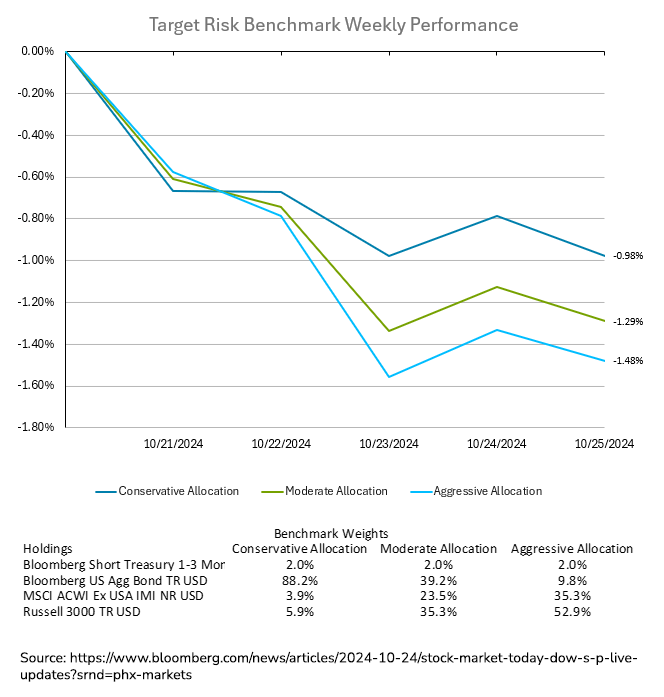

A stock rally faltered on Friday as bank losses weighed on the broader market, despite gains in technology shares. The S&P 500 closed flat after an initial 1% rise, with banking stocks suffering—New York Community Bancorp fell 8.3%, Goldman Sachs dropped 2.3%, and JPMorgan lost 1.2%. Crypto shares also took a hit following reports of a federal investigation into Tether for potential sanctions and anti-money laundering violations. Bitcoin fell 2% and the 10-year Treasury yield edged higher to 4.24% amid broader market caution. Investors remain wary ahead of the U.S. presidential election, jobs data, and Federal Reserve policy updates, which could shape the economic outlook. The Nasdaq 100 rose 0.6% and tech giants—the Magnificent Seven—extended their gains, positioning themselves to drive future market performance. Upcoming earnings from Alphabet, Meta and Amazon are expected to show robust growth, while Nvidia’s results in November could affect sentiment given its AI leadership. Despite volatility, strategists view recent market swings as signs of a maturing bull rally, with breadth expanding across tech, banks, and commodities. However, tech valuations are under scrutiny, as investors grow impatient for AI-driven profitability. Analysts expect earnings growth to accelerate in key firms like Microsoft, Apple and Nvidia, though the rest of the sector may slow. U.S. consumer sentiment hit a six-month high, reflecting easing inflation expectations. Assets declined across all asset classes last week, resulting in losses for investors across all risk tolerances. Conservative investors fared the best, with the conservative target risk benchmark below falling by -0.98%. The losses in moderate and aggressive portfolios were larger, with the moderate target risk benchmark falling -1.29% and the aggressive target risk benchmark -1.48%.

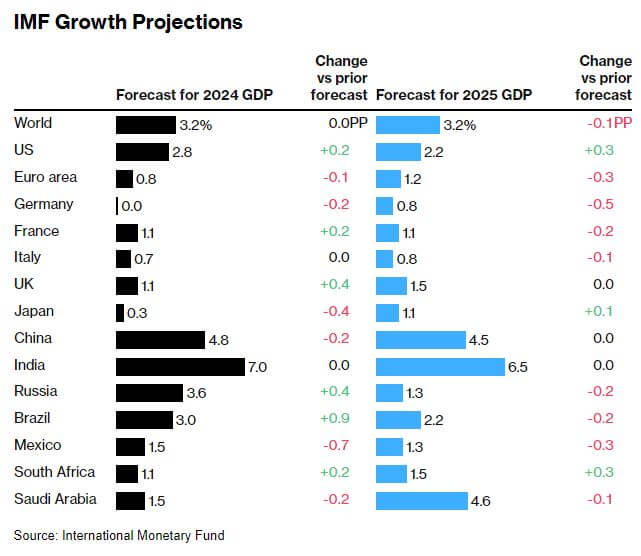

The International Monetary Fund (IMF) has revised its global growth forecast for 2025 to 3.2%, down by 0.1 percentage point from July’s estimate, while maintaining this year’s outlook at 3.2%. Inflation is expected to decelerate from 5.8% in 2024 to 4.3% next year, yet geopolitical conflicts, trade protectionism, and rising public debt pose significant threats to global stability. IMF Chief Economist Pierre-Olivier Gourinchas highlighted risks from regional conflicts disrupting commodity markets and trade barriers stifling economic activity, projecting that global output could shrink by 0.5% by 2026 if protectionism escalates. The IMF expressed concern over surging global debt, which is set to reach $100 trillion by year-end, driven by U.S. and Chinese borrowing. The fund adjusted regional forecasts, lowering euro area growth to 1.2%, citing manufacturing challenges in Germany and Italy, while Mexico’s outlook reflects the impact of monetary tightening. China’s growth forecast was reduced to 4.5% due to real estate sector weakness, with the IMF acknowledging the recent but insufficient policy efforts.

The U.S. economy is outperforming other advanced economies, driven by increased investment, higher productivity, and wage growth, according to the IMF’s latest report. The IMF upgraded its 2025 U.S. GDP growth forecast to 2.2%, making it the fastest among the G7 economies. The IMF attributes the U.S.’s economic momentum to strong nonresidential investment, bolstered by government-led green energy and infrastructure initiatives, alongside robust consumer spending fueled by rising real wages. U.S. investment, measured by gross fixed capital formation, is projected to grow 4.5% in 2025—more than three times the rate of other advanced economies. This surge marks a significant shift from the previous decade, when U.S. investment tracked in line with other advanced nations. By comparison, Germany, once Europe’s economic leader, is now facing consecutive annual declines in investment. Economists note that increased U.S. energy independence, supported by fracking and new technologies, has insulated the country from global energy shocks, especially after Russia’s invasion of Ukraine. In contrast, European firms face much higher energy costs, limiting their ability to invest in productivity-enhancing technologies. The divergence between the U.S. and Europe underscores the long-term impact of sustained investment in software, equipment and intellectual property.

This week saw heightened volatility in U.S. Treasury markets, with bond yields swinging sharply as traders reassessed their expectations for Fed policy and upcoming election outcomes. The ICE BofA Move Index, a key measure of Treasury volatility, hit a new high for 2024, signaling potential turbulence ahead. Initially, the 10-year Treasury yield surged past 4.2%, marking its highest level since July, reflecting a 13-basis-point increase. Uncertainty around inflation, fiscal policy, and the election has fueled these market shifts. Analysts warn that volatility may persist as investors brace for critical events, including the release of employment data, inflation reports, and the Fed’s policy meeting on November 6, just after the U.S. election. Arif Husain of T. Rowe Price anticipates 10-year yields testing 5% in the coming months amid rising inflation fears and concerns about fiscal policy. High-profile investors like Paul Tudor Jones and Stanley Druckenmiller have also adopted bearish stances, avoiding bonds due to inflation risks. Election-related uncertainty, particularly the potential for Republican control of both the White House and Congress, has dampened demand for longer-term bonds due to expectations of expansive fiscal policies that may stoke inflation. Some traders, however, see signs that the recent bond selloff may have been excessive. Hedging activity on Friday pointed to bets that yields could dip to 4.12% by Monday. Treasury returns have been underwhelming due to the recent selloff, with year-to-date gains eroding amid October’s losses, now up just 1.7% versus 4.4% for cash-like T-bills. Investors now expect rate cuts of 129 basis points through 2025—down from 195 basis points a month ago. Parametric reports on the ballooning U.S. debt here.