The stock market experienced significant volatility on Friday as shifting news about tariffs disrupted trading across multiple asset classes. Earlier in the day, optimism in the technology sector had calmed investor anxieties, but a White House announcement about President Donald Trump’s tariff plans quickly reversed that sentiment. The statement indicated that Trump intended to impose levies on China, Mexico, and Canada over the weekend, which led to a rise in the dollar and declines in stock prices. Earlier reports suggesting a one-month delay in implementation had briefly weakened the dollar, but those were quickly refuted. Oil prices surged after Trump specified that crude oil imports would also be subject to tariffs. Market analysts noted that Friday’s fluctuations were a reminder of how unexpected developments can swiftly alter market sentiment. In the technology sector, concerns about AI investment and earnings growth loomed. The so-called "Magnificent Seven" tech stocks, which have been driving the market rally for the past two years, faced scrutiny over their future profitability. With the release of earnings from several of these firms, investors expressed relief that AI-related concerns had not significantly impacted demand or revenue. Retail investors continued to show confidence, pouring $8.1 billion into US stocks, the highest level in two years. Despite the week’s turbulence, analysts remain optimistic about the broader market. UBS Global Wealth Management’s Solita Marcelli pointed to factors such as economic productivity gains from AI, strong US economic activity, healthy earnings growth, lower borrowing costs, and increased capital market activity as reasons for continued stock market strength.

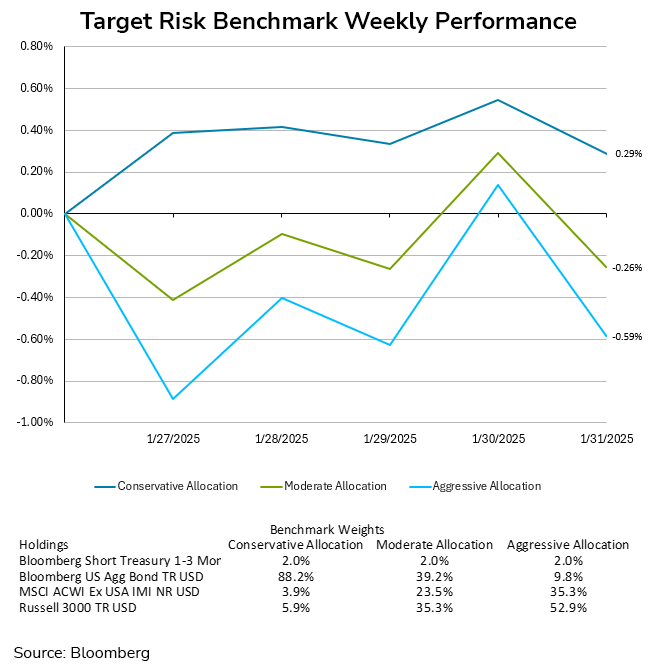

The sudden shift in sentiment weighed on returns for investors with higher risk tolerances for the week. The decline in equities resulted in the aggressive target risk benchmark falling by -0.59% for the week, while the moderate target risk benchmark held up better with a weekly decline of -0.26%. The risk-off shift saw bond yields decline in a bid for safety, resulting in the conservative target risk benchmark performing the best of the three for the week with a gain of 0.29%.

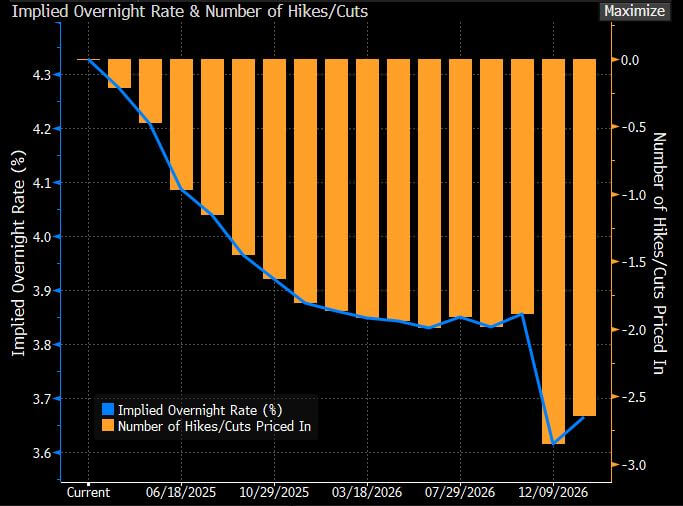

The Federal Reserve has paused its recent cycle of interest rate cuts, opting for a cautious approach as it assesses inflation trends and economic conditions. The decision maintains the federal funds rate at approximately 4.3% following three consecutive reductions from a high of 5.3% last September. Fed Chair Jerome Powell emphasized that, with rates now less restrictive, there is no urgency to adjust policy further. Projections suggest two potential rate cuts in 2025, a revision from four previously expected, contingent on continued inflation moderation. Key considerations include whether price growth is aligning with the Fed’s 2% target and the extent to which interest rates are constraining economic activity. The Federal Reserve’s preferred inflation gauge, the core PCE index, remained subdued in December, rising 0.2% month-over-month and 2.8% year-over-year. On a three-month annualized basis, inflation slowed to 2.2%, the lowest since July. Real disposable income showed minimal growth, contributing to a declining savings rate of 3.8%, the lowest in two years. Consumer spending remained strong, with inflation-adjusted spending increasing 0.4%. The U.S. economy grew at an annualized 2.3% in Q4 2024, supported by strong consumer spending, which rose 4.2%, the highest in consecutive quarters since 2021. Business investment declined, partly due to a Boeing strike, while residential investment showed signs of recovery. The economy expanded 2.8% for the year, outperforming global peers. Concerns persist regarding persistent inflationary pressures, particularly due to businesses’ annual price resets, which were relatively large in prior years. Additionally, political and economic uncertainties, including potential tariff increases, could complicate inflation dynamics. Market reactions to previous rate cuts have demonstrated the influence of broader economic sentiment, with long-term yields rising despite the Fed’s easing measures. This has limited the anticipated benefits for interest-sensitive sectors such as real estate. If inflation remains stubborn or external factors such as trade policy disrupt inflation expectations, the Fed may extend its pause indefinitely.

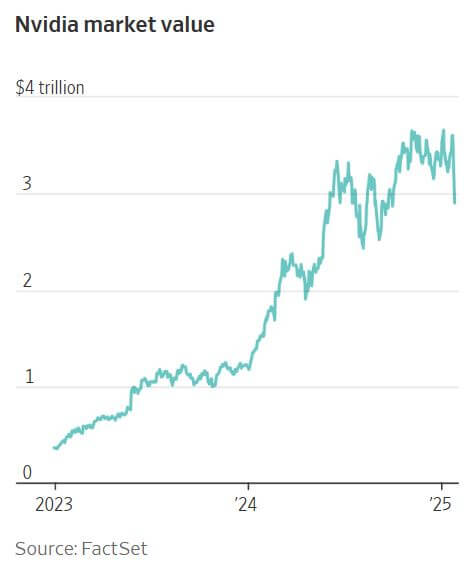

The recent AI-driven market euphoria swiftly turned to panic, with American tech giants losing approximately $1 trillion in value before recovering later in the week. Nvidia, a leader in AI chipmaking, saw its stock drop by 17% on Monday, while Alphabet, Amazon, and Microsoft have also suffered declines. The catalyst for this downturn is DeepSeek, a little-known Chinese AI startup that has shocked analysts with its efficient large language model, R1. Using innovative techniques, DeepSeek has developed AI models that rival Western counterparts but require significantly less computing power and cost. This breakthrough threatens the massive investments American firms have poured into AI infrastructure. In 2023, cloud-computing leaders spent $180 billion on data centers, a figure projected to surge further in 2025. If AI models can now be trained with fewer resources, these expenditures may be excessive, raising concerns for cloud providers, chipmakers, and energy suppliers. Siemens Energy and uranium producer Cameco have already suffered significant stock declines. The implications extend to venture-backed AI firms. Investors committed $132 billion to AI startups in 2024, but DeepSeek’s efficiency could make it harder for cash-burning companies like OpenAI and Anthropic to secure funding. Chipmakers such as Groq and Cerebras, along with AI cloud firm CoreWeave, may also face difficulties. Geopolitics could further disrupt the AI sector, as DeepSeek’s success suggests U.S. chip export restrictions have failed, potentially prompting stricter measures, which could decrease demand for chips. AI demand remains uncertain. If enterprises struggle with large-scale implementation, the current market slump could spiral into a deeper downturn. Technology stocks rebounded later in the week, recovering from Monday’s DeepSeek-driven selloff. The rebound suggests some investors viewed the dip as a buying opportunity.