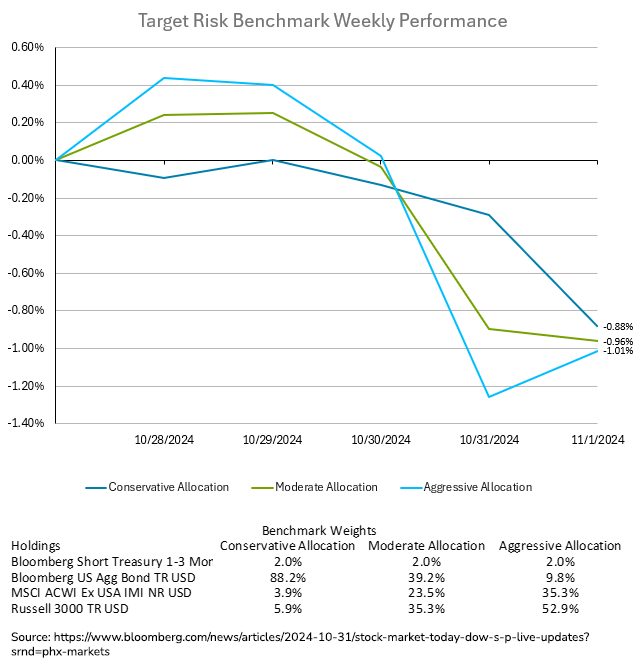

U.S. stocks rebounded late last week as investors focused on strong corporate earnings, despite economic uncertainties surrounding the upcoming presidential election. Major tech stocks led the gains: Amazon surged 6.2% on solid earnings, while Intel and Exxon Mobil rallied on strong outlooks. The S&P 500 ended its two-day decline, buoyed by resilient corporate performance, even as Apple slipped after a softer forecast. Treasury yields rose, indicating cautious investor sentiment, with the 10-year US Treasury note ending the week at 4.37%. Investor sentiment is increasingly bullish, as shown by reduced cash holdings and increased allocations to equities. This bullish sentiment coincides with the Fed’s easing policy, supported by robust inflows into equities and bonds, and rising risk appetite. Deutsche Bank analysts attribute these inflows to increased household income and savings built during the pandemic. Meanwhile, hedge funds and speculators raised long positions on the dollar, anticipating its safe-haven appeal amidst election uncertainties and potential changes to tariffs. As U.S. fiscal and monetary policies evolve, markets remain watchful of potential shifts in the economic landscape while largely optimistic about sustained growth in equities and a stable recovery trajectory. The concentration of economic data releases, corporate earnings, and the upcoming election last week resulted in high volatility for the period across asset classes, but the end result was the same for aggressive and conservative investors. The aggressive target risk benchmark ended the week with a loss of -1.01% after the equity rebound on Friday. The conservative target risk benchmark ended the week with a similar loss of -0.88% after the increase in bond yields to end the week. The moderate target risk benchmark split the difference with a loss of -0.96%.

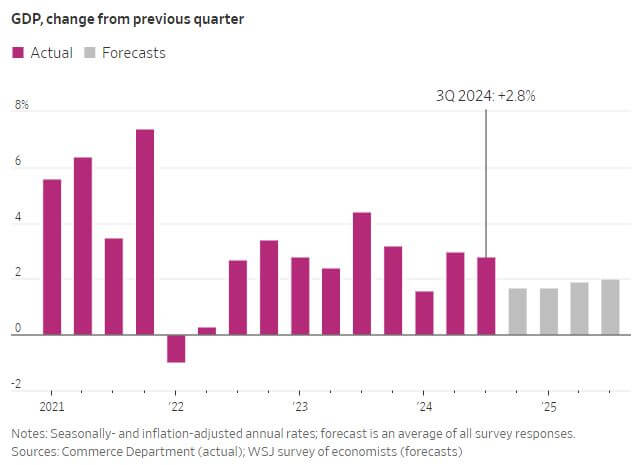

The U.S. economy grew at a steady 2.8% annualized rate in the third quarter, with consumer spending driving the momentum ahead of the election. Household purchases surged by 3.7% for the quarter, the highest since early 2023, as spending on autos, furnishings, and recreational items rose. Government expenditure also played a significant role, rising by 5%. Business investment grew, led by spending on equipment and transportation, while AI-related tech investments in computers surged 32.7%. However, residential investment fell 5.1%, weighed down by high mortgage rates. Despite strong growth, challenges remain. Trade and inventory factors slightly restrained GDP, and lower-income households showed increased price sensitivity as high costs linger. According to Bloomberg Economics, while the GDP figures are positive, underlying consumer stability varies across income brackets, with wealthier households primarily fueling spending. The Q3 GDP data was followed by September figures for the Fed’s core personal consumption expenditures (PCE) index, which excludes food and energy. PCE rose by 0.3% in September compared to the month prior, marking a 2.7% year-over-year increase. Overall inflation was recorded at 2.1%, near the Fed’s 2% target. Inflation-adjusted consumer spending grew 0.4%, driven by stronger wages, while the savings rate dipped to 4.6%. Wages and salaries increased by 0.5% for the second month, and employment costs moderated, aligning with Fed Chair Jerome Powell’s view that labor market pressures on inflation are diminishing. The October employment report, showing only a modest gain of 12,000 nonfarm jobs, supports the Fed’s trajectory to cut interest rates by 25 basis points in their upcoming meetings. While payrolls were affected by recent hurricanes and a Boeing strike, downward revisions to August and September job growth indicate a cooling labor market.

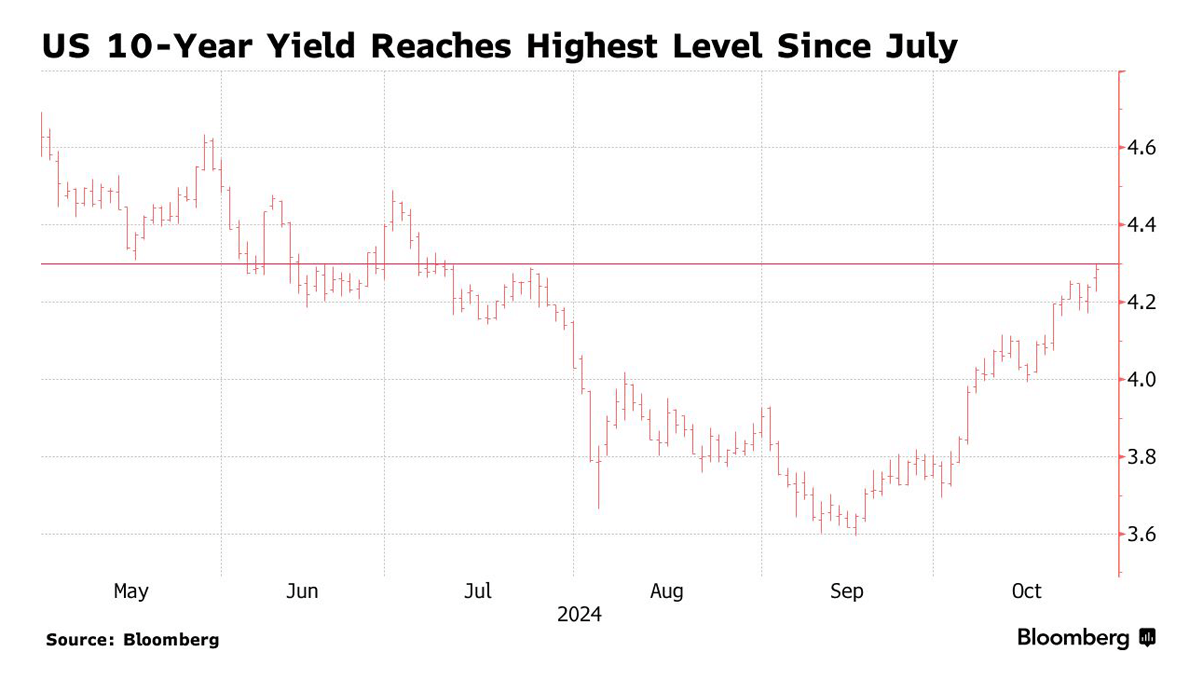

As the U.S. presidential and congressional elections approach, the Treasury market—the backbone of global finance—faces scrutiny, with ten-year Treasury yields rising from 3.6% in mid-September to 4.3%. This increase reflects both market volatility and potential concerns over America’s fiscal direction, though political impact on yields remains limited so far. However, a clean electoral sweep by either party could alter fiscal constraints, especially with bold tax and spending promises from both candidates. Projections already forecast U.S. deficits to average 5.5% of GDP over the decade, fueling growing Treasury issuance, especially of short-term bills that require frequent refinancing. Experts are divided on the impact of increasing U.S. debt. Some analysts expect “bond vigilantes”—investors who might resist excessive government spending—to impose limits on fiscal policy by demanding higher yields. Others argue that the effect of new debt issuance is minimal compared to inflation and growth expectations, as the U.S. Treasury market’s high liquidity absorbs additional bonds without major disruptions. The term premium, indicating compensation investors demand for risks like inflation and political uncertainty, has slightly increased. However, it remains low compared to past decades when inflation or federal debt raised greater concerns. Yet, analysts caution that history may not reliably predict current outcomes given unprecedented peacetime debt levels and the looming debt ceiling reinstatement next year. Political gridlock could increase default risks, making even small interest rate adjustments impactful as debt grows. The economic foundation for the next administration appears strong, though Treasury market stability may hinge on prudent fiscal management amidst escalating debt.