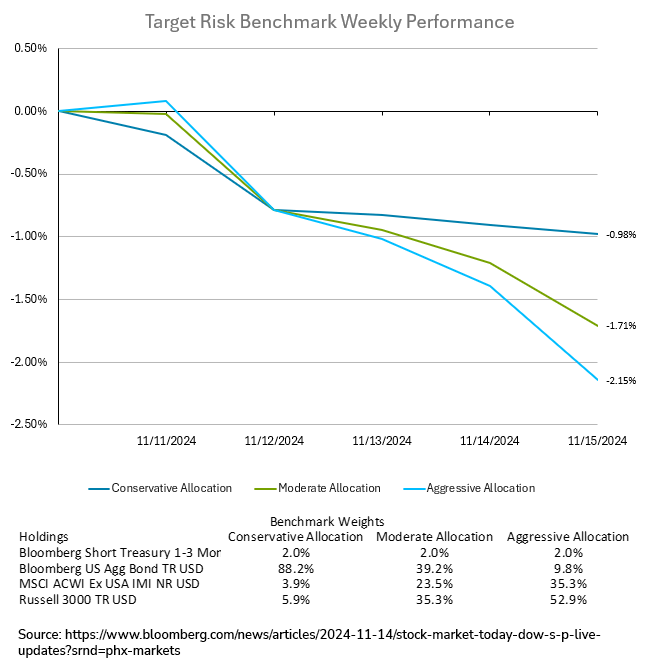

Stocks faced significant declines on Friday, capping their worst week in over two months as investor sentiment shifted on fading optimism around Trump-era pro-business policies and Federal Reserve monetary easing. The S&P 500 dropped 2.1% for the week, erasing over half its post-election rally, while the Nasdaq 100 fell over 3%, marking their steepest losses since early September. Tech stocks led the declines, with major players like Amazon, Nvidia, and Meta shedding over 3%. Market bets on a December rate cut by the Fed eased to 56%, down from 80% earlier in the week, following cautious remarks by Fed Chair Jerome Powell. He emphasized a measured approach to policy easing, reinforced by stronger-than-expected retail sales data and upward revisions for prior months. Boston Fed President Susan Collins and Chicago Fed President Austan Goolsbee reiterated that any rate decisions will hinge on inflation trends and incoming economic data. The broader market recalibrated as investors weighed the potential inflationary costs of President-elect Trump’s fiscal agenda, with growing concerns about larger deficits and debt levels. Treasury yields briefly surged to 4.5%—the highest since May—before retreating to 4.44%, while the dollar softened after a seven-week rally. The losses were broad based across asset classes, resulting in a down week for investors across all risk tolerances. The conservative target risk benchmark held up the best, finishing the week down -0.98%. The moderate and aggressive target risk benchmarks suffered larger declines, finishing the week with declines of -1.71% and -2.15%, respectively.

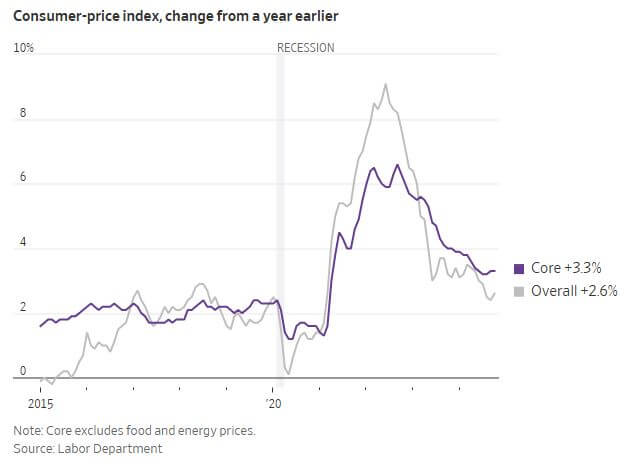

In October, U.S. consumer prices rose by 2.6% from a year prior, up from September's 2.4% increase, reflecting the ongoing, uneven cooling trend in inflation. Core inflation, which excludes volatile food and energy prices, climbed 3.3% year-over-year, aligning with economists' expectations. This moderate uptick in inflation, combined with steady consumer spending and employment, suggests the Fed might still reduce interest rates in December, though firmer inflation could spark debate over slowing the pace of rate cuts in 2024. Fed Chair Jerome Powell indicated that bumps in inflation were anticipated, attributing persistent price increases to lagging adjustments in areas like rent, rather than new inflationary pressures. Energy prices remained stable, balancing declining gasoline costs with rises in electricity and natural gas prices, while used cars and airline fares saw notable month-over-month gains. Looking forward, the Fed aims to strike a balance, gradually easing interest rates without rekindling inflation. Central bank officials, however, remain cautious; they want to avoid prematurely lowering rates too far, potentially risking economic stability. While some Fed members, like Dallas Fed President Lorie Logan, believe the neutral rate—a level that neither spurs nor suppresses growth—might be near, they advocate a cautious approach, akin to navigating shallow waters. This aligns with their goal to stabilize inflation while sustaining the labor market, without inducing a recession.

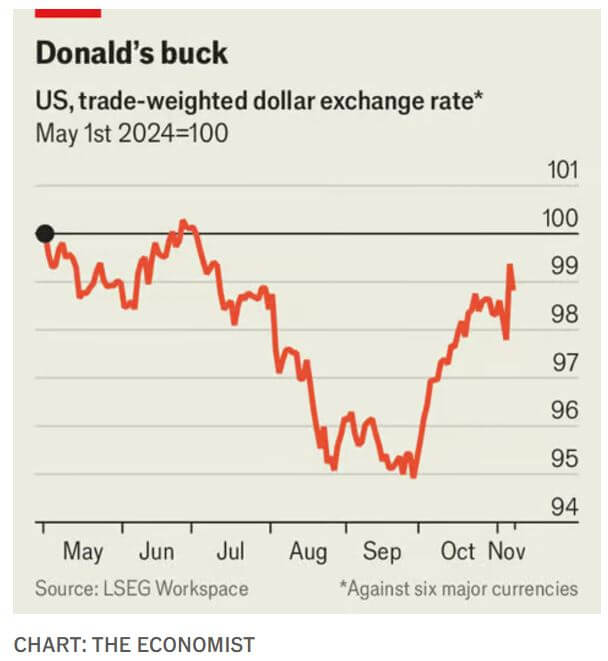

In 1971, Treasury Secretary John Connally famously remarked that the dollar was “our currency, but your problem,” a sentiment that endures as the dollar’s fluctuations profoundly impact the global economy. With Donald Trump’s election as U.S. President, anticipated tax cuts, deregulation, and increased government borrowing could drive up inflation and lead the Fed to maintain higher interest rates, making dollar assets more attractive and strengthening the currency. Already, a rising dollar has led to a 1.5% appreciation against other major currencies, spurred by expectations of persistently high U.S. interest rates. A stronger dollar can dampen global growth by increasing the costs of imports, especially as much of global trade is conducted in dollars. Emerging markets, more sensitive to dollar fluctuations, face potential GDP declines with a 10% dollar appreciation estimated to cut their output by 1.9 percentage points. Advanced economies are also affected, though less severely, with declines of 0.6 percentage points on average. The dollar’s strength impacts global economies through trade and financial channels. Dollar-priced imports become more expensive, curbing demand and straining supply chains, particularly in Asia and Latin America, where dollar stability is crucial. Financially, countries and firms with dollar-denominated debt face higher burdens, and rising U.S. rates deter investment in emerging markets, prompting capital outflows and higher local interest rates. While the Fed recently cut rates, allowing some temporary relief, the upward pressure on global borrowing costs could persist, with broader implications for central banks striving to support weak growth. Though Trump has criticized the strong dollar for harming U.S. manufacturing, his administration’s policies may sustain its strength, posing challenges for global economies dependent on a stable dollar.