Stocks fell sharply Friday after weaker-than-expected economic data heightened concerns about corporate America’s outlook, compounded by a surge in long-term consumer inflation expectations—the highest since 1995. Investor sentiment was further unsettled by disappointing readings across consumer sentiment, housing, and services sectors, particularly as the Federal Reserve shows no urgency to cut interest rates. Treasury markets saw a late rally, driving the 10-year note yield down eight basis points to 4.43%, marking its sixth consecutive weekly decline as investors sought safer assets amid falling stocks and oil prices. Market analysts offered mixed perspectives on the outlook. Gina Bolvin of Bolvin Wealth Management suggested that Walmart’s weak retail sales guidance might serve as a catalyst for a healthy correction, though she noted that strong earnings growth and an anticipated Federal Reserve rate cut support a continued bull market. Mark Hackett of Nationwide suggested the market is in a consolidation phase following a robust two-year rally, with potential leadership shifts toward international and value stocks. Ned Davis Research analysts argued that most similar consolidation phases typically led to continued bull markets, barring significant inflation or earnings disruptions. Meanwhile, hedge funds have reduced net positions in most "Magnificent Seven" stocks, with Tesla notably excluded from top holdings. Additionally, median short interest in S&P 500 stocks rose to 2% of market cap—the highest since 2020. In contrast, European equities experienced their largest inflows since the onset of the Ukraine war, reflecting improving business conditions and optimism in markets like Germany, China, Japan, and South Korea.

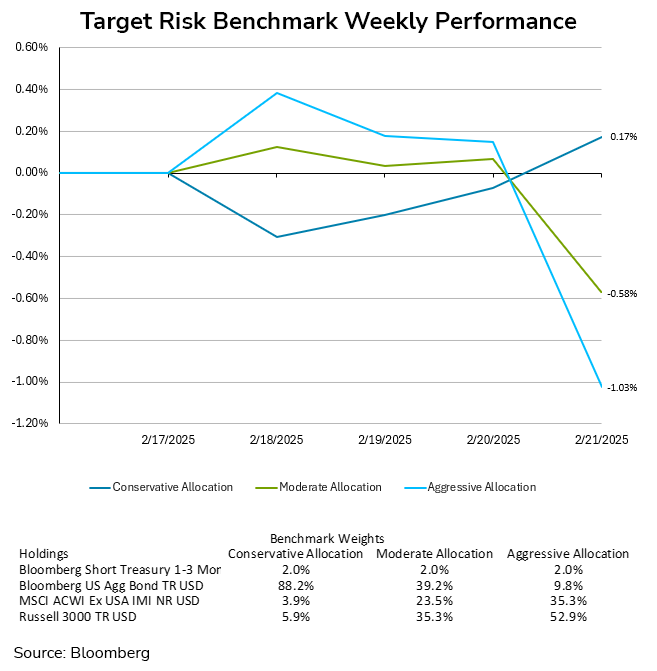

The sudden shift in sentiment resulted in weekly losses for aggressive and balanced investors. Domestic equities sold off significantly, while international stocks were flat for the week. However, bonds thankfully acted as a counterweight as investors sought out safety, helping to offset equity losses. The aggressive target risk benchmark finished the week down -1.03% after the sharp selloff on Friday. The moderate target risk benchmark saw a smaller decline of -0.58% for the week. In contrast declining bond yields benefited the conservative target risk benchmark, which finished the week with a gain of 0.17%.

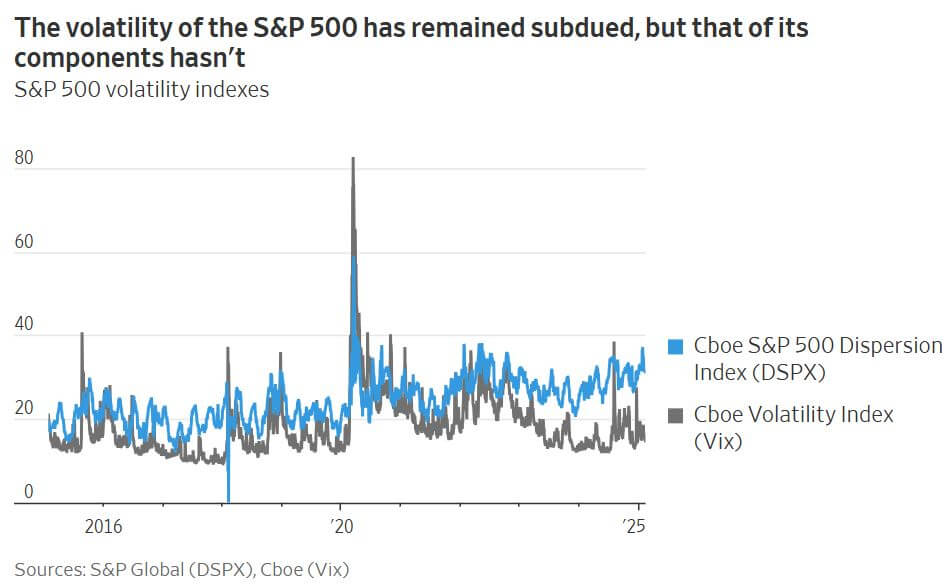

The current stock market presents a paradox: while the S&P 500 has shown relative stability, individual stocks within the index have experienced significant volatility. Year-to-date, the S&P 500 has risen modestly despite disruptions from China’s advancements in artificial intelligence and the Trump administration’s tariff policies. The Cboe Volatility Index (Vix)—the market’s “fear gauge”—has remained below its historical average of 19.5, indicating muted overall investor anxiety.However, beneath this surface stability lies pronounced dispersion—the divergence in individual stock movements. The Cboe S&P 500 Dispersion Index, which measures the degree to which individual stocks deviate from the broader index, has reached its highest level since May 2022. One factor contributing to this phenomenon is the differentiated impact of AI developments. Unlike previous periods when AI enthusiasm uniformly lifted related stocks, the current wave of Chinese AI models poses varying risks and opportunities for different companies. For instance, since China’s DeepSeek AI announcement on January 24, Alphabet’s share price has dropped while Meta Platforms has risen. Similar divergence is evident in companies sensitive to protectionist policies, such as Caterpillar, Hasbro, and Dollar General. Investor behavior may also be amplifying dispersion. Hedge funds increasingly use options to bet on low index volatility while profiting from high individual stock volatility. According to Cboe data, this strategy yielded a 28% return in 2024—outperforming the S&P 500. However, these trades can reinforce volatility by compelling banks, which take the opposite side of these bets, to adjust their equity holdings accordingly. Additionally, the rise of short-term options trading among retail investors and derivative-based ETFs may further distort market signals. Historically, periods of high dispersion often precede broader market volatility, as correlations tend to increase during downturns. Given elevated equity valuations, investors should consider holding bonds and cash as a hedge against potential market disruptions.

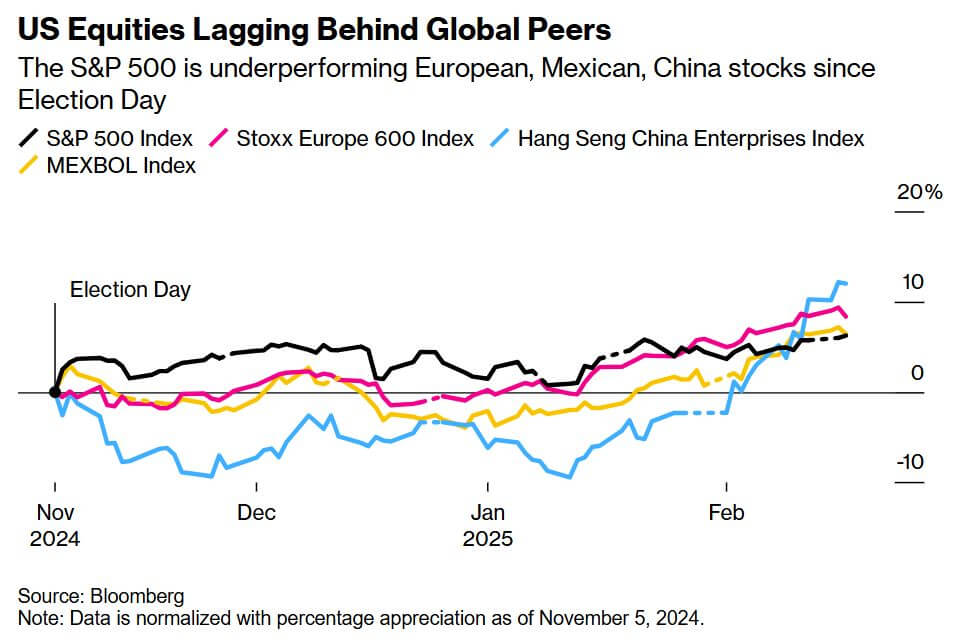

One month into President Donald Trump’s second term, the momentum behind many trades that were initially popular following his re-election has waned. Investors who had anticipated robust growth driven by deregulation, tax cuts, and tariffs are now recalibrating expectations across equities, currencies, and cryptocurrencies. US equities, particularly the S&P 500, have lagged behind global peers like European, Chinese, and Mexican markets. Small-cap stocks, which initially surged due to their domestic focus and expected insulation from trade wars, have since faltered. The Russell 2000 Index spiked 5.8% the day after the election but now sits only about 1% above its November 5 close. Elevated interest rates have disproportionately affected small and mid-sized firms due to their higher debt burdens. Energy stocks, despite an early post-election rally, have returned to pre-election levels, while financial stocks have performed better, with the S&P 500 Financials Index up 12%, largely driven by solid bank earnings. The US dollar, once a primary beneficiary of the Trump trade, has also lost momentum. After rising 4.5% from Election Day through mid-January, the Bloomberg Dollar Spot Index has since declined by 1.5%. Traders had overestimated the inflationary impact of tariffs and their subsequent effect on bond yields. This miscalculation, combined with the Treasury’s decision to maintain steady bond issuance and reduce deficit concerns, has also led to a flattening of the yield curve between two- and 10-year Treasury notes, reversing its sharp post-election steepening. In the cryptocurrency sector, post-election gains have moderated. Bitcoin surged around 50% in the two months following Trump’s victory, fueled by expectations of a more favorable regulatory environment. However, after peaking above $100,000 in January, it has since fallen below $97,000. The administration’s delay in implementing policies like a national Bitcoin reserve and scandals involving meme coins have dampened market enthusiasm.Overall, the initial optimism surrounding Trump’s second term has been tempered by the complex realities of trade policies, interest rates, and delayed regulatory reforms, leading to more cautious investor sentiment across asset classes.