades, which led to a 15% rise in the onshore benchmark this week. This week’s trading frenzy, with turnover approaching 1 trillion yuan in the morning session alone, is the highest recorded before a national holiday, driven by a fear of missing out on the rally.

Pan’s moves have temporarily lifted market confidence and bought time for the Chinese economy, which faces challenges such as a property market downturn, weak consumer prices, and rising global trade tensions. However, economists, including Duncan Wrigley from Pantheon Macroeconomics, argue that more comprehensive reforms are needed to address underlying economic issues and stimulate consumption. Despite the market’s positive reaction, many experts believe the measures are insufficient to prevent Japan-style deflation and that China needs a more coherent strategy to encourage its 1.4 billion citizens to increase spending. There are debates on whether China should abandon its strict fiscal rules to boost spending on social welfare and infrastructure. The Chinese government's reluctance to adopt direct cash handouts, fearing it could lead to unsustainable welfare expenses, highlights the complexity of the situation. Meanwhile, investment in China’s property market remains weak, as confidence in the private sector is low due to the government’s past regulatory actions and ongoing geopolitical tensions.