A late-year selloff in leading technology stocks has capped a remarkable 2024 for U.S. equities, with major indices retreating amid thin trading. Tesla and Nvidia led a 2.1% drop in the “Magnificent Seven” group of technology stocks Friday as broader market indices, including the Dow Jones and Russell 2000, also declined. Market experts attribute the volatility to year-end portfolio rebalancing by institutional investors and muted trading volumes typical of the holiday season. Redemptions in tech and cryptocurrency funds underscored investors taking some gains off the table, with the tech sector enduring its longest outflow streak since early 2023. Despite 2024’s robust gains, analysts caution against overreliance on elevated tech valuations, which embed aggressive earnings growth expectations. Bloomberg Intelligence estimates the tech sector needs to deliver nearly 40% earnings growth to justify its market-cap share, amplifying downside risks if results fall short. Market strategists highlight the importance of diversification, noting the high concentration risk in a handful of megacaps.

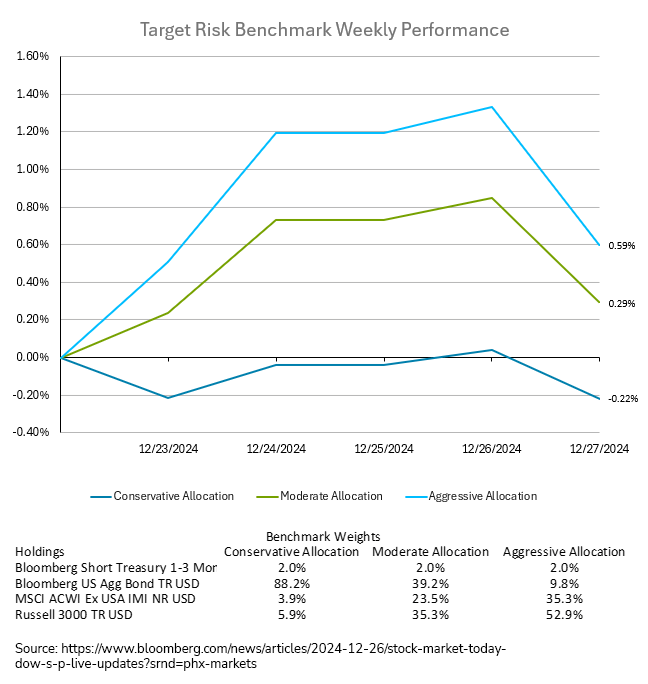

Even with the Friday selloff in equities, aggressive portfolios outperformed conservative allocations for the week. The Bloomberg US Aggregate Bond Index finished the week with a loss of -0.33%, with the yield on the US 10 Year Treasury note rising to end the week at 4.62%. The rise in bond yields led the conservative target risk benchmark to a weekly loss of -0.22%. International and domestic equities both finished the week with gains, bolstering the return for the moderate and aggressive target risk benchmarks. The moderate target risk benchmark ended the week with a small gain of 0.29%, while the aggressive target risk benchmark held on to a weekly gain of 0.59%.

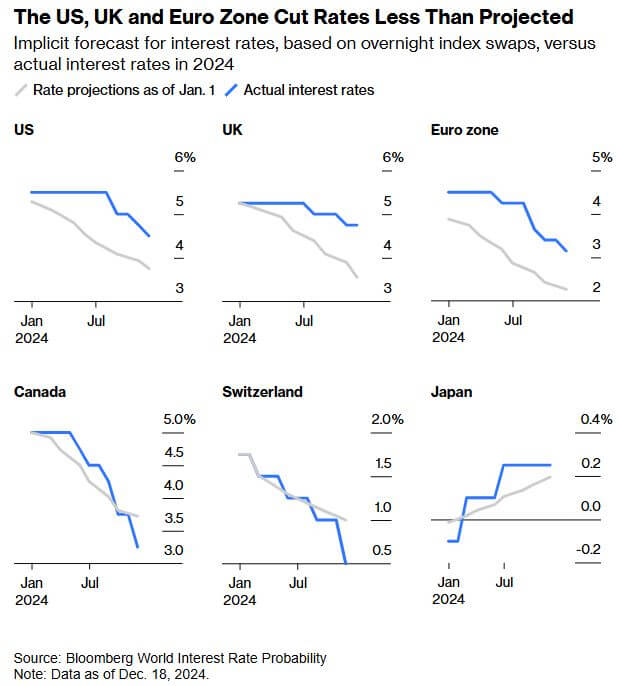

Central banks have navigated a challenging year in their effort to combat inflation, with mixed success. As 2024 concludes, the optimism of a swift descent from post-pandemic interest rate peaks has been tempered by persistent economic pressures and uneven coordination among global policymakers. Divergent economic conditions have driven central banks onto varied paths. The Federal Reserve, constrained by a resilient U.S. economy, only began easing rates in September, sustaining high bond yields and a strong dollar, which hindered global inflation control. The Bank of England and European Central Bank cut rates less than anticipated, while Canada and Switzerland moved faster. In contrast, Japan and emerging markets like Brazil faced unique challenges, with Japan raising rates and Brazil resuming hikes due to currency pressures. Inflation has receded globally but remains stubborn in the U.S., where disinflation stalled despite earlier gains. Consumer expectations for future inflation persist, compelling central banks to maintain cautious policies. Political factors, such as the potential inflationary impact of Donald Trump’s economic agenda, including proposed tariffs, amplify uncertainty. Despite coordinated rate cuts dominating 2024, central banks in developed markets have adopted a "higher-for-longer" stance, wary of premature easing. Emerging markets, having acted early against inflation, now face renewed hikes. Global progress has been made—particularly as China’s slowdown exports deflation—but rates remain significantly above pre-pandemic norms, straining economies. The year concludes without major financial crises, but central banks remain vigilant as geopolitical instability, fiscal challenges, and inflation fears loom, threatening a prolonged period of precarious economic management.

Wall Street’s latest lucrative bet centers on Argentina, defying the country’s history of sovereign debt defaults and economic instability. Investors are flocking to Argentine markets, spurred by President Javier Milei’s bold economic overhaul. Hedge funds and money managers have reaped significant gains, with Argentine stocks outperforming globally and government bonds surging. The MSCI Argentina ETF has climbed over 60%, while the S&P Merval Index has soared by more than 160% in local currency terms this year. Milei, a libertarian outsider, assumed office in December 2023 after campaigning on radical fiscal reforms. His austerity measures include halting public works, cutting subsidies, and narrowing currency exchange disparities. These policies have triggered short-term economic pain, exacerbating poverty, but have also yielded notable successes: inflation has sharply declined, Argentina achieved a quarterly fiscal surplus for the first time in over a decade, and the economy has emerged from recession with 3.9% growth in Q3 2024. Investor sentiment has shifted dramatically. Argentina’s hard-currency debt index has delivered a 90% return this year, while the country’s markets have attracted increased participation from distressed-debt specialists and emerging-market funds. Despite progress, challenges persist. Argentina faces an $8 billion foreign currency reserve deficit, raising concerns over its ability to meet bondholder obligations. To address this, Milei is negotiating with the International Monetary Fund (IMF) for new financing. Investors are optimistic about Milei’s reform trajectory, bolstered by his international outreach and disciplined fiscal approach. While uncertainties remain, Argentina’s potential for sustained economic recovery and financial stability has captivated global markets, signaling a possible transformation of its troubled economic narrative.